Structure, strategy, and trust Accelerating confidence in the next era of high-net-worth advice.

Structure, strategy, and trust Accelerating confidence in the next era of high-net-worth advice.

Brought to you by Generation Life

In this special production

About this paper

This paper has been prepared by Ensombl as a resource for financial advisers, with the permission and support of Generation Life.

We would like to thank the following adviser contributors:

This report has been accredited with 1 CPD Points. Click here for CPD accreditation link.

By reading this report and completing the 8 multiple choice questions with an 80% pass mark, you will have a better understanding of financial advice for high-net-worth clients, covering trust in adviser/client relationships, legislative impacts on superannuation (e.g., Division 296 tax), tax-effective investing, estate and succession planning, and behavioural coaching, all directly related to financial advice and planning.

1.0 trust and financial advice

Trust has long been seen as a core underpinning of financial advice, being a key driver of a positive reputation for the profession, and reinforcing effective, enduring adviser-client relationships.

Conversely, lack of trust is a barrier to the uptake, and value, of financial advice.

Go back just six years to the post-Hayne Royal Commission era and ASIC’s 2019 Report 627: ‘Financial Advice: What consumers really think’4 , which quantified this barrier, finding lack of trust in financial advisers among the common reasons for choosing to not engage advisers:

Barriers to seeking financial advice

The same research also indicates that lack of trust can still limit openness in some adviser-client relationships. 50% of participants were hesitant to share details of their financial circumstances, and more than one in three said they lacked sufficient trust to fully disclose all the money they had. This may suggest that many clients only become fully transparent once a strong level of trust has been built.

To the extent that clients who trust their adviser are more likely to accept their recommendations, value their expertise, and respond positively to their coaching and reassurance during market turbulence, any lack of openness on the part of the client may therefore undermine the effectiveness, and perceived value – of that advice. In this sense, trust can be seen as the key that unlocks the value of advice and allows its true potential to be harnessed.

And the reason is simple: the stronger the trust, the more engaged clients are – and the more value they can obtain from advice.

2.0 Trust as the key to unlocking value in financial advice

Trust is undoubtedly a critical enabler of effective advice relationships. It has a powerful multiplier effect, converting technical capability into emotional assurance, and determining whether a client accepts recommendations, stays invested, and attributes value to the advice and the relationship.

When trust is strong, the value of advice can compound. Yet when it is weak, holding clients back, even the best designed strategies have a higher risk of failing to connect.

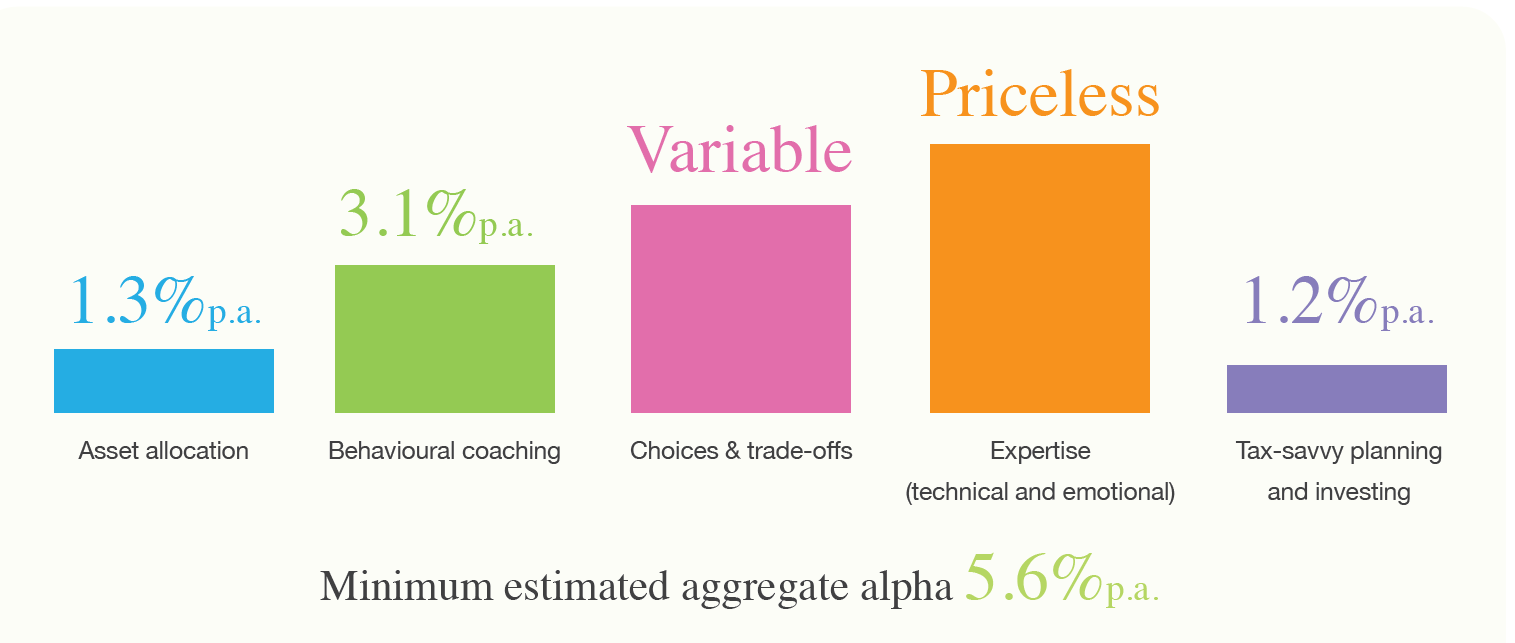

Indeed, according to Russell Investment’s annual ‘Value of an Adviser Study’, trust remains the bedrock of client satisfaction and the single greatest determinant of perceived value. The Russell Investment’s formula quantifies the tangible ‘advice alpha’ to distinct advice components including, from asset allocation and behavioural coaching to tax-savvy planning and expertise.

The 2025 edition of the study estimated that advice delivered an annualised uplift in portfolio performance of at least 5.6 percent, of which more than half was driven by behavioural coaching. This could be said to be the dimension that hinges most on trust and consistency of communication.

Advice value by component

Source: Russell Investments, Value of an Adviser 20258

As research leader, Jason Morris summarised:

The conclusion for when it comes to unlocking value in advice can be considered clear: every dimension of adviser value is interdependent, and each relies on a foundation of trust and transparency to unlock its potential.

2.1 Trust is high and increasing

Australian data confirms that trust among advice clients is already high and remains the decisive differentiator of perceived value.

The FAAA/CoreData ‘Value of Advice’ 2024 study8 found that 94% of advised clients trust their adviser to act in their best interests, 93% credit advice for helping them manage risk, and 92% report improved financial habits.

Clients who trust their adviser not only experienced better financial outcomes but also reported stronger wellbeing, with four in five respondents saying they worry less about money, and half reporting measurable improvements in mental health.

In separate research, CoreData also found that trust has been on an upward trajectory since the 2018 Hayne Royal Commission, and is now sitting close to its previous decade-high level.9

2.2 Trust outcomes magnified for HNW clients

Trust outcomes are magnified among affluent investors.

The State of Wealth series found that HNW and UHNW clients who maintain adviser relationships show greater composure during market volatility; they may attribute their discipline and perspective to their trusted advisers. The 2021 edition of this research10 revealed that 57.2% of HNW investors rely on advisers when making financial decisions, not simply as service providers, but as a guiding hand that reduces uncertainty and knowledge gaps.

As structural and legislative changes become more complex, advice relationships are strengthening and shaping how people respond. Australians are paying closer attention to policy settings and advisers are becoming the anchor helping them to make sense of change. Generation Life’s recent research found 86% of Australians with financial advice report being happy with their financial situation, compared with just 55% without advice.11

2.3 The behavioural logic behind the impact of trust

The behavioural logic behind the impact of trust is simple: trust enables disclosure, and disclosure enables better advice.

Where clients are hesitant to fully share their financial information, advisers are limited in their ability to provide appropriate personal advice and must caution that recommendations may not be suitable. Based on ASIC guidance, incomplete fact-finding and limited client understanding increase the risk of poorer advice outcomes and can undermine consumer trust. Conversely, where early wins and transparent communication build confidence, clients may become more open about goals, fears, and priorities, allowing advisers to deliver holistic strategies that are truly tailored to their real-life values and aspirations.

2.4 Transparent communication is critical

Trust does not magically emerge from qualifications or investment performance, rather it is engineered through the frequency and transparency of communication. Several studies support this

“For me, trust is built by asking the right questions, not by showing how much you know.”

Tony Kofkin

Managing Director | Kofkin Bond

Netwealth’s study13 into high-trust practices found a correlation between client loyalty, and the frequency of proactive communication. More loyal, established clients preferred a higher frequency of personalised contact with their adviser. Conclusion? A cookie-cutter approach of mass communication is unlikely to move the trust needle.

Similarly, PwC’s 2023 research14 found that consistent communication is one of the strongest predictors of both loyalty and advocacy, with trust, transparency, and alignment on goals emerging as the shared foundations of retention and referrals.

This in turn aligns strongly with Vanguard’s Quantifying Adviser’s Alpha framework15, which demonstrates that advisers who provide behavioural coaching – fostering discipline and composure through volatility – can potentially deliver a greater incremental value add for clients.

2.5 Trust amplifies emotional and financial outcomes

Taken together, both Australian and global analyses show that trust can function as both an emotional and economic multiplier, amplifying the perceived and actual value of advice for clients, while reinforcing loyalty, advocacy, and fee acceptance for advisers.

Through this lens, trust is not just a soft virtue, or an ethical ideal for advisers to aspire to, but rather it is an operational asset that amplifies not just the value of advice to clients, but also the value of advice businesses.

In a stable rules environment, this compounding happens gradually. But today the environment is uncertain and subject to change at any time and that alters the trust timeline.

3.0 Trust catalyst – regulatory uncertainty

For much of 2025, the dominant topic among HNW investors and their financial advisers was the Division 296 superannuation tax which has now passed both Houses of Parliament, applicable to funds with earnings on balances over $3 million and $10 million.

Originally proposed in 2023, the looming introduction of the Division 296 tax, and subsequent revisions to its form,16 became the centre of political and media storms. More importantly, it created an unwelcome air of uncertainty for impacted investors, many of whom were left to reassess relevant retirement savings and wealth transfer strategies with superannuation at their core. Anecdotally, HNW investors started to realign some of their portfolios out of superannuation, even before the final legislation has been enacted.

New findings by Generation Life suggest this uncertainty is not theoretical. One-third of HNW respondents who reduced super contributions during the past year did so in response to proposed government tax changes, of those who reduced contributions and almost 40% did so following financial adviser guidance – evidence that policy volatility is translating directly into advice engagement and demand for clarity.17

But regardless of the merits of this reform, and the uncertainty that surrounds its design, what is certain is the opportunity provided to financial advisers to demonstrate their technical capability, and strategic creativity, by helping their clients early on. Even more powerful is the opportunity to show emotional intelligence, by recognising the anxiety, however quiet, that uncertainty plants in the minds of their clients.

Financial adviser insight

“Clarity creates calm. If you’re proactive and transparent, people don’t panic when rules change.”

Michael Bova

Managing Director | Family Wealth Advisory

Financial advisers who anticipate such policy volatility, use their licence authorisations to translate policies into plain language, and guide clients through the implications and responses, are not merely providing technical clarity, they are demonstrating foresight. And when policy risk feels personal – as it can for more affluent individuals (who feel they are being ‘targeted’) – foresight becomes care, and care translates directly into trust.

Further illustrating the financial adviser role as an interpreter, 75% of financial advisers in Generation Life’s research reported speaking to most or all of their clients about the proposed Division 296 since its announcement predominantly around the lack of clarity and concerns about rule changes. Yet 44% of HNW Australians remain unfamiliar with the proposal. Where familiarity does exist, this awareness tends to increase confidence (45% reported higher confidence, versus only 8% lower), underscoring how critical proactive communication is in turning uncertainty into trusted reassurance.18

Financial adviser insight

“The releases of the Division 296 proposals were frustrating, but they also opened up opportunities to show foresight — to get in front of clients, anticipate, and act.”

Tony Kofkin

Managing Director | Kofkin Bond

“Silence is the enemy of confidence. When something like a new potential Division 296 comes up, we’re straight on the phone.”

Les McGuire

Financial Adviser | Future Proof Wealth

Leading, properly authorised financial advisers turn policy volatility into teachable moments. Instead of becoming fixated over new taxes being setbacks, they jump straight into assessing strategic pivots, providing evidence of their role as interpreters of complexity, rather than simply being ‘harbingers’ of bad news.

But legislation is only one front. The second, longer-term catalyst reshaping trust is the change in demographics.

4.0 Generational wealth transfer: the new trust frontier

Beyond legislative uncertainty and change, the second great catalyst reshaping trust in advice is the change in demographics.

But this is not merely a wealth event, it is a trust migration, and a potential existential crisis, for financial advisers who don’t successfully build trust with the inheritors.

Here, LGT20 provides a striking insight: nearly two-thirds of wealthy families have no formal succession plan. This absence of preparation does not reflect indifference, but discomfort – families often avoid confronting mortality, fairness, or control. For financial advisers, this gap may represent both a challenge and an opportunity to lead conversations that clients may not initiate themselves.

Typical fears around wealth transfers and inheritances include:

- Misuse or poor management of inherited assets by the inheritor

- Family conflict and challenges to estates (particularly in blended families)

- Tax inefficiency or erosion

Did you know?

Generation Life’s Investment Bonds offer a flexible, tax-effective approach to intergenerational wealth transfers, easing common concerns and giving families confidence, control and certainty* over how and when wealth is passed on.

Key benefits:

- Tax-effective investment returns

- Simple wealth transfers

- Ownership can be transferred tax-free for income and capital gains purposes

- Flexible structuring, can be used in conjunction with or outside a will

- If appropriately structured, can avoid estate delays, probate, complexities, and uncertainties

- Enables financial advisers to help protect family wealth while preserving flexibility for heirs

Financial advisers are key to solving all these challenges, against a backdrop of the evolving shift in values and priorities among wealth holders.

Knight Frank’s 2023 Wealth Report21 indicates that new wealth creators continue to prioritise growth, control, and capital preservation, reflecting a pragmatic, hands-on approach to stewardship. Their focus on measurable outcomes and performance suggests a stronger emphasis on technical outcomes and functional advice objectives, relative to explicitly values-led considerations

Successor generations, by contrast, increasingly seek to connect wealth with purpose, favouring investments that reflect shared values, sustainability, and legacy. For financial advisers, this evolution signals a move from transactional expertise to relational guidance: the conversation is no longer just about protecting capital, but about sustaining meaning across generations.

Financial advisers who engage heirs early, frame discussions around values, and integrate purpose into portfolio design have been shown as positioning themselves as trusted partners.

Did you know?

Generation Life’s investment bonds can act as a bridge across generations, giving financial advisers a structured way to maintain continuity with the next generation.

By providing a predictable tax treatment on wealth transfer, clear beneficiary rules, and flexible investment options, these solutions can empower financial advisers to gain clients and retain funds under advice when wealth transfers, turning succession planning into a trust-strengthening opportunity.

Financial adviser insight

“The biggest issue is keeping the relationship when wealth transfers. You’ve got to engage the next generation early”

Shane Light

Head of Advice | The Hopkins Group

“For our $50 million-plus families, we hold annual family meetings: we talk about where the wealth came from, the family’s values, and how to be good custodians.”

Michael Bova

Managing Director | Family Wealth Advisory

“I bring the kids into meetings, sometimes in person, sometimes on Zoom, because trust transfers better when everyone’s in the room.”

Les McGuire

Financial Adviser | Future Proof Wealth

The extent to which financial advisers who don’t get this right could be in for a shock. Capgemini research suggests that over 80 per cent of inheritors will sack their parents’ financial adviser within 2 years of receiving their inheritances.22 CoreData is likely to have added to the sense of alarm with their findings that financial advisers lose two-thirds of funds under advice (FUA) on average when money moves between generations.23

“Often younger generations either don’t know who their parents’ financial adviser is or they’re simply not interested in engaging with them. The question for financial advisers becomes: what would happen to your practice if you lost, say, 66 per cent of your funds under advice over the next decade?”24

Brett & Justin Joffe

Flux Finance

Helping clients retain intergenerational wealth means building intergenerational trust. And key to this is understanding generational differences in engagement sequencing and communication styles and channels. For millennial investors for example, trust is built digitally before it is earnt personally.

Financial services entrepreneur Adele Martin observed that:

Younger clients also research extensively or as Martin describes it, ‘stalk’ financial advisers online to assess tone, values, and authenticity. Martin explains that a dated website can break trust before first contact, whereas an active, transparent social presence can act as a digital handshake.

Speaking as a millennial herself, Martin observed:

Many proactive financial advisers have gone to the length of developing new service models catered to younger clients, and matching inheritors with more age-aligned financial advisers.

Financial adviser insight

“We’re pairing younger financial advisers with younger family members now. It’s the best retention strategy we’ve ever had.”

Michael Williams

Managing Director | The Hopkins Group

“It can be harder with younger family members; they don’t want their parents’ financial adviser. So, I bring in younger financial advisers who speak their language.”

Tony Kofkin

Managing Director | Kofkin Bond

“You can’t talk to kids like you talk to parents, they need a completely different language.”

Les McGuire

Financial Adviser | Future Proof Wealth

The implication for financial advisers is profound. The success factors underpinning relationships with first generation clients may not automatically translate to heirs who have different wealth objectives, different time frames, and different communication preferences. Financial advisers who engage heirs well before succession events may, not only secure future clients but also model a wider conception of fiduciary duty, one that boosts the continuity of trust itself.

These catalysts don’t change opinions about whether trust matters – they change how deliberately and quickly financial advisers must build it, and how far it must extend within families.

Designing trust through structure, strategy and systems

5.0 The anatomy of trust

Crucially, trust is also something that can be systemised via structural and procedural design and repeatable behaviours, allowing financial advisers to effectively control how they build trust, and how quickly.

Financial adviser insight

“We’re very systemised around education, transparency, and security. Clients feel cared for when they see you’ve thought about all that.”

Les McGuire

Financial Adviser | Future Proof Wealth

“Part of earning trust is if you say you’re going to do something, you deliver, and then you exceed what you said you were going to do.”

Michael Bova

Managing Director | Family Wealth Advisory

“You can’t shortcut trust, but you can structure for it, with process, with transparency, and with education.”

Shane Light

Head of Advice | The Hopkins Group

Academic research by Devlin et al.27 conceptualised trust not as a single emotion, but a structured mechanism built on three interdependent layers, cognitive, affective, and the overarching influence of institutional trust.

Cognitive trust was said to anchor in competence and reliability; affective trust grows from empathy and goodwill, and institutional trust stems from confidence in the systems and governance that surround advice.

Across a decade of longitudinal data, Devlin’s Trust Index showed that overall confidence in financial services remained relatively stable, even after the global financial crisis, but unevenly distributed. Financial advisers, supported by personal relationships, displayed higher trust results than banks, which bore the brunt of negative perceptions.28

Their findings underline that fairness, transparency, and clear communication are the strongest levers of trust repair. When clients perceive equitable treatment and open dialogue, trust can be rebuilt even amid systemic shocks. In this sense, trust is both emotional and engineered, a measurable outcome of behaviour, structure, and consistency.

5.1 Trust timeline

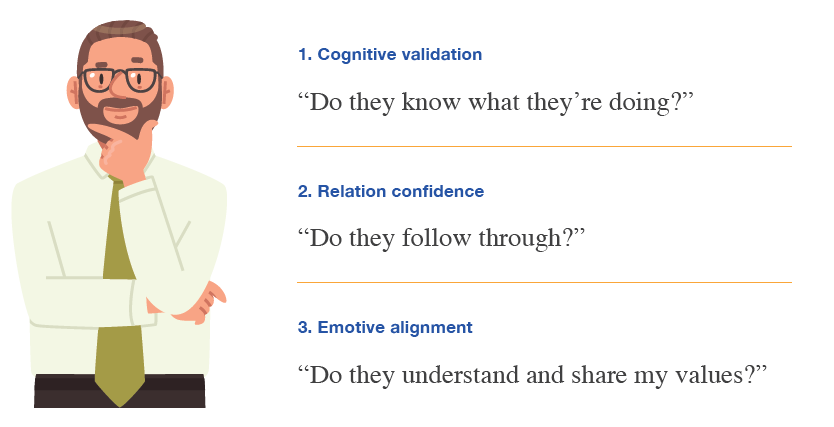

Just as when beginning a new personal relationship, clients rarely extend full confidence at the outset of an advisory relationship; they build it through sequential experiences when competence, reliability, and alignment of interests are validated.

In summary, what we’ve learned from this report is that trust develops in three identifiable phases:

This progression can be visualised as a pyramid, where each level reinforces the next and enduring trust rests on a foundation of consistent delivery.

- Base – Cognitive / functional trust: Formed through early signals of competence and clarity. Clients assess whether the financial adviser is acting in their best interests, demonstrating expertise, providing personalised advice, and explaining recommendations clearly.

- Middle – Developing (relational) trust: Reinforced through reliability and respect, by keeping promises, responding promptly, and following through on commitments.

- Long-term (emotive) trust: Established when values align and clients perceive genuine care, shared purpose, and stewardship over legacy or ESG priorities.

This hierarchy reflects how trust compounds: technical credibility earns confidence; reliability sustains it; and shared values deepen it into advocacy.

5.2 Cognitive/functional trust

At the heart of cognitive trust lies fiduciary intent – the belief that the financial adviser is acting wholly in their client’s best interests. Studies have found this foundational behaviour to be a critical factor of financial adviser trust across all client segments.29

Financial adviser insight

“The number one thing clients care about is not fees, not performance, not tax. It’s whether or not you will act in their best interests… We put ‘acting in your best interests’ on every piece of communication before they even walk in the door.”

Troy Chapman

Financial Adviser | Country Wide Wealth

When clients accept that their financial adviser’s incentives align with their own outcomes, perceived risk declines and emotional safety rises. This effect may strengthen among older and higher-net-worth investors, for whom fiduciary alignment could be read as entailing both competence and care.

“Transparency is arguably the most important quality we bring. I talk clients through the process, the regulations, and how we make sure best interests are always at the forefront.”

Les McGuire

Financial Adviser | Future Proof Wealth

While an FAAA study30 found nearly all advised clients trusted their financial adviser to act in their best interests, the dimensions of trust were found to vary across generations. Older clients tend to equate trust with reliability, expertise, and fiduciary care, while younger investors place greater emphasis on education, accessibility, and digital engagement. The study found that Gen Y clients are twice as likely as Baby Boomers to value a flexible, hybrid advice experience, a reminder that while stewardship builds trust for older clients, connection sustains it for younger ones.

“Education is powerful, you can see trust form in real time when clients start leaning forward.”

Les McGuire

Financial Adviser | Future Proof Wealth

“Education never stops. We revisit the ‘why’ behind every structure, so clients always feel informed and in control.”

Tony Kofkin

Managing Director | Kofkin Bond

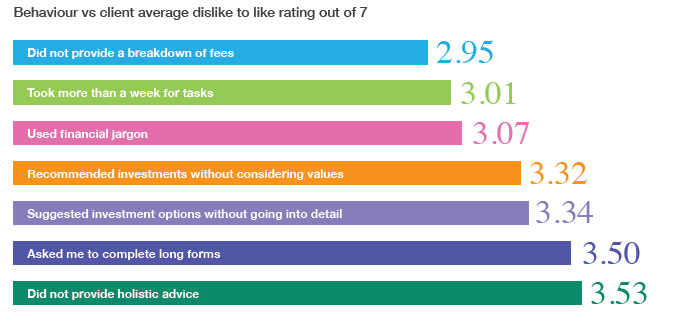

The way financial advisers demonstrate their expertise may also shape the way clients perceive whether their best interests are being served. Financial services products and concepts are complex, with their own highly technical language. But using this jargon to demonstrate competence may create a barrier to trust by reinforcing information asymmetry. Using jargon-free language and being prepared to educate clients shows you are not using knowledge as power, but as a bridge.

Trust barrier – financial adviser behaviours31

Did you know?

Financial advisers using Generation Life’s investment bonds and lifetime income solutions may more easily demonstrate competence and reliability because these structures offer clear rules, a level of control and certainty and transparent recipient arrangements.

By integrating these solutions into their advice, financial advisers can also focus on educating clients and aligning with their values, which can accelerate trust development across cognitive, relational, and emotive phases.

“We make a rod for our own back when we overcomplicate things.”

Tony Kofkin

Managing Director | Kofkin Bond

Demonstrating best-interest behaviours through transparent reasoning, conflict-free recommendations, and clear articulation of value converts technical proficiency into confidence. From this base, emotional trust can take root, transforming professional confidence into personal conviction and ensuring that clients not only believe in the advice, but in the financial adviser.

5.3 Emotional trust – from competence to connection

Once capability is proven, trust evolves from respect to rapport. Emotional trust depends on the financial adviser’s ability to understand their clients’ true values and motivations, not just their balance sheets or surface level goals.

Financial adviser insight

“Trust is earned in the small things — the detail, the follow-ups, the extra call you didn’t need to make”

Shane Light

Head of Advice | The Hopkins Group

“When clients see you calm during chaos, they borrow that calm. That’s trust in action.”

Michael Williams

Managing Director | The Hopkins Group

As advice relationships mature, empathy and values alignment overtake technical skill as the main drivers of loyalty.

Younger generations of advice clients may well turn this sequence on its head. Russell’s 202532 data revealed a great priority on personal values alignment among Gen Z consumers. Nearly half of unadvised Gen Z investors (46%) said they would seek advice if it helped align their investments with their personal values.

Similarly, HNW clients, like other cohorts are said to covet alignment between wealth and personal values.33 Financial advisers who can engage with clients around personal values more quickly, and translate those values into investment intent, can accelerate the strengthening of trust.

“Everyone has a difficult relationship with money. When you wrap family emotions around it, it gets more complex, and that’s where financial advisers can add real value.”

Michael Bova

Managing Director | Family Wealth Advisory

5.4 Structural trust – consistency and independence

Structural trust concerns the systems and governance that make trust repetitive.

For all their flaws, mandatory disclosures and consumer protections within the retail advice system help build client trust and confidence through their mere existence. Clients can take comfort that advice and products are offered within a strict governance framework designed to protect them from financial harm.

Since Covid-19, virtual communication has become entrenched and the traditional wisdom that all clients prefer in-person engagement is no longer true. While a majority of clients prefer face-to-face engagement during onboarding, for many people today face-to-face means virtual.

Findings from a 2024 study in the Journal of Financial Planning35 showed that clients and financial advisers with higher tech-self-efficacy were more likely to view virtual and in-person meetings the same in terms of trust-building effectiveness. The key is to ensure communication channels are aligned to individual client preferences.

Financial adviser insight

“Some of my biggest clients, I’ve never met face-to-face. Trust doesn’t always need a handshake; it just needs consistency.”

Tony Kofkin

Managing Director | Kofkin Bond

Data protection is increasingly important to consumers. Respondents to a 2024 PWC survey36 found protecting their data(79%) was crucial to earning trust—especially in financial advice.

Client portals may also be a tangible example of structural trust. According to PWC, delivering a consistent and reliable customer experience in resolving their concerns was also a critical trust builder, cited by 73% of respondents.37

Fee structures are another structural trust lever. BNY Pershing38 found that HNW and UHNW clients’ preference (32%) is for flat fee models, though some clients valued hybrid models. Regardless of approach, tailoring and transparently explaining fees can be a powerful driver of trust.

Finally, practice business models matter. Independent, flexible practices have been found to be preferred by nearly half of all HNWIs, rising to at least 57% for those aged 50 or more.39 Independence can be proof of objectivity and integrity, and can be crucial for trust to be maximised.

Alongside governance, communication and business models, the choice of structures – from super and discretionary trusts to investment bonds and investment-linked lifetime income solutions – can also shape how “trustworthy” a strategy may feel in practice. Clients may draw confidence from knowing not only what they own, but how it is owned, taxed and ultimately transferred. Structures that provide clear rules around access, beneficiaries and tax treatment can therefore operate as powerful structural trust levers in their own right.

6.0 Structural diversification – a shield against regulatory change

If trust is the foundation of advice, structure is how that trust endures. As legislative and market uncertainties rise, financial advisers are re-engineering wealth frameworks to help withstand change and preserve client confidence. Structural diversification, the deliberate use of multiple ownership, taxation, and control vehicles, has become both a defensive tool every bit as important as asset diversification.

6.1 Structure as a supportive shield

Portfolio diversification can protect against downside risk; structural diversification can protect trust, by ensuring your client’s wealth is insulated from an affective single-point policy threat.

Financial adviser insight

“Diversifying tax structures is your supportive shield against government or legislative change.”

Troy Chapman

Financial Adviser | Country Wide Wealth

“Flexibility is crucial. Everything we put in place has to adapt as rules change. Division 296 is just another reminder that you plan for the unexpected.”

Tony Kofkin

Managing Director | Kofkin Bond

Australia’s shifting legislative environment has become a major determinant of after-tax outcomes, prompting affluent investors to adopt multi-structure strategies that balance flexibility with a somewhat improved sense of predictability.

Recent Division 296 reforms40 are just the latest example of tax policy risk. Other areas remain under the seemingly ongoing spectre of rule changes: negative gearing, franking credits, family trusts, estate taxes, short term accommodation (Airbnb tax), and further superannuation changes.

In this context, diversification of tax structures can become a good enabler for better wealth stability and predictability. For many HNW families, that increasingly means combining super, trusts and companies with structures such as investment bonds and investment-linked lifetime income solutions that can offer tax-effective treatment, provide clear recipient rules and sit outside the superannuation system. Modern solutions in this space – including those offered by Generation Life – are being used as part of a “shock absorber” structure, helping financial advisers reduce single-point policy risk as they give clients greater confidence that their plans will endure through future rule changes from those same policies.

Did you know?

Generation Life’s innovative investment solutions – including investment bonds and investment-linked lifetime income products – can act as a structural “shock absorber” for high-net-worth families. They provide:

- Clear rules for recipients, succession, and control

- Tax-efficient investment flexibility outside of superannuation

- Confidence that wealth strategies can endure through known regulatory changes.

“Diversification generally is a powerful strategy for family wealth. Having assets in different environments gives you resilience.”

Michael Bova

Managing Director | Family Wealth Advisory

6.2 Beyond diversification of assets – diversification of control

Structural diversification concerns not just where assets are invested, but how they are owned.

Discretionary trusts, private companies, self-managed super funds, and investment-bond structures each deliver different governance, tax, and succession characteristics. By blending these, financial advisers may better manage control risk – the risk that legislative change or beneficiary conflict concentrates decision-making power in ways that undermine the owners’ intentions.

For example, investment bond structures can hard-wire rules around who benefits, when and on what terms, converting sensitive control conversations into clear, documented settings.

6.3 Empirical validation – diversifying for financial and emotional resilience

A strong body of evidence supports the importance of structural diversification, not just for investor wealth, but also for peace of mind.

FT Adviser described diversification across tax wrappers as essential for managing liquidity and guarding against changes in tax reliefs. Research from the Oxford Centre for Business Taxation finds that investment tax incentives have much stronger effects in periods of low policy uncertainty than in periods of high uncertainty, suggesting that the stability and predictability of tax rules are critical for encouraging investment.41

A 2025 publication in the Journal of Contemporary Accounting & Economics42 found that firms with more diversified tax strategies experienced lower volatility in effective tax rates, indicating reduced exposure to tax-related risk. While corporate in scope, the findings may be said to translate directly to high-net-worth contexts—diversified tax architecture combining trusts, companies, superannuation, and investment bonds can smooth future outcomes and strengthen confidence in the financial adviser’s foresight.

When clients can see that different “tax homes” are working together – some focused on accumulation, others on succession or income – it is likely to reinforce both cognitive trust (“the strategy is robust”) and emotional trust (“my family will be looked after, whatever happens to the rules”).

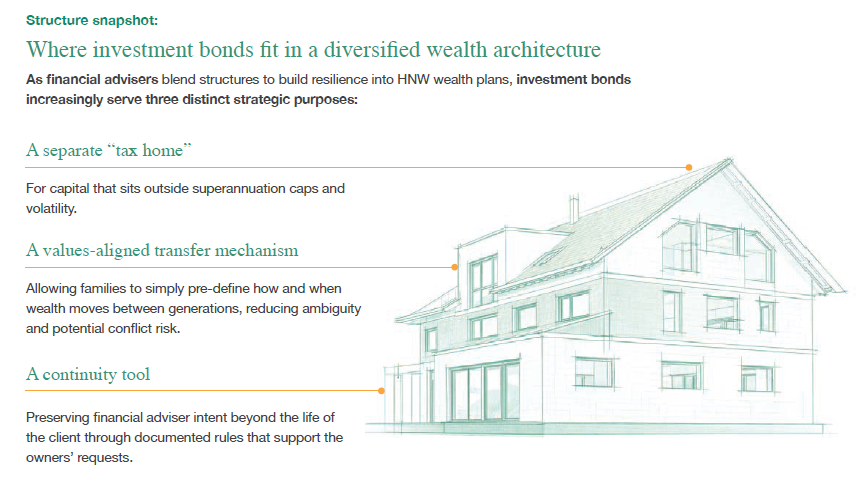

6.4 Designing trust into wealth strategies

Prudent contemporary wealth portfolios from investment houses and investors may operate on two levels: diversification of assets to manage volatility, and diversification of structures to mitigate tax risks. Both increase immunity from shock and drive financial and emotional stability. In effect, trust is increasingly being designed into the architecture of wealth itself – with structures such as investment bonds and lifetime income solutions used to turn intentions about fairness, control and legacy into clear, repeatable rules.

These roles differ from those of superannuation, trusts and companies – which emphasise accumulation, control and asset protection – by focusing instead on predictability, clarity of intent and intergenerational simplicity.

Placed alongside other entities, investment bonds can help financial advisers build trust and provide estate planning certainty into a strategy.

7.0 Case study – designing trust into wealth transfer strategies

To see how structure can actively reinforce trust, consider the example of an HNW family seeking to simplify succession planning and reduce the emotional and administrative challenges of passing wealth between generations.

Context

A family with approximately $5 million in investable assets, diversified across superannuation, discretionary trusts, and direct equities, wished to transfer part of their wealth to adult children without triggering tax inefficiencies or immediate family disputes. Their financial adviser recommended using a tax-paid investment bond structure for a portion of their surplus capital, a vehicle designed to combine disciplined long-term investing with the ability to predetermine future ownership and beneficiary arrangements.

Mechanism

Investment bonds are governed under life-insurance legislation, with earnings taxed internally at a maximum of 30 per cent (although some issuers, such as Generation Life, employ strategies to bring the average effective rate of tax down to about 10%-15%43 over the long-term).

Unlike superannuation, there is no cap on the initial investment, and provided additional contributions stay within the 125% rule (which allows the investment owner to make additional contributions annually up to 125% of their previous year’s contributions) and the investment remains for at least ten years – the investment bond owner can generally make withdrawals fully tax-paid with no personal tax payable.

Unlike conventional family trusts, with the investment bond, the investor nominated beneficiaries directly, bypassing the estate and probate requirements, and for proceeds to transfer smoothly according to documented intentions. Where features such as future-event transfer arrangements or age-based access rules are used, the investment bond owner can specify restrictions on future distributions to intended recipients to align them with the owner’s values, while reducing the potential for conflict or ad-hoc decisionmaking later on.

This approach provided several advantages:

- Clarity and control: beneficiaries or recipients were named explicitly, reducing ambiguity.

- Tax certainty: With no tax payable on future investment bond transfers or death benefit payments.

- Administrative efficiency: The structure limited discretions and minimised the potential for dispute and estate litigation costs.

- Continuity of trust: clear documentation meant the financial adviser’s guidance would continue to shape decisions even after control passed to the next generation.

- Emotional reassurance: the investment bond owner could see, in advance, how and when their wealth would pass to their nominated beneficiaries, helping reduce anxiety about both misuse and unfairness between siblings.

Outcome

The family enjoys increased confidence that their wealth plan was set up to work as intended, and by designing a strategy that removed a lot of uncertainty, the financial adviser’s role evolved from portfolio manager to trusted steward of continuity.

The structure itself became a trust mechanism embodying transparency, consistency, and foresight.

Crucially, the product choice felt like an extension of the family’s intentions –not a constraint on them – which further deepened trust in both the plan and the financial adviser.

Financial adviser insight

“I think investment bonds are one of the top strategies that’ll come out of Division 296 once it is enacted.”

Troy Chapman

Financial Adviser | Country Wide Wealth

“Investment bonds tick so many strategy boxes… At the higher end, bonds can act almost like testamentary trusts…”

Michael Bova

Managing Director | Family Wealth Advisory

8.0 The trust acceleration framework

Financial adviser insight

“You can’t shortcut trust, but you can structure for it, with process, with transparency, and with education”

Troy Chapman

Financial Adviser | Country Wide Wealth

Trust was once considered something that emerged over years. Today, it can be designed, measured, and accelerated. Trust follows a predictable chronology, progressing from understanding and communication to demonstration and reaffirmation. When financial advisers move systematically and deliberately through these stages, by building trust cues into communication and processes, the growth of trust can be accelerated.

Trust acceleration framework:

Step 1 – Understand the client

Outcome: Trust begins with understanding. The first signal of credibility is curiosity, taking time to understand not just financial goals, but motivations, fears, and aspirations. This early empathy lowers perceived risk and replaces evaluation with connection. Genuine understanding will always precede influence.

Step 2 – Communicate clearly and often

Outcome: Clients trust what they can see and understand. Regular updates, transparent reasoning, and proactive outreach transform uncertainty into predictability. Frequency and quality of financial adviser communication are stronger predictors of trust and loyalty than technical expertise alone.

Step 3 – Demonstrate competence with context

Outcome:Competence builds confidence only when clients can follow the logic. Explaining the ‘why’ behind recommendations in plain language shows respect and transparency. It shifts perception from “they know more than me” to “they’re helping me know more.” Competence without context feels like control, but with context, clients feel empowered.

Step 4 – Reassure through consistency

Outcome:Consistency is the quiet language of trust. Keeping promises, being available, and following through, especially during uncertainty, signal reliability. Consistency turns professionalism into dependability and transforms reassurance into habit.

Step 5 – Reaffirm and renew

Outcome:Trust fades without reinforcement. Regular reviews and reflection points sustain engagement and show that the relationship is active, not static. Even when little changes, reaffirming goals and progress preserves confidence.

Step 6 – Reaffirm and renew

Outcome:Each step strengthens the next. Understanding shapes communication; communication validates competence; competence enables reassurance; and reassurance earns renewal. When this sequence is intentional, trust becomes more than a feeling it becomes systemised client confidence.

Financial adviser insight

“It’s never about products; it’s about education, strategy, and structure. If you focus on those three, trust takes care of itself.”

Troy Chapman

Financial Adviser | Country Wide Wealth

Conclusion

Trust runs through every dimension of advice, behavioural, structural, and emotional, but it no longer depends on time alone. Financial advisers who systemise trust-building behaviours can accelerate it by embedding transparency, communication, and consistency into process.

Different generations build trust differently: older and high-net-worth clients value stewardship and stability, while younger investors respond to accessibility and alignment with values. Adapting to those cues is critical for financial advisers seeing to engage multiple generations and play an effective role in the intergenerational wealth transfers.The risk of legislative changes, often seen as a threat, can equally serve as an opportunity to turn uncertainty into reassurance. By implementing clear structures, diversified ownership frameworks and transparent governance, financial advisers can reduce complexity and transform risk into a source of confidence.

Generation Life’s investment bond and retirement income solutions provide the practical tools financial advisers need to do exactly this. Investment bonds offer a simple, tax-effective structure for long-term wealth accumulation, estate planning and intergenerational transfers, providing transparency and control across generations. Retirement income solutions can help advisers design income strategies that help manage longevity risk and deliver certainty, including reversionary pension arrangements to support continuity of income for surviving spouses or dependants.

Together, through their simplicity, structural flexibility and tax efficiency, these solutions help advisers make trust tangible—giving families visibility over how their wealth is managed, built and transferred over generations.

In an environment often defined by ongoing change, Generation Life enables financial advisers to turn trust from an abstract ideal into a demonstrable, enduring foundation for HNW client relationships.

About Generation Life

At Generation Life, we are award-winning market leaders in tax-aware investing, intergenerational wealth transfers, succession planning, and retirement income solutions.

As a wholly owned subsidiary of Generation Development Group (ASX:GDG), we are proud to be part of a broader group that includes Lonsec Research and Ratings and Evidentia Group.

Our support and approach

We specialise in our investment designs, support and products tailored across generations. Our services are underpinned by three key strengths:

Innovation, support and market expertise

We design innovative products that use the power of financial markets to help generate greater wealth and better lifestyles for all Australians. Our leading investment menu provides your clients with a choice of investment management styles and objectives to cater for different goals across all major asset classes.

About Ensombl

Ensombl goes beyond visibility – it creates a pathway for expertise to drive adoption and advocacy within the adviser community.

As Australia’s largest and most engaged network of financial advisers, Ensombl fosters peer-led influence that cuts through a saturated marketplace. In an industry overwhelmed by sales-driven interruptions, advisers trust insights from respected peers over traditional corporate messaging, making Ensombl the ideal platform for authentic engagement.

Through data-driven content, adviser-led discussions, and a highly engaged digital ecosystem, Ensombl doesn’t just connect brands with advisers, it embeds them in relevant conversation, driving connection and adoption.

References

1. Generation Life 2025/26 Navigating Uncertainty Report co-designed with CoreData.

2. Generation Life 2025/26 Navigating Uncertainty Report co-designed with CoreData.

3. Generation Life 2025/26 Navigating Uncertainty Report co-designed with CoreData.

4. Australian Securities and Investments Commission (2019). Report 627: Financial advice: What consumers really think. https://download.asic.gov.au/media/5243978/rep627-published-26-august-2019.pdf, accessed 8 January 2026.

5. Australian Securities and Investments Commission (2019). Report 627: Financial advice: What consumers really think. https://download.asic.gov.au/media/5243978/rep627-published-26-august-2019.pdf, accessed 8 January 2026.

6. Russell Investments, Value of an Advisor Study. (2025). In 2025 Value of an Advisor Study (12th ed., pp. 2-5) [Report; PDF]. https://russellinvestments.com/content/dam/ri/files/us/en/financial-professionalinsights/value-of-an-advisor-study.pdf, accessed 8 January 2026.

7. Wai,M. (2025, August 29). Trust key to client satisfaction in advice: Report. Financial Standard. https://www.financialstandard.com.au/news/trust-key-toclient-satisfaction-in-advice-report-179809727

8. Value of advice Consumer research. (2024). In Financial Advice Association Australia & MYMAVINS, Value of Advice Consumer Research. https://faaa.au/wp-content/uploads/2024/09/FAAA-Value-of-Advice-2024-Report.pdf Report.pdf

9. Siljic, J. (2025, September 19). Adviser trust surges back to 2014 levels, signalling new era of renewed confidence. Independent Financial Adviser. https://www.ifa.com.au/news34772-adviser-trust-surges-back-to-2014-levels-signalling-new-era-of-renewed-confidence, accessed 8 January 2026.

10. Morgan, C., Crestone Wealth Management & CoreData. 2021 State of Wealth Report. https://coredatainsights.com/wp-content/uploads/2021/12/Crestone-2021-State-of-Wealth-Report-new-addresses-ELECTRONIC-lo-res.pdf

11. Generation Life 2025/26 Navigating Uncertainty Report co-designed with CoreData.

12. INFO 267 ‘Tips for giving limited advice’, https://www.asic.gov.au/regulatory-resources/financial-services/giving-financial-product-advice/tips-for-givinglimited-advice/

13. Netwealth. (2025). Netwealth report on client retention in financial advice | Netwealth Advisable Australian 2025 research | Loyalty that lasts. https://www.netwealth.com.au/web/insights/the-advisable-australian/creating-loyalty-that-lasts/

14. PwC. (2023). Transform to build Trust [Report]. PwC’s 11th Global Family Business Survey

15. Kinniry, F. M., Jr., Jaconetti, C. M., DiJoseph, M. A., Walker, D. J., & Quinn, M. C. (2022, July). The Vanguard Group. Putting a value on your value: Quantifying Vanguard Advisor’s Alpha, accessed 8 January 2026.

16. Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026 [and related Bill]

17. Generation Life 2025/26 Navigating Uncertainty Report co-designed with CoreData.

18. Generation Life 2025/26 Navigating Uncertainty Report co-designed with CoreData.

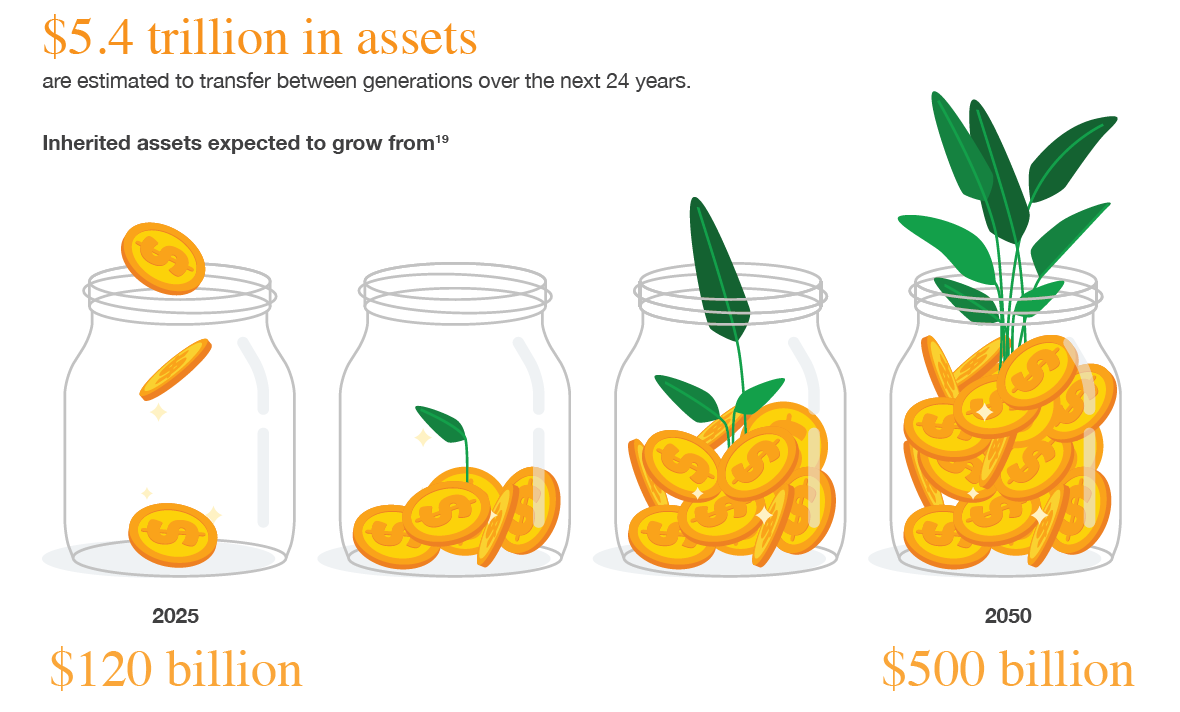

19. Gruber J., Why the $5.4 trillion wealth transfer is a generational tragedy. (2025, March 12). Firstlinks. https://www.firstlinks.com.au/why-the-5-4-trillion-dollarwealth-transfer-generational-tragedy, accessed 8 January 2026.

20. HNWIs favour advice from IFAs: LGT Crestone. Money Management. https://www.moneymanagement.com.au/hnwis-favour-advice-ifas-lgt-crestone/,accessed 8 January 2026

21. Knight Frank, The Wealth Report 2023. https://content.knightfrank.com/resources/knightfrank.com/wealthreport/2023/the-wealth-report-2023.pdf, accessed

8 January 2026.

22. Hayes,E. (2025, June 4.) 81% of young millionaires will drop parents’ advisors, Capgemini says Young. FA-Mag. https://www.fa-mag.com/news/youngmillionaires-considering-dropping-their-advisors–report-82784.html, accessed 8 January 2026.

23. Siljic, J. (2025, April 29). Building trust imperative to retaining intergenerational wealth. Money Management. https://www.moneymanagement.com.au/news/financial-planning/building-trust-imperative-retaining-intergenerational-wealth, accessed 8 January 2026.

24. Siljic, J. (2025, April 29). Building trust imperative to retaining intergenerational wealth. Money Management. https://www.moneymanagement.com.au/news/financial-planning/building-trust-imperative-retaining-intergenerational-wealth, accessed 8 January 2026.

25. Ford, K. (2025, October 28). Embracing change: The shifting landscape of financial advice for a new generation. IFA. https://www.ifa.com.au/embracingchange-the-shifting-landscape-of-financial-advice-for-a-new-generation-2, accessed 8 January 2026.

26. Ford, K. (2025, October 28). Embracing change: The shifting landscape of financial advice for a new generation. IFA. https://www.ifa.com.au/embracingchange-the-shifting-landscape-of-financial-advice-for-a-new-generation-2, accessed 8 January 2026.

27. Devlin, J. F., Ennew, C. T., Sekhon, H. S., & Roy, S. K. (2015). Trust in financial services: Retrospect and prospect. Journal of Financial Services Marketing,

20(4), 234-245 https://irep.ntu.ac.uk/id/eprint/47836/1/1632753_Devlin.pdf

28. Nottingham University Business School, ‘Trust and Fairness in Financial Services’ (2014) https://www.nottingham.ac.uk/business/who-we-are/centres-andinstitutes/gcbfi/documents/crbfs-reports/trust-fair14-devlin.pdf

29. Nottingham University Business School, ‘Trust and Fairness in Financial Services’ (2014) https://www.nottingham.ac.uk/business/who-we-are/centres-andinstitutes/gcbfi/documents/crbfs-reports/trust-fair14-devlin.pdf

30. Value of Advice Consumer Research Key Findings 2024 – Australia. Financial Advice Association Australia. http://faaa.au/wp-content/uploads/2024/09/FAAA-Value-of-Advice-2024-Report.pdf, accessed 8 January 2026.

31. Dastoor, C. (2025, May 22). The most ‘irritating’ behaviours exhibited by advisers. Source of adviser behaviours: Morningstar, Professional Planner. https://www.professionalplanner.com.au/2025/05/the-most-irritating-behaviours-exhibited-by-advisers/\, accessed 8 January 2026.

32. Pretty, R. (2025, September 16). Trust key to client satisfaction in advice — report. Financial Standard. https://www.financialstandard.com.au/news/trustkey-to-client-satisfaction-in-advice-report-179809727

33. Connelly, D., ‘Client Values: How Financial Advisors Can Discover and Use Them to Strengthen Trust and Loyalty’, https://donconnelly.com/client-valueshow-financial-advisors-can-discover-and-use-them-to-strengthen-trust-and-loyalty/, accessed 4 March 2026

34. Netwealth. ‘Understanding Australian Advice Clients Better.’ Accessed January 2026. https://www.netwealth.com.au/web/insights/the-advisable-australian/understanding-australian-advice-clients-better

35. Comparative Perspectives on Virtual Financial Planning: Similarities and Differences between Planner and Client’s Assessments of Virtual Client Meetings.(2024, April 1). Financial Planning Association. https://www.financialplanningassociation.org/learning/publications/journal/APR24-comparative-perspectivesvirtual-financial-planning-similarities-and-differences-between

36. PwC.,Trust in US Business Survey. PwC. https://www.pwc.com/us/en/library/trust-in-business-survey.html, accessed 8 January 2026.

37. PwC.,Trust in US Business Survey. PwC. https://www.pwc.com/us/en/library/trust-in-business-survey.html, accessed 8 January 2026.

38. BNY Pershing & WealthManagement IQ. (2021). Evolution of Advisor Offerings & Investor Preferences: A Guide to What Investors Want From Advisors.https://www.bny.com/assets/pershing/documents/pdfs/perspectives/what-investors-actually-want-from-their-advisors.pdf, accessed 8 January 2026.

39. Nath R., Super top of mind for young HNWIs. (2023, August 2). Super Review. https://www.superreview.com.au/news/superannuation/super-top-mindyoung-hnwis, accessed 8 January 2026.

40. Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026 – accessed March 2026: https://www.aph.gov.au/Parliamentary_Business/Bills_Legislation/Bills_Search_Results/Result?bId=r7437

41. Sardana, S. (2019, February 27). Experts agree on necessity of diversifying tax wrappers. FTAdviser. https://www.ftadviser.com/tax-efficientinvestments/2019/02/27/experts-agree-on-necessity-of-diversifying-tax-wrappers/#:~:text=Tax%20should%20form%20part%20of,may%20tinker%20with%20tax%20reliefs.

42. Krieg, K. S. and Li, J. (2025). Does diverse tax planning reduce tax risk? Journal of Contemporary Accounting & Economics Vol. 21, Issue 3, December 2025, 100490. https://doi.org/10.1016/j.jcae.2025.100490, accessed 8 January 2026.

43. Indicative effective average tax rates for growth focused Tax Optimised investment options. The effective average tax rates represent the estimated average annual tax as a percentage of earnings for each 12-month period over a period of 15 years. Actual tax amounts payable are not guaranteed and may vary from year to year based on the investment option. Past performance is not indicative of future performance.

Disclaimer:

Generation Life Limited AFSL 225408 ABN 68 092 843 902 (Generation Life) is the product issuer, provides general financial product advice and other services related to investment life insurance products and life risk insurance products. Any superannuation general financial product advice provided is by Generation Development Services Pty Limited ABN 14 093 660 523 (GDS) as Corporate Authorised Representative, No. 001317211 of Evidentia Financial Services Pty Ltd AFSL 546217 ABN 97 664 546 525 (Evidentia). The information provided is general in nature and does not consider the investment objectives, financial situation or needs of any person and is not intended to constitute personal financial advice. The product’s Product Disclosure Statement (PDS) and Target Market Determination (TMD) are available at www.genlife.com.au and should be considered in deciding whether to acquire, hold or dispose of the product. Superannuation products’ PDSs, offer documents and TMDs are available via the websites of their product issuers. Generation Life’s products are considered as able to provide certainty and protection as its investment bonds are governed by legislation that has changed infrequently and they can be appropriately structured to bypass an estate and be protected in case of bankruptcy of the life insured, and its LifeIncome product provides a regular income for life. Investments carry risks. Past performance is not a reliable indicator of future performance. Generation Life, GDS and Evidentia exclude, to the maximum extent permitted by law, any liability (including negligence) that might arise from this information or any reliance on it. Generation Life, GDS and Evidentia do not make neither any guarantee or representation that they will derive any particular level of investment returns nor as to the currency, completeness, availability or suitability of any information provided. Generation Life does not accept any responsibility or liability for superannuation general financial product advice provided by GDS.