table, th, td { border: 1px solid; padding:5px;}

The Difference Between Robo-Advice and Digital Advice

When digital advice first launched in Australia, providers were constantly asked .. “So you offer Robo-Advice?” To which the reply was always: Most definitely not!

The misconceptions around digital advice remain in some quarters, so it’s worth revisiting the nature of robo and digital advice, and how they relate to comprehensive – human – advice.

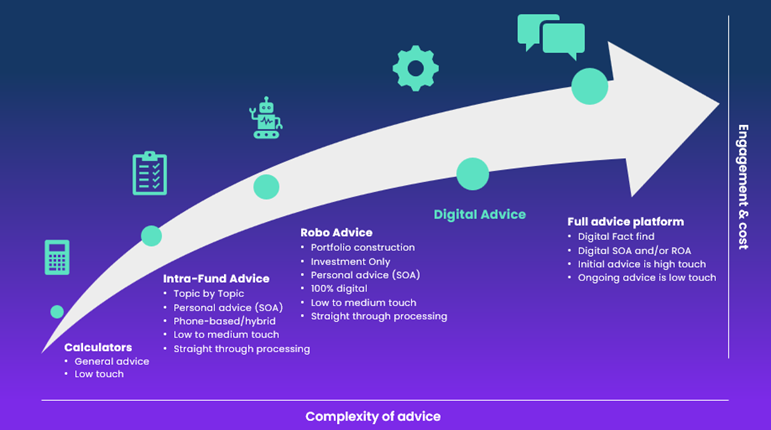

The comparison below looks at the key characteristics of, and differences between these three types of advice, in terms of their delivery, customisation, and the degree of human interaction.

| Advice Type | Characteristics |

| Robo |

|

| Digital |

– Offer complex multi-topic advice – digital offer single topic or scaled advice but will eventually have the capability to offer comprehensive personal advice in the near future. – Use AI to determine advice recommendations: As a rules-based industry, using AI is risky as the tech is always learning and may not adhere strictly to the regulatory requirements that an AFSL must adhere to. Hence the use of rules-based algorithms and stochastic based calculation engines. |

| Comprehensive |

|

Looking at it another way the spectrum of advice models can be summarised as follows.

The growing use of ‘Hybrid’ Digital-Human Advice.

- The Hybrid ‘Digital-Human’ option is becoming more important in offering an experience that delivers the best of the tech with a human element – a critical and a key differentiator in delivering digital advice globally.

It has to be remembered that the great majority of users of digital advice come from a background of:

- having minimal and simple advice needs,

- limited financial literacy,

- a lack of familiarity with digital advice tools

- have never met a financial planner

- All of which means their capability to truly self-serve is also questionable. The hybrid human-digital option offers the affordability benefits of digital, with the ‘safety-net’ of having human support and guidance.

Key take-aways

To summarise, the key differences between Robo-Advice and Personal Advice provided by Digital means lies in the following key areas:

- Degree of Personalisation: It is minimal for Robo as it only covers investment advice, however is fully personal advice via Digital.

- Level of Human Involvement: It is Nil for Robo but available via Digital.

To learn more about MoneyGPS & digital advice, view our Solutions Showcase in the AdviceTech feed of Ensombl.

About moneyGPS: For further information about the moneyGPS Digital Advice offering please contact:

- George Haramis, CEO

- Mobile: 0410 590 526

- Email: george@moneygps.com.au

- Call: 1300 24 24 42 to speak to our Concierge Team.