A better equities portfolio: actively-managed outperformance with passive-level fees

Equity portfolios offer the lure of enormous gains, but they also come with substantial risk. Fortunately there is a way to shift the balance between risk and return with lower fees than those offered by traditional active managers.

It requires a better understanding of the underlying factors that drive performance. We previously looked at how valuation and momentum drive the bulk of active Australian equity managers’ performance, however there are others.

Referring to “Risk Factors” is just another way to describe the underlying fundamental characteristics that drive equity performance, and they happen to be the same as those espoused by legendary investors such as Warren Buffet. Investors like Buffet look for quality companies that deliver high, sustainable profits over long periods and then buy them at attractive prices.

Stocks that exhibit these characteristics (or factors) show:

• Value (which can be measured in different ways such as a low Price-to-free cash flow, price-to-book or CAPE (Cyclically Adjusted Price Earnings) ratio suggesting the company is ‘cheap’).

• Quality (companies that exhibit stable earnings, low leverage and high profitability).

• Momentum (companies with a rising 6-12-month price, taking advantage of investors short-termism).

• Low volatility (companies with more stable share prices).

The factors that create a foundation for outperformance

An equity portfolio built with stocks that exhibit these factors should outperform a traditional market-cap weighted indexed portfolio. One simple strategy is to split the portfolio evenly between Australian and global stocks, rebalancing each month to those stocks with the highest value, quality, momentum and low volatility scores.

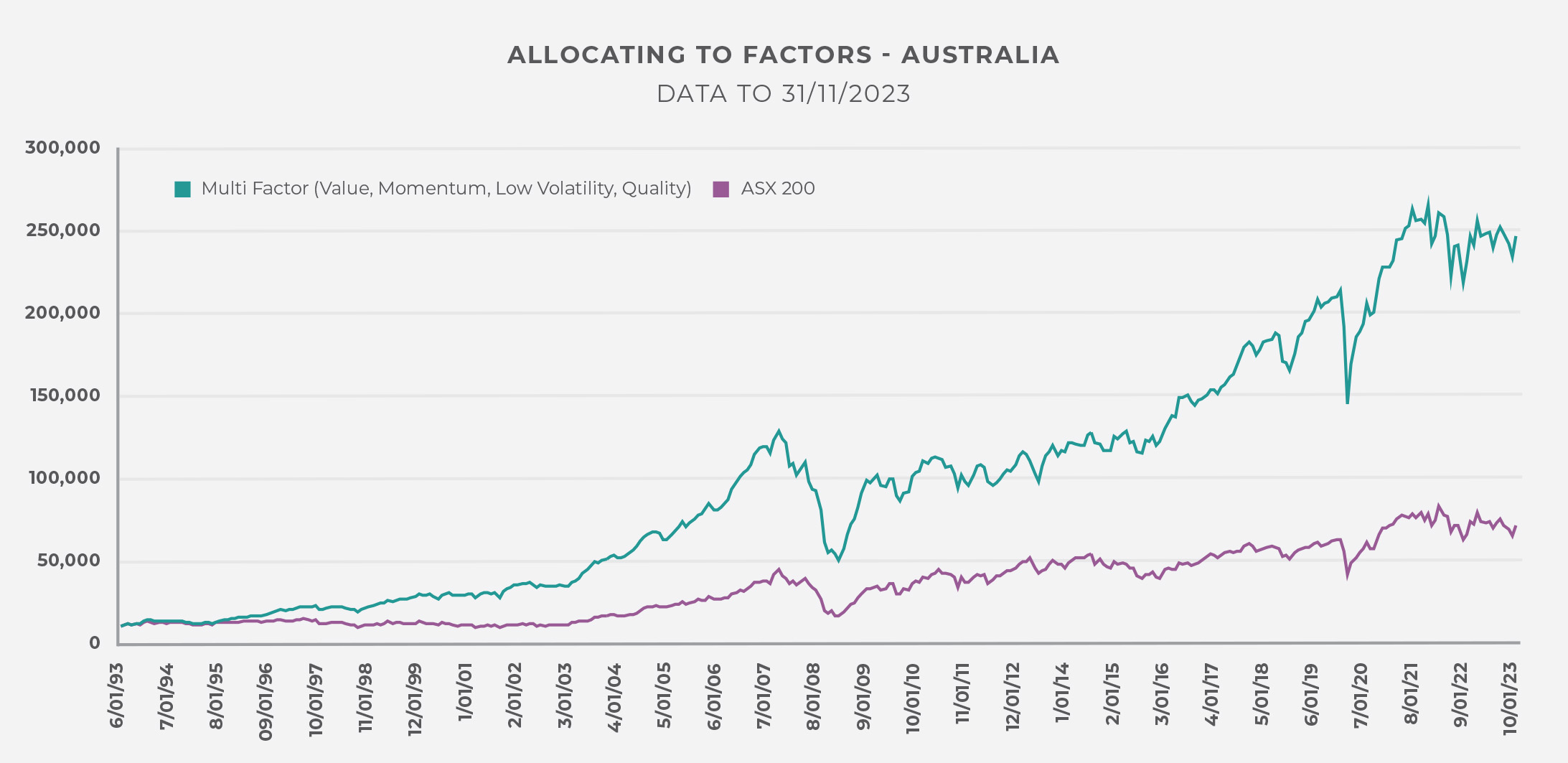

The graph below shows an Australian equity portfolio built using these factors would have delivered a higher expected return between 1993 and 2023

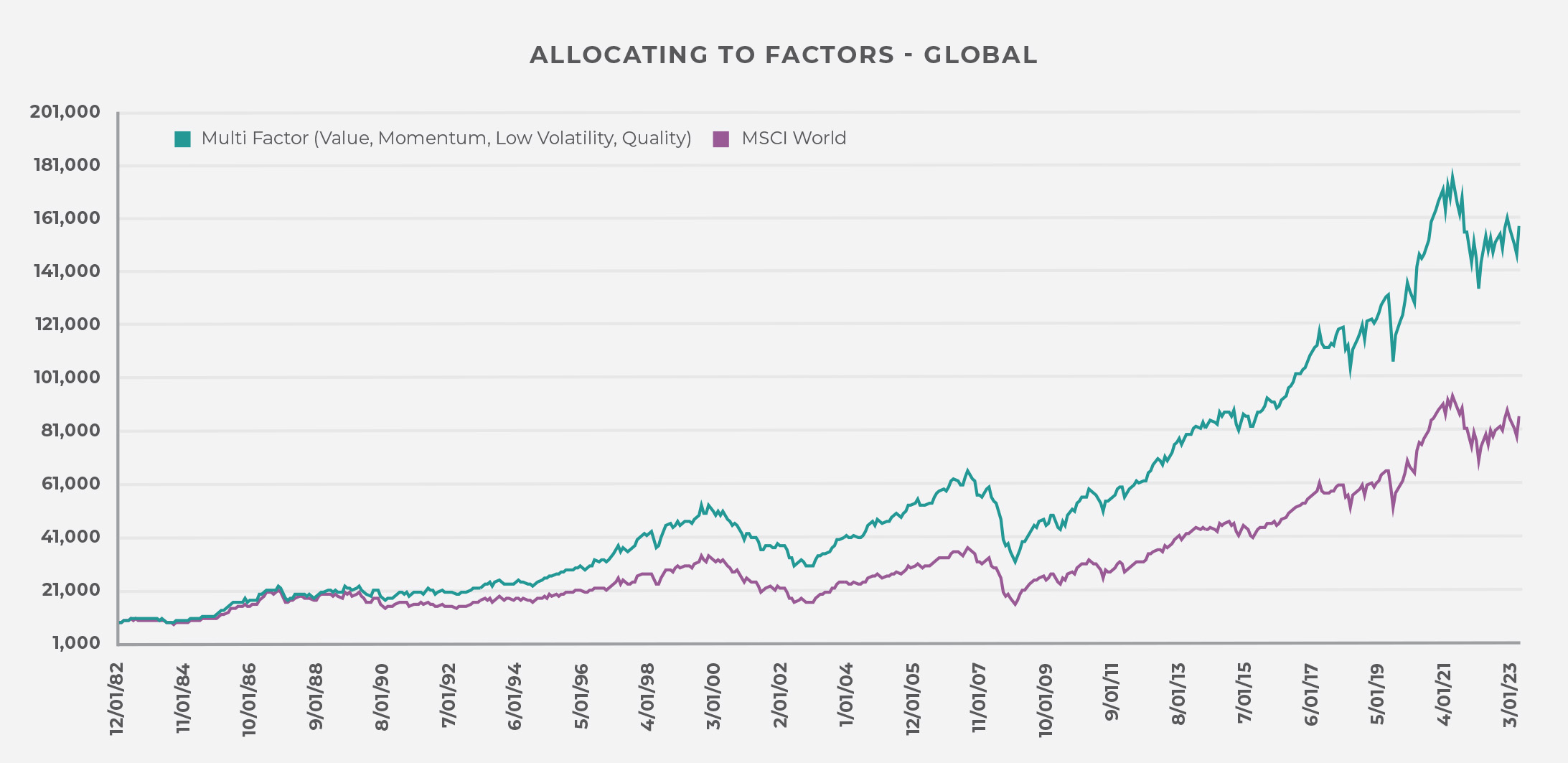

Momentum has historically been a stronger factor in the Australian share market than in many other developed countries such as the US. However, a global equity portfolio built using the same four factors to select stocks also delivered higher returns between 1982 and 2023, as shown in the graph below.

Easier access: building a portfolio with factors

These factors are now available to investors through low-cost exchange-traded fund (ETF) structures, which can have management fees as low as 0.25 per cent.

The US market is the most advanced in the world, where ETFs represent 12.7 per cent of all US equity assets compared to 4.4 per cent across the Asia-Pacific. US-focused ETFs can cover value, momentum, low volatility and quality factors (as well as many others).

While the Australian market is not quite as advanced, there are still ETFs for many factors available. Investors can still create Australian equity multi-factor portfolios using a combination of ETFs and other investment structures, such as managed funds (there may not yet be a momentum or value Australian equity ETF, but there are still momentum and value managers).

This type of static portfolio can reasonably be expected to deliver a higher return over time, but it’s still not the optimal approach because different factors naturally perform at different times (as we saw in regards to manager performance in this white paper, factors tend to follow the same cycles, with those that have performed well over the medium term having a reduced risk premium associated with them, and so cycling to an out-of-favour factor may increase the odds of outperformance).

For example, value wasn’t a strong positive factor for several years when interest rates were falling and investors pumped up loss-making growth stocks .

Innova takes an active approach to portfolio construction, rotating into and out of these factors as market conditions change. This approach increases the chances of delivering higher returns while managing the extra volatility and size of drawdowns associated with equities.

To read more about factors, download Innova’s white paper on Factors, Funds and Performance Chasing here.