The US equity rally so far shows no signs of slowing down, and in the wake of the US election results the S&P 500 has been sent to new highs. Despite valuations nearing record territory, many investors are still confident market outperformance could continue into the new year. So where do the opportunities lie for those still keen to tap into the world’s biggest economy?

The rally rolls on

The outsized growth of the Megacap 7 tech stocks, combined with the commencement of interest rate cuts and now a clear election outcome, have helped to push the US equity market from strength to strength in 2024. As of 6 December 2024, the S&P 500 Index is up almost 28% year to date1 , after breaking through 6000 points in mid-November.

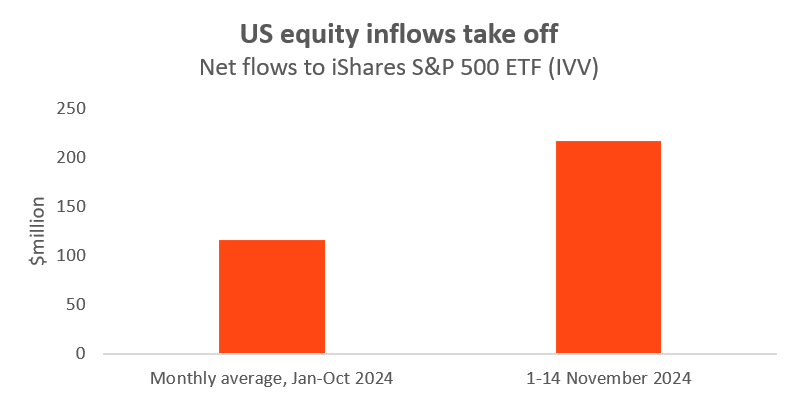

While market sentiment had turned more balanced in Q3 following August’s sharp downturn and in the lead-up to the election, former President Trump’s victory has seemingly provided the signal for investors to re-enter US equities. In the first two weeks of November alone, large-cap US equities took in more than $217 million inflows from Australian iShares investors – almost double their average monthly inflows from January to October 20242.

Source: BlackRock data as of 15 November 2024. Flows are in Australian dollars

Including US mid and small-cap exposures to the mix, total flows to iShares US equities ETFs in the first 14 days of November were more than $240 million3. Large-cap US equities remains iShares’ most popular Australian product category in 2024, attracting more than $1.67 billion in flows year to date4.

How much upside may be left?

By historic measures, it’s not surprising some investors may be questioning whether US shares could run out of puff. Looking at the cyclically adjusted price-to-earnings ratio of the index over the last century, we see that the S&P 500 has only reached these levels a handful of times before – prior to the 1929 crash, the 2000 dot-com bust and during the extreme volatility of the COVID crisis5.

A recent survey of BlackRock global investment professionals reveals more than 60% believe the US is the best market to generate above-benchmark returns in 20256. With 2025 earnings growth for the S&P 500 currently projected at around 14%7 , rate cuts still on the horizon from the Federal Reserve, and economic growth looking robust, macro and business conditions are still supportive of further gains.

Source: LSEG Datastream, BlackRock Investment Institute, 3 December 2024.

Notes: 12 month forward profit margin as calculated by 12-month forward total earnings divided by sales. US represented by MSCI USA Index. Europe represented by MSCI Europe Index. Projections and forward looking statements may not come to pass.

While it also raises risks around persistent inflation, the potential policy agenda of a second Trump presidency is likely to be firmly ‘America first’, including support for domestically focused industries and a tougher trade stance on China – which could contribute to relative outperformance for the equity market. We also see the AI theme continuing to play out in the US long-term, meaning cyclical patterns in stock valuations become less relevant – for instance, megacap tech names may not return to their previous weightings within US equity benchmarks.

Different ways to play the Trump trade

So, which sectors can benefit from these supportive trends? We expect continuing strong earnings from big tech names and are comfortable leaning into the current concentrated AI scenario, which has generated outsized returns for portfolios this year. However, we also see gains broadening out to more cyclical and domestic-focused industries in the US, as a result of the political climate and falling rate environment.

With an over 30% weighting to technology and a long-term track record of over 10% annual returns, the S&P 500 Index remains a simple and powerful option for investors to access the innovative companies driving equity market growth8, with top holdings including Microsoft, Apple and NVIDIA9 .

As the best regarded gauge of US equity market performance, covering around 80% of market capitalisation, investors can also tap into diversified growth from winners beyond tech through the index, capturing the potential market upside of the broader ‘America first’ theme. As an example, some of the largest non-tech stock weightings in the index include Warren Buffett’s insurance giant Berkshire Hathaway, and global wholesale retailer Costco.

For investors wishing to lean further into market performance beyond tech, where valuations are less stretched and macro tailwinds could prove beneficial, mid and small-cap indices offer more concentrated exposure to sectors such as industrials and financials. These sectors have outperformed as part of the ‘rotation trade’ away from megacap names in the second half of 2024, and financials in particular are likely to benefit from a potential Trump policy agenda.

Source: BlackRock based on holdings data for iShares S&P 500 ETF, iShares S&P Small Cap ETF and iShares S&P Mid Cap ETF as of 19 November 2024

Depending on their preferences or views, investors could consider a core allocation to large-cap US equities, while potentially building on tactical ‘tilts’ to small and mid-cap exposures with higher weightings to cyclical sectors. Broadly, with deregulation and corporate tax cuts potentially on the agenda, and the AI theme continuing to expand, we think the US has the potential to outperform well into the new year.

Learn more about BlackRock

Stay ahead of markets with insights from our local and global experts, strategists and portfolio managers. Uncover the latest on the global economy, geopolitics and other timely investment ideas.

REFERENCES

1. Source: BlackRock data as at 6 December 2024. Past performance is not a reliable indicator of future performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

2. Source: BlackRock data as of 15 November 2024

3. Source: BlackRock data as of 15 November 2024

4. Source: BlackRock data as of 30 November 2024

5. Source: BlackRock Investment Institute and LSEG Datastream, November 2024.

6. Source: BlackRock Investment Institute as of 15 November 2024, based on a survey of approximately 100 2025 BII Outlook Forum attendees. Projections and forward-looking statements may not come to pass.

7. Source: BlackRock data as of 18 November 2024. Projections and forward-looking statements may not come to pass.

8. Source: S&P Dow Jones as at 19 July 2024, based on average annualised returns over a 10-year period. Past performance is not a reliable indicator of future performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

9. Source: BlackRock based on top 3 holdings of iShares S&P 500 ETF as at 9 December 2024. For illustrative purposes only. This is not a recommendation to invest in any particular financial product.

Note examples used are the largest financials and consumer staples sector holdings in the iShares S&P 500 ETF. For illustrative purposes only. This is not a recommendation to invest in any particular financial product.

Opinions are subject to change and they are not a guarantee of future results. This information should not be relied upon as research, investment advice or a recommendation.

IMPORTANT INFORMATION

Issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975, AFSL 230 523 (BIMAL) for the exclusive use of the recipient, which warrants by receipt of this material that it is a wholesale client as defined under the Australian Corporations Act 2001 (Cth).

This material provides general advice only and does not take into account your individual objectives, financial situation, needs or circumstances. Before making any investment decision, you should assess whether the material is appropriate for you and obtain financial advice tailored to you having regard to your individual objectives, financial situation, needs and circumstances. Refer to BIMAL’s Financial Services Guide on its website for more information. This material is not a financial product recommendation or an offer or solicitation with respect to the purchase or sale of any financial product in any jurisdiction.

Information provided is for illustrative and informational purposes and is subject to change. It has not been approved by any regulator.

This material is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. BIMAL is a part of the global BlackRock Group which comprises of financial product issuers and investment managers around the world. BIMAL is the issuer of financial products and acts as an investment manager in Australia.

For BIMAL Schemes: BIMAL is the responsible entity and issuer of units in the Australian domiciled managed investment schemes referred to in this material, including the Australian domiciled iShares ETFs. Any potential investor should consider the latest product disclosure statement (PDS) before deciding whether to acquire, or continue to hold, an investment in any BlackRock fund. BlackRock has also issued a target market determination (TMD) that describes the class of consumers that comprises the target market for each BlackRock fund and matters relevant to their distribution and review. The PDS and the TMD can be obtained by contacting the BIMAL Client Services Centre on 1300 366 100. In some instances the PDS and the TMD are also available on the BIMAL website at www.blackrock.com/au. An iShares ETF is not sponsored, endorsed, issued, sold or promoted by the provider of the index which a particular iShares ETF seeks to track. No index provider makes any representation regarding the advisability of investing in the iShares ETFs. Further information on the index providers can be found in the BIMAL website terms and conditions at www.blackrock.com/au.

BIMAL, its officers, employees and agents believe that the information in this material and the sources on which it is based (which may be sourced from third parties) are correct as at the date of publication. While every care has been taken in the preparation of this material, no warranty of accuracy or reliability is given and no responsibility for the information is accepted by BIMAL, its officers, employees or agents. Except where contrary to law, BIMAL excludes all liability for this information.

Any investment is subject to investment risk, including delays on the payment of withdrawal proceeds and the loss of income or the principal invested. While any forecasts, estimates and opinions in this material are made on a reasonable basis, actual future results and operations may differ materially from the forecasts, estimates and opinions set out in this material. No guarantee as to the repayment of capital or the performance of any product or rate of return referred to in this material is made by BIMAL or any entity in the BlackRock group of companies.

No part of this material may be reproduced or distributed in any manner without the prior written permission of BIMAL.

© 2024 BlackRock, Inc. or its affiliates. All Rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, ALADDIN, iSHARES and the stylised i logo are registered and unregistered trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.