With the US election result having provided some welcome clarity to markets, focus now shifts to the broader macro environment as we head into 2025. Can the Fed continue cutting rates, and where will the opportunities come from as earnings broaden out from US large-caps? At BlackRock, we see some key themes driving market activity in the months to come.

1. 2025: The year of the rate cut?

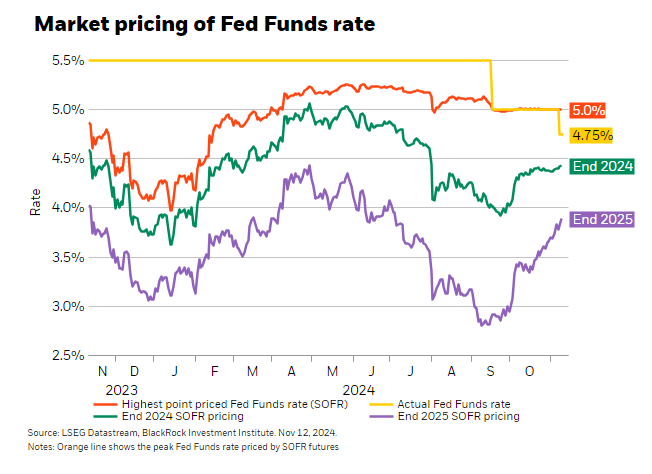

At the beginning of 2024, markets were riding high on optimism that interest rate cuts were coming hard and fast from the Federal Reserve and other developed market central banks. Those rate cuts have materialised later in the year than many expected, but we do expect the Fed to continue on a dovish path heading into 2025 given that reasonable progress has been made taming inflation in the US economy.

The Fed’s focus has shifted to supporting the domestic labour market as we’ve seen softer jobs data out of the US, which we believe is the thinking behind the relatively rapid start to the rate cut cycle over their September and November meetings. However, we are of the view that markets may still have priced in too many cuts by the end of 2025, and recent CPI figures are a warning that inflation could still surprise to the upside – particularly given some of the policies floated by President-elect Trump are expected to put upward pressure on prices.

Turning to Australian interest rates, however, in disappointing news for mortgage holders we expect the rate cut cycle to be slower and shallower than in other developed markets. Inflation is more of a concern for the RBA than supporting the broader economy, with growth still in modestly positive territory and the jobs market holding up well despite somewhat restrictive monetary policy conditions.

Turning to Australian interest rates, however, in disappointing news for mortgage holders we expect the rate cut cycle to be slower and shallower than in other developed markets. Inflation is more of a concern for the RBA than supporting the broader economy, with growth still in modestly positive territory and the jobs market holding up well despite somewhat restrictive monetary policy conditions.

We saw the central bank soften their language around a rate cut to some degree in their November meeting, so the good news is that cuts are coming. But we expect the RBA to be much more cautious in their approach than the Fed, with just a handful of 25 basis point cuts expected to start early to mid next year.

2. Emerging markets: Don’t get China FOMO

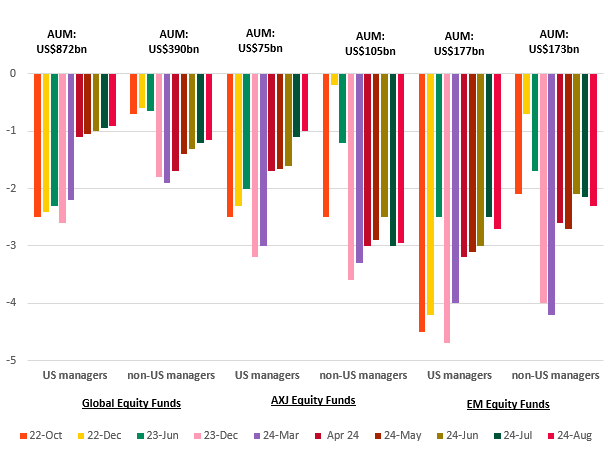

China’s stimulus announcement in late September came as a huge surprise to markets, reversing year-to-date declines in Chinese equities and providing a short-term ‘sugar rush’ to China ETF flows. We see this trend as mainly being driven by fund managers seeking to rebalance their Asian equities allocations after years of going underweight China (see chart below), as well as Chinese investors re-entering the local equity market.

China underweight positions

Top 30 global mutual funds by category

Source: Source: Morningstar, Factset, EPFR. Notes: Data as of end-August 24. Fund universe of each category is formed by the largest 30 active mutual funds under Morningstar regional category. All the covered funds are benchmarking to either MSCI or FTSE standard regional indices of All Country World, Asia ex-Japan or Emerging Markets.

Source: Source: Morningstar, Factset, EPFR. Notes: Data as of end-August 24. Fund universe of each category is formed by the largest 30 active mutual funds under Morningstar regional category. All the covered funds are benchmarking to either MSCI or FTSE standard regional indices of All Country World, Asia ex-Japan or Emerging Markets.

The jury is still out on whether the stimulus itself is enough turn around China’s long-term challenges, and on which sectors in particular will benefit. But the momentum created by the announcement alone, combined with record low valuations in Chinese equities, creates a buy signal that is difficult for investors to ignore.

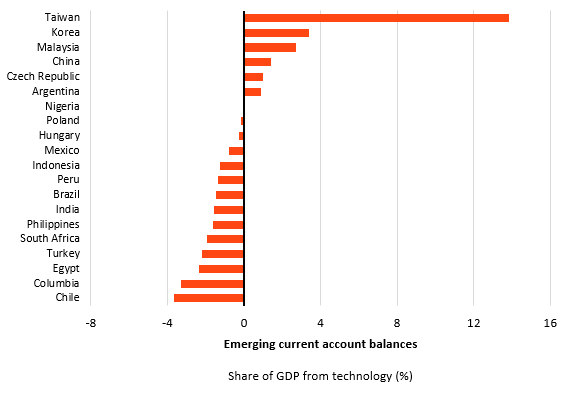

We see merit in jumping into the China trade in the short term with some basic index exposure, particularly if investors have been underweight China previously. But on a long-term basis, India with its demographic and export advantages, and tech-heavy Taiwan and South Korea present better prospects (see chart below).

Source: LSEG Datastream, IMF and BlackRock Investment Institute, April 2024

Source: LSEG Datastream, IMF and BlackRock Investment Institute, April 2024

Given the very separate structural forces at play across these emerging market economies, we think separating China from its EM neighbours makes sense from a portfolio allocation perspective. On a broader basis, we like EM as a diversification play in the months ahead – the long-term structural tailwinds for some of these markets are much different to the traditional commodity-heavy make-up of the EM index in years past.

3. Japan: Looking beyond the yen

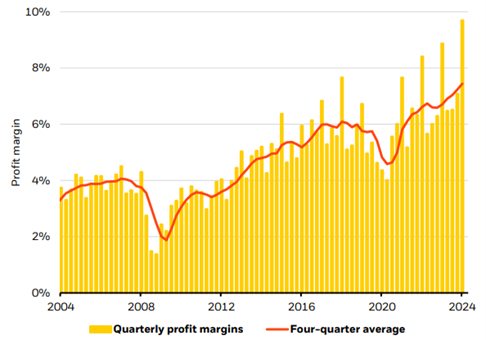

With interest rates on their way down in the vast majority of developed nations, Japan may be the only outlier in this category, having recently seen its first rate rise in more than 15 years. While in August we saw Japan’s worst equity market downturn since the 1980s, this was primarily due to the unwind of the yen carry-trade, which has been extremely popular in recent years with hedge fund and quant managers taking advantage of Japan’s ultra-low interest rates.

Aside from this technical anomaly we believe the macro fundamentals in Japan still look extremely strong, with tailwinds from corporate structural reforms, US$7 trillion in household savings waiting to be deployed into markets, and inflation holding around the Bank of Japan’s 2% target. However, we do keep a keen eye to the effect of any further rate rises and currency fluctuations on corporate earnings – two key pieces to watch on Japan next year.

Japan corporate profit margins, 2004-2024

Source: BlackRock Investment Institute, Japan Ministry of Finance (MOF), with data from Haver Analytics, September 2024. The bars show operating profit margins of companies in all industries excluding finance and insurance, based on data from MOF’s Financial Statements Statistics of Corporations by Industry, Quarterly. Past performance is not a reliable indicator of current or future results.

Source: BlackRock Investment Institute, Japan Ministry of Finance (MOF), with data from Haver Analytics, September 2024. The bars show operating profit margins of companies in all industries excluding finance and insurance, based on data from MOF’s Financial Statements Statistics of Corporations by Industry, Quarterly. Past performance is not a reliable indicator of current or future results.

4. Commodities: The gold rush continues

This year we’ve seen gold surge to record highs on the back of continued central bank buying and geopolitical tensions. We think this momentum is likely to continue into next year, particularly with interest rates coming down in the US and Europe.

We’ve seen investors return to gold ETFs in 2024 as well, albeit modestly, so we do think there is plenty more to come from an inflow perspective next year.

Overall, we see a positive outlook for risk assets heading into 2025 as easing rates and a pro-growth environment in the US are expected to keep equity markets humming. Despite stretched valuations, robust fundamentals continue to drive large-cap tech growth in particular.

However, earnings are expected to broaden out to a wider range of winners than we have seen in 2024, as the global easing cycle gets underway and the AI transformation evolves into new areas.

Learn more about BlackRock

Stay ahead of markets with insights from our local and global experts, strategists and portfolio managers. Uncover the latest on the global economy, geopolitics and other timely investment ideas.

IMPORTANT INFORMATION

Issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975, AFSL 230 523 (BIMAL) for the exclusive use of the recipient, which warrants by receipt of this material that it is a wholesale client as defined under the Australian Corporations Act 2001 (Cth).

This material provides general advice only and does not take into account your individual objectives, financial situation, needs or circumstances. Before making any investment decision, you should assess whether the material is appropriate for you and obtain financial advice tailored to you having regard to your individual objectives, financial situation, needs and circumstances. Refer to BIMAL’s Financial Services Guide on its website for more information. This material is not a financial product recommendation or an offer or solicitation with respect to the purchase or sale of any financial product in any jurisdiction.

Information provided is for illustrative and informational purposes and is subject to change. It has not been approved by any regulator.

This material is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. BIMAL is a part of the global BlackRock Group which comprises of financial product issuers and investment managers around the world. BIMAL is the issuer of financial products and acts as an investment manager in Australia.

BIMAL, its officers, employees and agents believe that the information in this material and the sources on which it is based (which may be sourced from third parties) are correct as at the date of publication. While every care has been taken in the preparation of this material, no warranty of accuracy or reliability is given and no responsibility for the information is accepted by BIMAL, its officers, employees or agents. Except where contrary to law, BIMAL excludes all liability for this information.

Any investment is subject to investment risk, including delays on the payment of withdrawal proceeds and the loss of income or the principal invested. While any forecasts, estimates and opinions in this material are made on a reasonable basis, actual future results and operations may differ materially from the forecasts, estimates and opinions set out in this material. No guarantee as to the repayment of capital or the performance of any product or rate of return referred to in this material is made by BIMAL or any entity in the BlackRock group of companies.

No part of this material may be reproduced or distributed in any manner without the prior written permission of BIMAL.

© 2024 BlackRock, Inc. or its affiliates. All Rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, ALADDIN, iSHARES and the stylised i logo are registered and unregistered trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.