The opportunity hiding in your client base: Why ethical investing is no longer niche

{

“@context”: “http://schema.org”,

“@type”: “Article”,

“author”: {

“@type”: “Person”,

“name”: “Erica hall”

},

“datePublished”: “2025-04-15T08:00:00+00:00”,

“headline”: “The opportunity hiding in your client base: Why ethical investing is no longer niche”

}

Financial advice is, at its core, about helping people make choices that align their money with their lives. Advisers ask their clients about risk tolerance, time horizons, and retirement goals as a matter of routine.But there is one simple question that many advisers still overlook, and it may be costing them client loyalty, referrals, and growth.

Would you like your investments to reflect your personal values?

This small addition to a fact-find or review conversation can have a disproportionate impact. In one advice practice, this single line was added when offering clients four managed account models, index, active, direct equities, and sustainable. Without a campaign or any expectation of strong demand, one in five clients opted for the sustainable model. Twenty percent of their book. These were clients who might otherwise have been disengaged or questioning whether their adviser truly understood them. Instead, they became more loyal, more engaged, and more likely to refer.

For advisers, this is the opportunity hiding in plain sight.

From niche to norm

Only a decade ago, ethical investing was seen as fringe. Some viewed it as a fad, a nice-to-have that might come at the expense of returns. Today, the landscape is very different.

Ethical portfolios do look different from the broader market. They avoid or underweight certain sectors and companies, while tilting toward others with stronger governance or sustainability profiles. At times, this creates divergence: periods of underperformance when excluded sectors rally, or outperformance when preferred areas lead. Over the long term, however, these effects have tended to balance out — and performance has in many cases compared favourably with the market.

According to the Responsible Investment Association of Australasia (RIAA)1, 88% of Australians now expect their investments to be responsible and ethical. Research by Netwealth found that among the emerging affluent, the very clients advisers most want to attract over the next decade, 76% already hold responsible investments in their portfolios2

RIAA’s research also highlights a growing assumption among clients: that their portfolios are already being constructed through a responsible investing lens. In other words, many clients now expect advisers to consider ESG factors by default.

This shift is being driven by several forces. Intergenerational wealth transfer is placing more capital in the hands of younger clients who want their portfolios to reflect their values. Women, who research shows are more likely to prioritise ethics, are playing an increasingly central role in household financial decisionmaking. And critically, a growing body of studies has shown that investors don’t necessarily need to sacrifice performance to invest responsibly, making the case for ethical investing even more compelling.

For many clients, this makes it an easy choice: why wouldn’t they align their wealth with their values if longterm returns can remain competitive?

What “ethical” really means

Part of the hesitation advisers feel about this space stems from the language. ESG, ethical, sustainable, impact investing – it can seem like a moving target and the sector is sometimes dismissed as “the alphabet soup”. The reality is simpler than it looks.

Ethical investing is primarily about alignment. It involves excluding industries such as fossil fuels, gambling, or tobacco; tilting portfolios toward companies with stronger environmental, social and governance practices; and using stewardship, engagement and voting, to push for better corporate behaviour.

Most clients don’t expect every holding to be flawless, they simply want confidence that their money isn’t working against their values. They want authenticity, managers with transparent screening processes, and credible third-party verification. They want peace of mind.

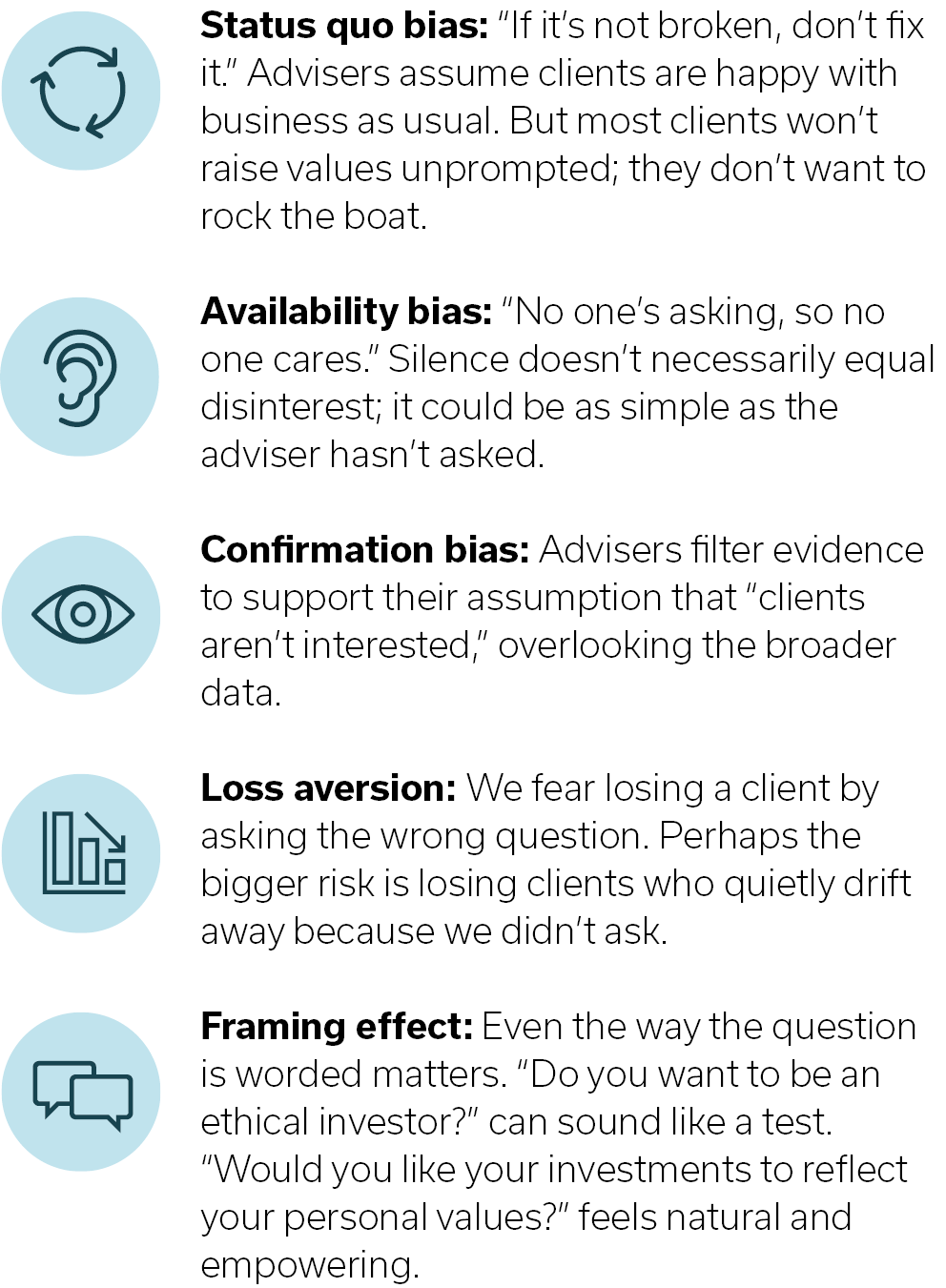

Advisers’ blind spot

So, if client appetite is this strong, why isn’t every adviser embedding values-based investing into their process? The answer may lie in behavioural bias, not in clients, but in advisers themselves.

In other words, the obstacle is not client resistance, it’s adviser hesitation.

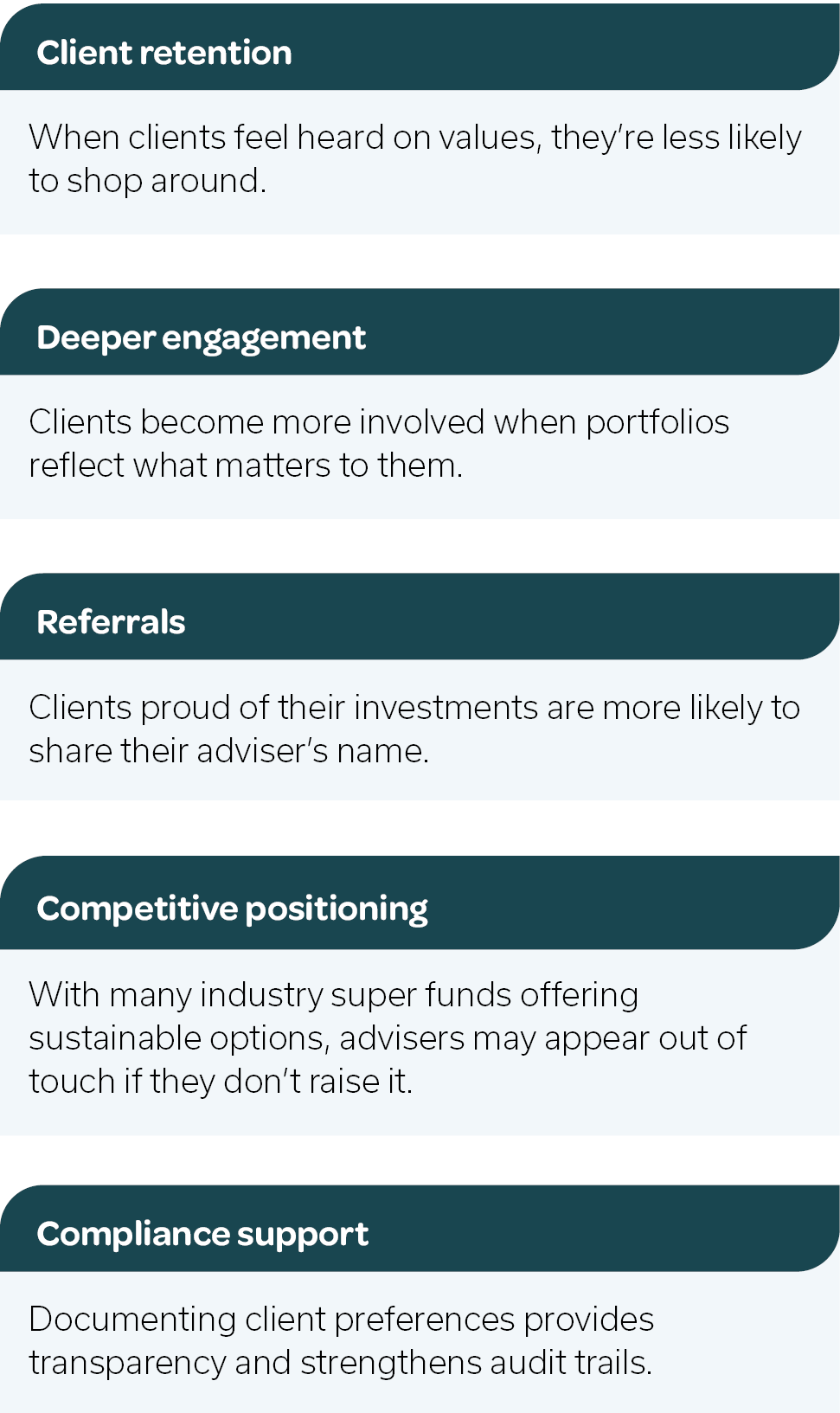

A strategic growth lever

Bringing ethical investing into the advice process is not about creating another product conversation. It’s about creating stronger relationships and building resilience into your practice.

The practical implementation doesn’t need to be difficult. Today, there is a wide range of managed accounts, model portfolios, and ethical solutions available. In other words, you don’t need to reinvent the wheel, you just need to be willing to offer the choice.

Avoiding pitfalls

Of course, there are traps to avoid. “Greenwashing” remains a risk, with some funds overstating their credentials. Advisers should look for fund managers with transparent screening, clear reporting, long track records, and independent certification (e.g. RIAA).

Another trap is assuming clients demand perfection. Most don’t. Many simply want to know that their investments align with their values.

The opportunity ahead

When advisers start these conversations, the impact can be profound. A client who once saw their portfolio as a set of numbers now sees it as an extension of their values. A family looking to transfer wealth feels confident the legacy will reflect their principles. And an adviser who once worried about asking a difficult question might find themselves at the centre of deeper, more trusting relationships.

The data is clear. The demographic tailwinds are strong. And the question is simple: ‘Would you like your investments to reflect your personal values?’

For many clients, the answer will be yes. And for advisers, the rewards, in retention, engagement, referrals, and differentiation could be transformative. This isn’t a passing trend. It’s fast becoming the baseline. Every client meeting where you don’t ask is a lost opportunity, for stronger relationships, for referrals, for growth. The next generation already assumes ESG is built in. If you’re not leading the conversation, someone else will.

So, ask the question. Offer the choice. Because if not now, when?

To receive 0.25 Client care and practice CPD points for this article, complete the quiz here.

Reference

1.Responsible Investment Benchmark Report Australia

2.Netwealth Advisable Australian Research – Understanding Australian advice clients better 2024.

This information is provided by Uniting Ethical Investors Limited (ABN 46 102 469 821) (AFSL 294147), trading as U Ethical. U Ethical can be contacted on 1800 996 888 or by mail and in person at Level 6, 130 Lonsdale Street, Melbourne VIC 3000.

The information provided is general information only. It does not constitute financial, tax or legal advice or an offer or solicitation to subscribe for units in any U Ethical product. It does not take into account your personal objectives, financial situation or needs.

Before acting on the information or deciding whether to acquire or hold units in a U Ethical product, you should consider whether the product is appropriate for you given your own objectives, financial situation and needs. You should also consider the disclosure document(s) for the product (such as the product disclosure statement and target market determination). The disclosure documents are available on our website www.uethical.com or can be provided by calling us on 1800 996 888.

U Ethical may receive fees in respect of investments in U Ethical products. U Ethical directors and employees do not receive commissions from investments in the products and are remunerated on a salaried basis.

U Ethical accepts no liability for any inaccurate, incomplete or omitted information of any kind or any losses caused by using this information.

All investments carry risks. There can be no assurance that the U Ethical product will achieve its targeted rate of return. There is no guarantee against loss resulting from an investment in the U Ethical product. Past performance is not indicative of future performance.

Image credits: Unsplash