Emerging market equities trade at roughly a 60% discount to the US, nearly the widest gap on record. Combined with attractive currency valuations, ongoing market and governance reforms, and differentiated returns drivers, we believe emerging markets may be one of the most overlooked opportunities in global equities today.

For the past fifteen years, investors have been rewarded for keeping things simple: owning US equities and mega-cap stocks. That instinct has been understandable. The US market has delivered exceptional returns driven by a narrow group of large companies whose growth, profitability and market dominance have repeatedly justified investor confidence.

Indices designed to represent global diversification now allocate roughly 65% to the United States—the highest proportion on record. That concentration was reinforced by the other defining story of the period: emerging market underperformance. As capital crowded into the US, emerging markets were left behind, and the case against them—weak governance, prolonged underperformance and volatile currencies—became embedded in investor thinking.

That thinking still shapes portfolios today, even if the reality on the ground has changed. While some emerging markets do face challenges, in many cases they are already reflected in the price. What is less well reflected is how much has changed.

When we look at valuations, reforms underway, cheap currencies and potential diversification benefits, we believe emerging markets may represent one of the most overlooked opportunities in global equities today.

Valuations: near the widest discount to the US on record

Valuations are a useful place to start. Using a cyclically adjusted price-to-earnings ratio, US equities currently trade at roughly 35 times earnings, whilst emerging markets change hands at around 16 times earnings. That is a 54% discount to the US, below emerging markets’ own long-term average and near the widest gap on record. The last time valuations diverged this sharply was the late 1990s, when US internet stocks were pricing in a tech revolution and Asian economies were in the grip of a financial crisis.

Historically, when US shares have traded at today’s elevated multiples, forward returns have been reliably lacklustre, barely keeping pace with inflation.

For emerging markets, the range of outcomes from today’s starting point is wider, but the skew looks materially more favourable. Historically, the average investor buying US equities at current valuations did about as well as the unluckiest investor who bought emerging market shares at today’s prices.

Depressed valuations, however, are not a sufficient investment case on their own. What matters equally is whether the fundamentals are changing and here, the picture is in our view more encouraging than the prevailing narrative reflects.

Reforms: the shift that markets may be underestimating

Macroeconomic policymaking across many emerging economies bears little resemblance to that of earlier cycles. Central banks are more independent, more credible, and more transparent. Financial systems are better capitalised and less reliant on short-term foreign currency funding. The fiscal prudence of markets scarred by the Asian Financial Crisis now stands in stark contrast to developed economies struggling with mounting debt burdens.

At the corporate level, structural reforms are beginning to strengthen governance and shareholder protections. South Korea is a case in point. Parliament has amended Korea’s Commercial Act—the laws that govern Korean businesses—multiple times; company managers now owe a fiduciary duty to shareholders, not merely to the firm itself. The results are already visible.

KB Financial, the parent of Korea’s largest bank, has curtailed overseas acquisitions and returned capital to its shareholders instead—its share price has more than doubled since the start of 2024. Samsung Electronics, Korea’s largest company by market capitalisation, also announced a buyback of approximately US$7 billion in 2024 in the face of pressure from shareholders. These are early-stage developments and setbacks remain likely, but they are evidence that the mechanics of value creation are changing.

The reforms reshaping emerging market policy frameworks and corporate behaviour have a currency dimension that is equally underappreciated.

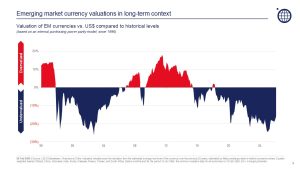

Currencies: a tailwind that most investors have not yet priced

The perception that emerging market currency exposure is a structural drag on returns no longer reflects the evidence in some cases. Across a broad basket of emerging market currencies, valuations sit well below long-term measures of fair value. Importantly, that undervaluation has arrived alongside stronger fundamentals: improved external balances, more credible monetary frameworks, and flexible exchange rate regimes that now absorb shocks rather than amplify them.

At the same time, the US dollar faces headwinds of its own. Elevated valuations, widening fiscal deficits, and rising dependence on foreign capital leave it more sensitive to shifts in confidence than the prevailing consensus assumes. For investors with a long-term horizon, currencies that are already priced for pessimism represent an additional source of potential return, not merely a risk to be managed.

Genuine diversification: increasingly scarce

In an increasingly concentrated global equity universe, diversification has become both more difficult and more valuable. US equities now account for roughly two-thirds of global indices, with the ten largest companies representing approximately a quarter of passive index exposure. Emerging markets offer something genuinely scarce: different economic cycles, different policy dynamics and a correlation of just 0.66 with US equities since 1988—lower than any developed market region.

That said, we are not making the case for broad emerging market exposure. Emerging market indices are themselves concentrated; the pace of change varies from country to country and valuation dispersions remain wide. India, for example, trades at a 100% premium to other emerging markets, on par with shares in the US. This dispersion underscores the limits of treating emerging markets as a monolith.

In this context, selectivity is both a risk management tool and a source of alpha. It allows active investors to hunt in markets where reform momentum, governance improvement, and capital discipline are converging, while avoiding areas where growth remains disconnected from shareholder returns.

Conclusion

The investment case for emerging markets today does not rest on a single argument. It rests on a convergence of conditions: cheap valuations with a skew of potential outcomes that we believe are compelling, structural reforms slowly translating into improving shareholder returns, currencies that are cheap by most measures of fair value, and a diversification benefit that has become genuinely scarce in an era of concentrated global portfolios.

For those willing to look beyond the outdated narratives, we believe emerging markets are home to some of the most attractive long-term opportunities in global equities today.

Explore the opportunity in greater detail

Emerging markets remain one of the most misunderstood and under-owned areas of global equities. In our latest white paper, we examine the valuation gap, reform trends, currency dynamics and investment opportunities shaping the asset class today.

To receive 0.25 Technical Competence CPD points for this article, complete the quiz here.

Disclaimer

This is a marketing communication. Past performance does not predict future results. The value of investments in the Orbis Funds may fall as well as rise and you may get back less than you originally invested. It is therefore important that you understand the risks involved before investing. This report represents Orbis’ view at a point in time and provides reasoning or rationale on why we bought or sold a particular security for the Orbis Funds. We may take the opposite view/position from that stated in this report. This is because our view may change as facts or circumstances change. This report constitutes general advice only and not personal financial product, tax, legal, or investment advice, and does not take into account the specific investment objectives, financial situation or individual needs of any particular person. This report does not prohibit the Orbis Funds from dealing in the securities before or after the report is published.

Additional notes for Australian clients: Equity Trustees Ltd AFSL No. 240975 (EQT) is the issuer of units in the Orbis Funds domiciled in Australia. You should consider such funds’ Product Disclosure Statement (PDS) or Information Memorandum (IM), as applicable, before acquiring or disposing units in such funds’. The PDS or IM can be obtained from www.orbis.com.au.

This information is provided for registered investment advisors and institutional investors and is not intended for public use. Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

Target Market Determinations (TMDs) for the Orbis Funds can be found on our ‘Forms’ page under ‘How to Invest’. Each TMD sets out who an investment in the relevant Fund might be appropriate for and the circumstances that trigger a review of the TMD.