Safe hands on the wheel

Brought to you by Milford. Actively honouring the advice promise to clients through turbulent markets

In this special production

Foreword

As an active manager with a 20-year history, Milford is proud to bring you this selection of insights, from leading financial advisers, on active management and the role it can play for their clients.

The analogy of the navigator is common when describing the role advisers play for their clients, and never has this role been more important. Investing has always been complex and emotionally challenging, but has become even more so in the last few years, where the collision of high inflation, rising interest rates and economic uncertainty have combined to create one of the most treacherous investing landscapes seen for many years.

Helping clients navigate this landscape while progressing towards their goals and dreams takes expertise, empathy, and the right tools. It is clear that one of those tools is active management, strategically applied in a way that can smooth the growth journey and help clients to get a better night’s sleep.

While some are keen to frame the passive and active narrative in a black and white context, (one way versus the other way), the majority of advisers we speak to prefer to skilfully blend both approaches when tailoring portfolios for their clients.

As the research shows, Australia is served by local fund managers who can hold their heads up high amongst international peers, and I am of the firm belief that Australian advisers similarly are world leaders in terms of their knowledge, skills, and service focus.

All of which means the ultimate winners are, of course, clients.

About this paper

This discussion paper is a joint initiative between Milford and Ensombl.

Informed by the insights of six experienced,successful, financial advisers – representing more than 700 clients – this paper explores how clients are being prepared for extended periods of market stagnation and volatility, and why now, more than ever, advisers and clients alike are looking for the ‘safe hands on the wheel’ that effective active investment management can provide.

We would like to thank the following advisers for their participation in the production of this paper:

Executive Summary

- Many people frame the narrative around active and passive management as being about one versus the other

- Most advisers, on the other hand, recognise a blended approach is often required to meet individual client objectives and circumstances

- While alpha may at times be hard to find in the largest markets, research suggests there are certain economic cycles, regions, and sectors, where active management can, and does, shine

- Periods of high inflation and economic uncertainty generally provide more opportunities for alpha, as do emerging markets, real estate, and small and mid-cap sectors

- Australian active managers as a category have consistently outperformed their international peers

- During the tumultuous 2022 calendar year, around 4 in 10 Australian share funds, and 6 in 10 AREIT funds beat benchmark, compared to around 1 in 5 for both over a 10-year period

- On top of market dynamics, financial advisers must also overlay client factors, including individual goals, timeframe, and risk tolerances

- The majority of clients represented by our contributing advisers conform to the loss averse investor type

- Australian research suggests this stereotype is widespread among Australian investors, of all age groups

- The priority for most clients is therefore capital protection, and a smoother growth journey that allows them to sleep at night

- From a portfolio construction perspective, advisers are looking to limit downside losses or drawdowns, even at the expense of some upside capture

- Advisers rely on active management to support this smoother growth trajectory

- Clients are largely benchmark unaware, and typically judge the performance of their financial plan simply in terms of the progress towards their financial and lifestyle goals

- On the topic of fees, while there was an overall imperative to ensure clients received value for money, fee considerations were not the main basis for manager selection

- Not all active managers are created equal, and selecting the right manager is crucial

- The main criteria used by advisers when assessing active managers, in addition to track record, were that they were true to label, and had conviction in their ideas

- Quantitative metrics used to assess this conviction included portfolio concentration, turnover, and tracking error

- There is evidence to suggest that market volatility and elevated inflation could persist over the medium term, and we could be in for an extended period of minimal real asset growth

- In such conditions, the impact of active management is greatly amplified

Introduction

The relative merits of active and passive investing have proved to be an enduring topic within investing circles, evoking passionate arguments, reams of data, and countless academic papers. It is a topic with which financial advisers, as the experts who guide their clients through the complexities of investing, are highly familiar.

The narrative around active and passive investing is framed by many as a black and white debate, where one philosophy or style is pitched against each other in a ‘winner takes all’ battle.

On that basis, superficially at least, there is ample evidence to declare passive investing to be the winner, with long-term outperformance of many well-known benchmarks proving elusive for the majority of fund managers, especially in the US, where the passive (index) investing revolution was born in the 1970s.

But dig a little deeper and a different perspective starts to emerge, one that suggests that the ability of, and opportunity for active managers to outperform benchmarks varies considerably by economic cycle, inflationary regime, region, and asset class. In simple terms, the more volatile and challenging the conditions, the more scope there is for active management to add value.

From a financial adviser perspective, an additional overlay on the active/passive narrative is necessary – that being the need to account for individual client circumstances, objectives, and risk preferences.

For the majority of advisers, these considerations typically distil down to an investment philosophy that blends elements of both active and passive, reframing the narrative more around optimising that blend, rather than choosing one or the other.

The economic reset that has occurred since Covid has made investment markets more complex, and treacherous, than they have been for decades. High inflation, rising interest rates and falling consumption have eroded business and consumer sentiment to their lowest level in years.

Evidence strongly suggests these conditions – conditions which not only favour, but virtually demand, a more active approach – could prevail for years, not months.

1. Active Management in Detail

The high-level view

S&P Indices versus Active (SPIVA) scorecards are semi-annual reports published by S&P Dow Jones Indices that compare the performance of active equity and fixed income funds against their benchmarks over different time horizons.

They are widely accepted as the report card for active managers as a collective.

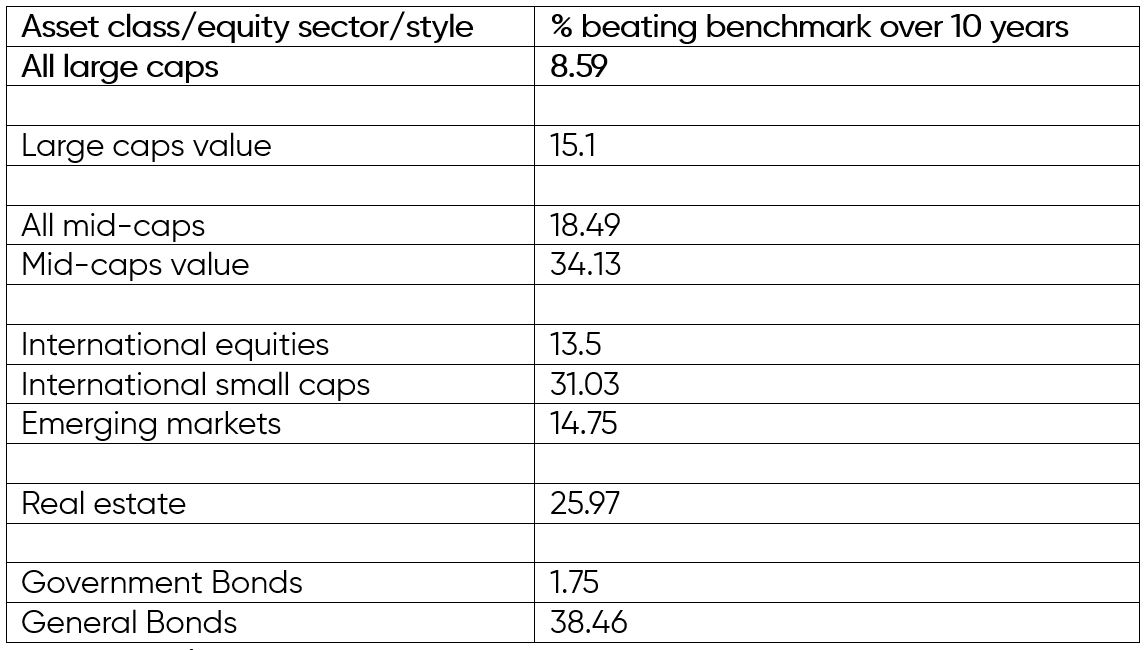

For many years now, the report card has typically found passive/index investing to be top of the class, especially in the US large caps category. Certainly, the report1 covering the 20 years ended 31 December 2022 contained no surprises, with less than 1 in 10 active managers beating benchmark over 10- 15- and 20-year periods.

US Active Large cap funds beating benchmark to end 2022

Adviser insight: access to information now less of a competitive advantage

“Fund manager research was once a differentiator, but these days, information is so freely available that its value as a point of competitive advantage has diminished, especially when you are talking about bigger markets and bigger companies.” Marisa Broome

But a deeper dive tells a different story

The same SPIVA scorecards tell a different story when we look at different time periods, different asset class sectors, and different regions.

Cycle differences

Intuitively, active managers are able to optimise their exposures in response to market turbulence, and this is borne out by the data.

If we continue to look at the data2 for US large caps for example, the figures for 1 year (being the disastrous 2022) and 3 years (taking in the Covid crash and subsequent recovery) show that active funds were far more successful, with nearly half of all managers (48.9%) beating benchmark over 1 year, and one quarter (25.73%) beating benchmark over 3 years.

US Active large cap funds beating benchmark to end 2022

In an exercise undertaken by US manager Hartford Funds3, based on Morningstar Large Cap data, they demonstrated that across the 27 market corrections since 1990 – including that occurring in August 2022 – active outperformed passive through 20 of those corrections.

Adviser Insight: volatility creates opportunity

“Volatile markets can lead to mispriced assets, which creates the opportunity to actively add value.” Anne Graham

Adviser insight: willingness to be educated is key when using active managers

“Understanding the individual managers used is critical, so If someone shows they want to be educated, and they have the right risk profile, I may look to introduce more active management, particularly for those asset classes that have demonstrated they are less efficient, and active management can be more helpful in producing alpha or reducing risk”. Callum Glasby

Sectoral, style, and regional differences

Sticking with the US markets, and continuing to use the 10-year period as a reference point, we can see active management also starts to add more value across different investment styles, equity sectors, and regions.

This intuitively makes sense.

Once you look beyond large caps in markets as big as the US, companies are not as well researched or covered by data history, and the likelihood of asset mispricing is therefore higher.

This in turn means more opportunity for active managers to add value.

In emerging markets, buying the index may come with a heightened risk of including companies of dubious quality, and the quality filtering role played by managers actively selecting stocks and sectors can make a bigger impact.

Non-government fixed interest securities, to the extent that they involve more risk, also offer more scope for alpha.

Adviser insights: Vigilance around fixed income favours an active approach

“I have a lot of retiree clients, and I have far more comfort with active management in the fixed income space, where managers can be more vigilant around portfolio duration when managing interest rate risk.” Callum Glasby

Adviser insights: active managers act as a quality filter when there is uncertainty

“In emerging markets, or even a market like China, buying the index means you might be getting a lot of companies that you don’t know a lot about. An active manager who is on the ground, understanding these companies, can act as a quality filter.” Sean Dunne

Table 1: Active performance – sectoral differences

Source: SPIVA4

Regional differences

Active managers also appear to be more successful outside of the US, (possibly explained by how saturated the US market is with research, and the challenges of investing in high growth US tech ‘mega-caps’, which can effectively turn managers into quasi-index trackers.)

Data for the 10 years ending December 2021, from AJ Bell5 in the UK, found that:

- 85% of all UK active funds outperformed their benchmarks, compared to

- 64% of European funds

- 63% of Asia Pacific Funds (excluding Japan), and

- 22% of US funds.

Many Australian active managers have excelled

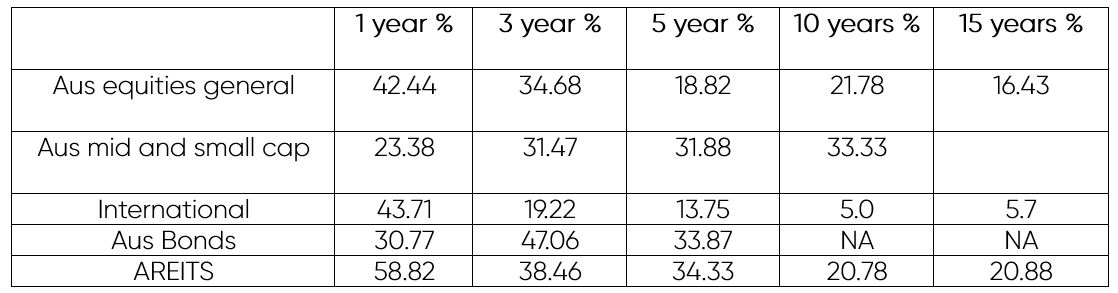

Bringing it all together, the SPIVA scorecard for Australia6, across different sectors and time periods, reinforces the point that there are plenty of active managers who have added alpha, especially through the extreme disruption and dislocation experienced by markets post covid.

Indeed, for the calendar year 2022, one of the most tumultuous in recent memory for both equities and fixed interest, the proportion of funds beating Australian indexes was in the following ranges:

- 1 in 4 for small caps

- 1 in 3 for bonds

- 4 in 10 for Australian and international equities, and

- 6 in 10 for AREITS managers.

Table 2: Australian active funds beating benchmark, period ended 31 Dec 2022 (absolute returns)

Source: SPIVA

Adviser insight: ability to quickly exit from problem situations is critical

“You can’t expect managers to magic returns out of a stagnant market, but you can expect that when things turn pear shaped, they can dump out of things more quickly.” Sean Dunne

2. Client and Adviser considerations

The specific challenges of investing during times of high inflation

Elevated inflation – as we are currently experiencing – creates another layer of risk for investors, reducing real rates of return and eroding the spending power of those on fixed incomes (such as retirees). The policy responses associated with inflation, especially interest rate increases, can also drive heightened volatility in both equity and fixed interest markets, making them even tougher to navigate.

From an asset mix and sector selection perspective, making a portfolio more resilient against inflation is likely to involve tilts towards commodities, energy, and infrastructure.

Studies also suggest a more active approach is also necessary during such periods.

One academic study, based on 95 years’ of US market data, found that trend-based active strategies focusing on equity, bonds, foreign exchange, and commodities have typically provided an impressive level of protection in times of high inflation.

The same study concluded that:

“Active, factor-based strategies performed far better than passive investments – in stocks or bonds – during periods of high inflation”.

Concentration risk can also undermine an indexed approach

The extent to which a market index is concentrated – and in what sectors – can be a significant driver of performance outcomes.

As an example, the S&P 500 is heavily concentrated in the technology sector, with 7 of the top 10 stocks in the index currently being tech related. A decade ago, this top 10 (which only accounted for 18% of the total capitalization, compared to around 30% now) was far more diverse, comprising only three technology stocks, alongside two oil companies, and an assortment of telcos, banks, and pharmaceutical companies.

This concentration applies at a global level, with the top 10 US Stocks also accounting for more than 20% of the MSCI world index (as at 1 September 2023).

The concentration into technology stocks (albeit quality ones) means the index may not be best placed to absorb the impact of inflation and as such may be expected to underperform in inflationary periods.

Australia’s main index, the S&P/ASX 200, also has a concentration issue – with 5 of the top 10 companies in the index being banks, not noted as an inflation resilient sector.

Adviser insights: smart beta as a way of reducing concentration risk in global equities

“Smart beta, which combines active and passive elements, can be an effective strategy, and it’s one I regularly use to help lower the concentration risk in US equities.” Callum Glasby

Adviser insight: Concentration risk – S&P 500 feels like the S&P 10

“Concentration risk has become an issue globally, so trying to keep up with benchmarks may result in too much risk for many portfolios. With recent valuations spikes the S&P 500 is looking more like an S&P 10 and I would argue there is more value in the other 490 and trust quality active managers to find it.” Richard Elmes

Overlaying client factors

In addition to considering market dynamics and broader economic context, advisers must also overlay client specific factors when considering the role for active management. These factors can include, but not be limited to:

- Lifestyle and financial goals

- Risk tolerance and risk capacity

- Investment timeframe

What clients want in an adviser

The value of advice is a much researched, frequently discussed topic. Various surveys have highlighted a range of attributes of advice – and advisers themselves- that clients value the most.

In research studies conducted by ASIC8 (Report 627) in 2019, and the FPA9 (now FAAA) in 2022, the importance of the financial adviser as an expert guide, helping clients navigate a challenging landscape, towards their goals, was evident.

Table 3: Top reasons for engaging a financial adviser (ASIC REP 627)

Source: ASIC

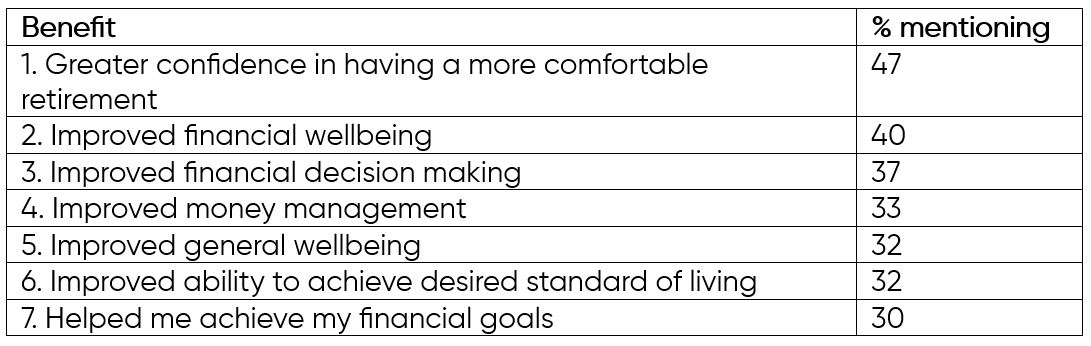

Table 4: Top benefits clients realise from financial advice relationships

Source: FPA

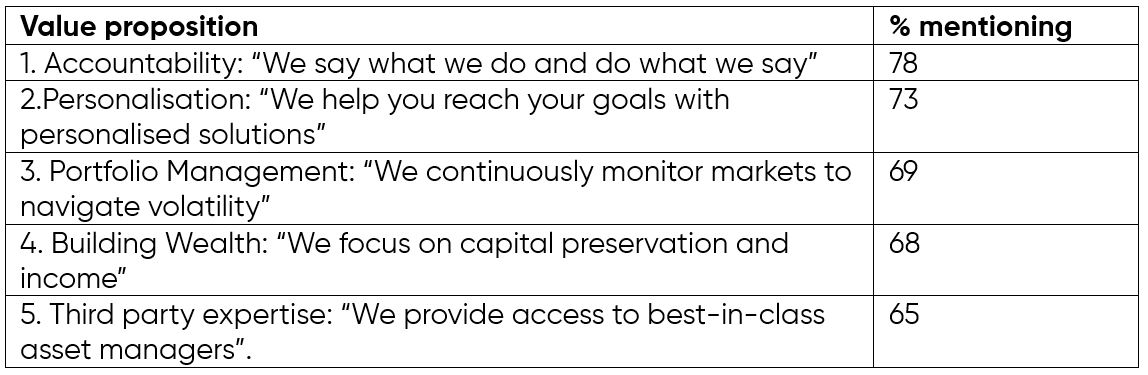

Attempting to understand the value advice from another perspective was a US study10, which asked higher net worth advice clients to rank the advice value propositions which resonated the strongest.

Table 5: Top rated adviser value propositions (US)

Source: Pershing, Harris Poll

Three points are clear from these studies:

- Clients are not engaging financial advisers to chase investment performance, they are looking for help to achieve their higher goals (lifestyle and financial)

- Navigating volatility and preserving capital is far more important than chasing the highest possible investment returns

- Clients recognise that advisers have expertise and access to opportunities that can help them achieve their goals.

Adviser insights: value of advice is not about investment performance

“Our focus is on getting the strategy right and solving client problems. They see us as having the knowledge and connections to bring in the right experts.” Marisa Broome

“My job is to prudently manage a client’s assets to achieve their goals while ensuring they can sleep at night.” Sean Dunne

“Our advice is largely around strategy and structure. Investments is an important facilitator, or a by-product, but it’s not why they engage us.” Anne Graham

Adviser insight: personalisation is key

“You can’t just grab a solution that worked for the last client and move it on to the next. You have to start with a blank canvas every time.” Callum Glasby

Loss aversion

The importance of the ‘safe hands on the wheel’ provided by financial advisers in turbulent markets is underpinned by the ‘loss aversion’ behavioural bias exhibited by many clients.

Simplistically, loss aversion means that individuals feel the pain of a financial loss far more than they enjoy a financial gain of equal value. According to Nobel Prize winning economists Kahneman and Tverskyy11, for any given amount, losses hurt twice as much as a gain of the same amount.

Adviser Insights: clients feel the losses more than the gains

“Not many clients would call to congratulate their Adviser for delivering a big upswing in performance, but if the market takes a nosedive, the phone doesn’t stop ringing.” Sean Dunne

“Loss aversion is extremely evident with the vast majority of clients I speak to.” Callum Glasby

Loss aversion can result in several sub-optimal investment behaviours:

- Avoiding risk, which can in turn see an overly conservative investment approach incapable of delivering the returns needed to achieve their objectives

- Selling assets at the worst time possible (during a downturn)

- Holding onto investments that should be disposed of, purely to avoid a loss.

Adviser insights: preventing poor client decision making

“We tell our clients we will manage their portfolios for the long term, through good and bad markets. There will be up years and down years, but importantly we will stop them making decisions they will regret.” Anne Graham

Economists Shlomo Benartzi and Richard Thaler extended the work on loss aversion to include other related behaviours, including the frequency with which investors checked the value of their portfolio.

Their seminal work on this topic, “Myopic Loss Aversion and the Equity Premium Puzzle”, concluded that loss aversion became more pronounced the more frequently investors checked the value of their portfolio12. The same study also found that individual investors were largely unwilling to accept variability of returns even if the short-run returns have no effect on immediate consumption.

This inherent conservatism is certainly reflected in research. And interestingly, isn’t limited to older investors.

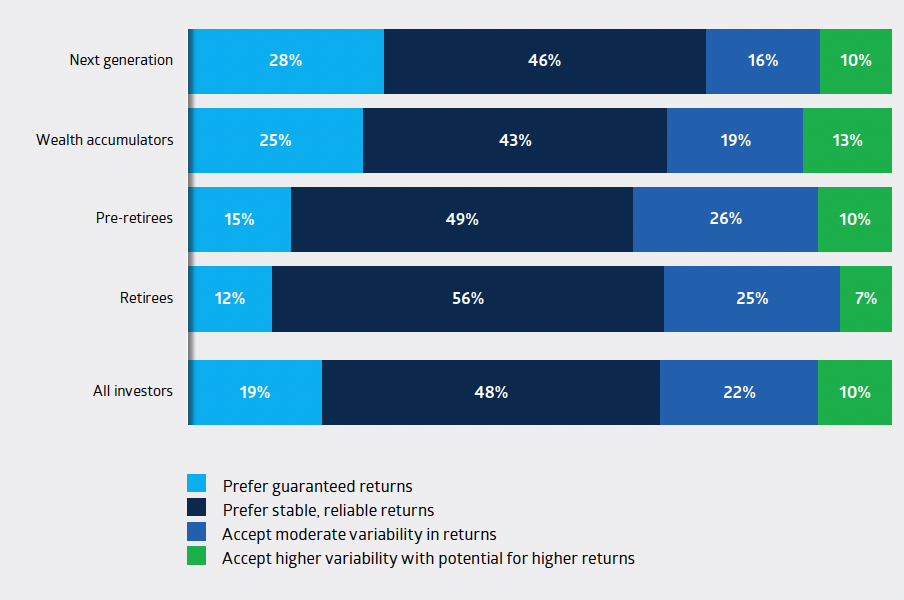

In Australia, the 2023 ASX Investor Study13 found that even younger investors preferred guaranteed and stable returns over higher risk/higher return scenarios

Figure 1: Attitudes to investment risk by investor generation (Australia)

Source: ASX

Australian retirees not prepared for losses of 10% or more

Unsurprisingly, retirees exhibited a strong preference for stability and predictability, a point reinforced by 2018 research14 released by National Seniors Australia.

Their study of 5,000 members found:

- 23% could not accept any annual loss on their portfolio

- Around 40% could only accept 5% or less

- Only 7% could tolerate a loss of 20% or more

Applying a real-world perspective on this, between 1920 and mid-2022, there were 46 market falls of 10% or more15. Almost one third of these (15) have occurred since January 2000.

Are most investors unsuited to the passive index rollercoaster ride?

Adopting a buy and hold, passive indexed strategy means buying into all the ups and downs of that index. Even for those with a long-term investment horizon, this can take extreme discipline. It also means handing over any sense of control over their investments.

The reality is that many clients do not behave in this way.

Adviser insights – investing is emotionally challenging

“We have observed that clients are far more interested in absolute returns during a market downturn and become more interested in relative returns during market upswings. Our objective is to manage both conditions for a client.” Anne Graham

“A lot of my clients are high net worth entrepreneurs who are used to having a sense of control, and they need to feel a sense of strategy and control around their investments also.” Sean Dunne

“I feel like half my job is managing clients’ emotions.” Andrew Foo

Risk capacity can also limit downside tolerance

Risk profiling is an essential (and mandatory) component of the advice process. Using either psychometric or revealed preference methodologies, advisers are able to gain an understanding of a client’s attitudes towards risk.

Often, this attitude towards, or tolerance for risk (expressed in terms of conservative, aggressive etc) is seen as the fundamental determinant of investment strategy.

But this is problematic for two reasons:

- The mere fact a person can tolerate aggressive investment risk does not mean they should be placed in aggressive investments (a point made clear by ASIC and AFCA)

- A person may be able to emotionally tolerate risk, but not have the financial capacity to take it.

In simple terms, even investors who are able to mentally cope with risk, may not be able to afford to take it.

Adviser insights: risk capacity more important than tolerance

“A client’s risk capacity is far more fundamental to me than their risk profile. Just because they can emotionally tolerate risk, doesn’t mean they can financially afford to take it.” Richard Elmes

Investment objectives and timeframes

THE FUNDAMENTAL BUILDING BLOCKS AROUND WHICH FINANCIAL PLANS ARE BUILT, ARE THE ULTIMATE GOALS AND OBJECTIVES OF THE INDIVIDUAL CLIENT.

These could be lifestyle goals and/or financial goals. They could be short, medium, and long term in nature.

The intersection of those goals with the client’s circumstances means the road to meeting those objectives will almost certainly be unique.

When building a financial plan, advisers will need to determine the product selection and asset allocations that will maximise the likelihood of meeting the client’s goals. Where the objectives can reasonably be met within the client’s

risk profile, advice becomes a fairly straightforward process.

But things don’t always run smoothly.

Timing issues may require investing more aggressively than the client can either emotionally tolerate, or has the capacity to afford. For example, someone closing in on retirement needs to be thinking and investing 20 – 30 years ahead, but doesn’t want to kick off their retirement recovering from a market downturn.

Adviser insight: timing issues can make an indexed approach riskier

“A 50-year old may have 10-15 years to retirement, and indexing into a growth strategy may feel like a good low cost idea, but if we get a 20% correction to the index and a multi-year recovery, that can hurt retirement plans. For a retiree, the risk is greater, with longevity risk and sequencing risks additional factors.” Richard Elmes

“In inflation adjusted terms, there are multiple examples from the US and Europe where it took markets decades to return to previous peaks.” Marisa Broome

Unique client circumstances and goals mean some level of active is almost always needed

Taking into account the highly individual nature of a client’s goals, timeframes, risk tolerance, and risk capacity, there would be very few clients for whom a purely passive approach to investing is appropriate. Some degree of active management will almost always be necessary and preferred.

Adviser insights: measuring progress towards goals, rather than against benchmarks

“Clients’ objectives don’t typically revolve around investment benchmarks, they revolve around their life dreams and circumstances.” Andrew Foo

“Market benchmarks and indices have little relevance to clients. What’s more important is their progress towards the goals enshrined in their financial plan.” Marisa Broome

“We judge returns in the context of the client’s goals.” Sean Dunne

“The adviser is in the driver’s seat to set the narrative, and I will always link the review back to their goals. With retiree clients and income-based goals, their reference point is absolute returns to deliver their income needs, not returns against a benchmark. Callum Glasby

Choosing a Manager

Advice and investment philosophies

A growing number of Australian financial advisers are recognising the importance of having a formal, documented investment philosophy.

An investment philosophy is a north star, a set of beliefs and principles that guide an adviser’s investment decision making. As such, there is a nexus between an adviser’s investment philosophy and advice philosophy, and both are integral to the overall advice proposition.

The building blocks of an investment philosophy can include:

- Beliefs about whether markets are efficient or inefficient

- Your own investment skills and resourcing

- Your ideal clients

- Your advice philosophy

Philosophies which blend active and passive elements are common

As mentioned above, the clients for whom a purely passive approach is both appropriate, and acceptable, are likely to be in the minority, and certainly among the advisers we spoke to, a blended approach incorporating some passive elements, alongside a dynamic (active) approach to asset allocation, was typical.

Adviser insights: investment philosophies typically blend active and passive

“We aren’t an ‘either or,’ it’s horses for courses, although a more active approach is our starting point for most clients, and that’s about being able to adapt the portfolio to the conditions of the time. I’d say about 80% of our total FUM is actively managed.” Anne Graham

“My philosophy is based on dynamic strategic asset allocation. I believe strategic asset allocation is the main driver of long term returns but I like the idea that a manager can be responsive enough to take opportunities along the way.” Sean Dunne

“From 2021 as interest rates reached zero, we became concerned about duration risks in defensive investments, valuation, and the concentration risks in major equity markets as a sharp ‘v’ shaped recovery from the pandemic market shocks, fuelled by stimulus unfolded. We decided to shift away from multi-asset index exposure for retirement and balanced portfolios and moved to an active and more defensive core strategy. This transition protected client portfolios from the drawdown in defensive indices as rates increased impacting duration positions and enabled equity portfolios to focus on quality and valuation of assets. . 90% plus of our total client FUM would be actively managed.” Richard Elmes

“To do all the work to understand a client’s risk profile, and then give them a ‘set and forget’ portfolio based on some formula, isn’t, in my opinion, good enough, and it’s not why they are paying for our help.” Marisa Broome

Adviser insight: passive means being prepared to receive what the market delivers

“Our philosophy revolves around strategic asset allocation as the main driver of returns. I have the active/passive conversation with every client and tell them there’s a place for both. If you are happy to receive exactly what the market delivers, and it is consistent with you achieving your goals, then a purely passive approach can work. But most clients would probably require a mix.” Callum Glasby

Fees don’t matter to clients, value does.

A major driving force behind the take up of passive indexed investing has been cost. Typically done through ETFs (themselves a lower cost structure), the buy and hold nature of indexed funds means far less turnover, translating into a lower cost structure. In some cases, the difference in management costs range from 50 to even 70 or 80 bps.

But for the advisers we spoke to, what matters most to them – and their clients – is value offered for those fees, rather than their absolute quantum.

Their common observation was that many new clients had a vague appreciation of the importance of fees – courtesy of the highly effective and long running ‘compare the pair’ industry super campaign – but they generally lacked any context. They certainly didn’t come with any preconceived ideas or understanding of what fees they may need to pay. Nor was it normal for clients to express a view on the fees associated with any investment recommended to them.

Fee budgets or targets – to the extent that these are used – are not client or licensee mandated, but typically become relevant for clients with existing investments, where Best Interests Duty might see advisers aim to deliver a solution with matching fees.

Adviser insights: the fee conversation is about value, not manager choice

“The long running ‘compare the pair’ campaign has given many people at least an awareness of the importance of fees, which is why we spend a lot of time educating about the importance of net returns. Low fees don’t help if the performance is bad.” Anne Graham

“We would very rarely get objections to fees, either our own, or the managers we use. They want to understand what they are paying for and why. Fundamentally all the clients care about is the value, and frankly, paying 1% to access the global expertise and hard to find opportunities offered by fund managers is exceptional value.” Richard Elmes

“I charge flat fees, based on the amount of attention the client needs. I’m not a fund manager so I don’t tie my fees to investment performance, nor do I make manager decisions based on any perceived client pressures to find the cheapest path; I choose managers who I believe can do the best job.” Sean Dunne

“The cheapest (indexed) path will often come with the most volatility, which is typically not what clients want.” Andrew Foo

Adviser insights: Best Interests Duty ensures an adviser focus on value too

“Product replacement advice is a focus point when it comes to satisfying our best interests duty. Finding a superior offering for a lower cost is preferred but not always possible. As the great man (Buffet) says ‘price is what you pay, value is what you get’. I apply this mantra to manager selection and always ensure I have strong evidence supporting the competitiveness of each asset in the portfolio.” Callum Glasby

“You do get the occasional client who raises the issue of manager fees, perhaps because they remember the advertising or they have had a golf club conversation, but they don’t relate that to an active or passive approach, just an overall sense of value, which is something I need to focus on anyway to act in their best interests.” Marisa Broome

Risk management and capital preservation is the core client need

The consensus view among the advisers we interviewed is that the majority of clients were suited – emotionally and objectively – to a strategy designed to capture much of the market upside (75-80%), while limiting the downside.

This smoothing of the journey – which can be achieved with a blend of active and passive strategies – offers clients the opportunity to achieve the growth necessary to reach their goals, while still being able to sleep at night.

Adviser insights: Clients want safe hands on the wheel and a smooth journey

“Clients come to us to help them navigate their way through a complex and confusing financial landscape, towards their lifestyle goals. Exposing them to the full ups and downs of the market, on the basis that history says they may be better off in the long-run, isn’t good enough. You may as well say ‘you’re on your own’.” Marisa Broome

“The road ahead looks very rocky. A steady growth story that may miss the peaks but limits the downside can help clients sleep at night – that’s priceless.” Richard Elmes

“Our focus is on risk management. We aren’t looking to shoot the lights out for clients, we would much rather limit the downside. We certainly dissuade them from any notion that we will be picking winners.” Anne Graham

“I’m not necessarily looking for managers to pick winners, I’m looking for them to act as a gatekeeper, to filter out the rubbish.” Sean Dunne

“It sounds boring, but we genuinely focus on what clients want, which is long term consistent returns and capital protection.” Andrew Foo

The upside of downside protection

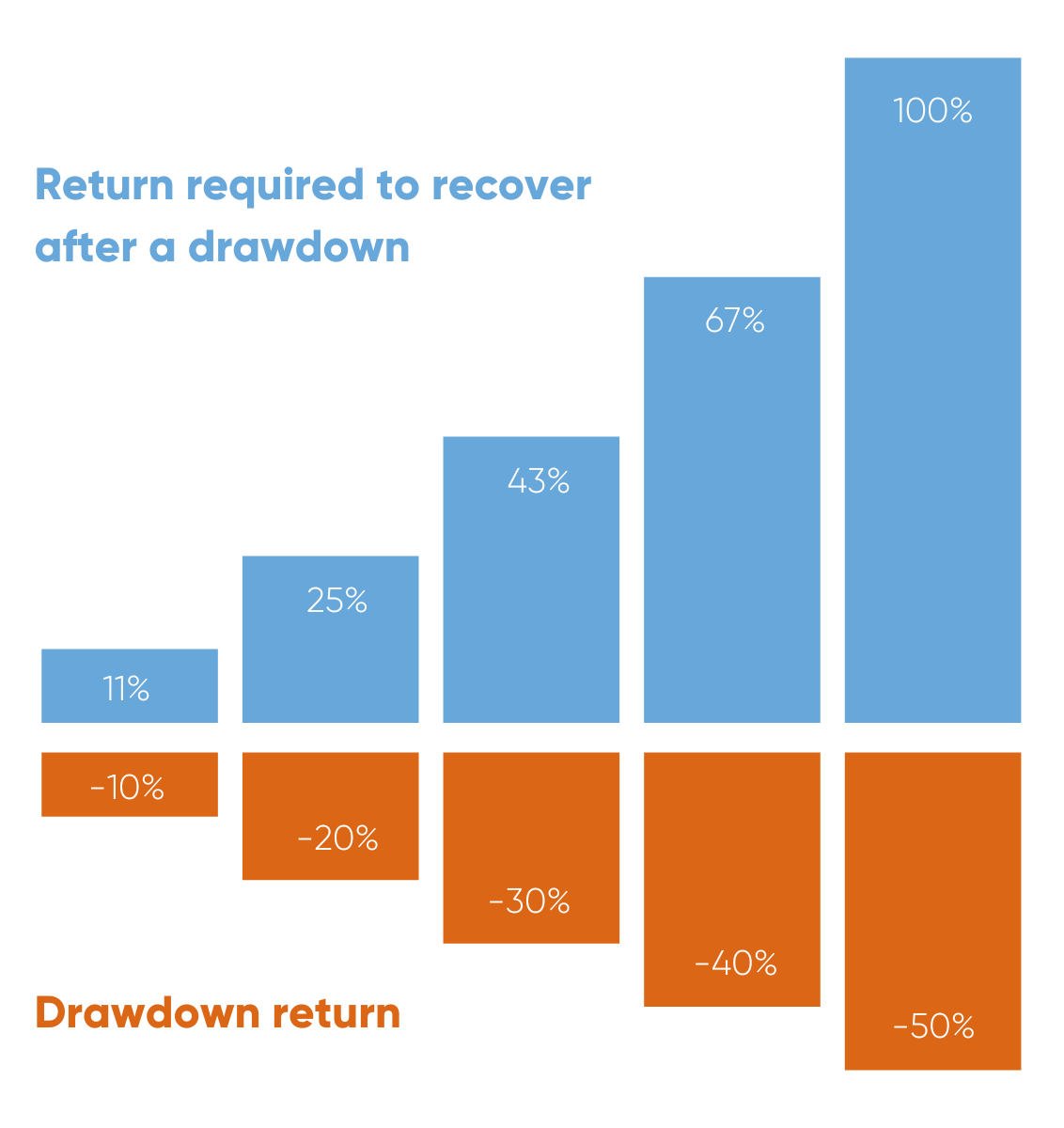

Aside from the emotional benefits of a smoother investment journey, simple mathematics demonstrates the powerful benefits of limiting downside losses.

As shown in Figure 2 below, limiting losses or drawdowns means you need a lower upside return to recover.

Figure 2: Returns needed to recover from downside loss

Source: Milford

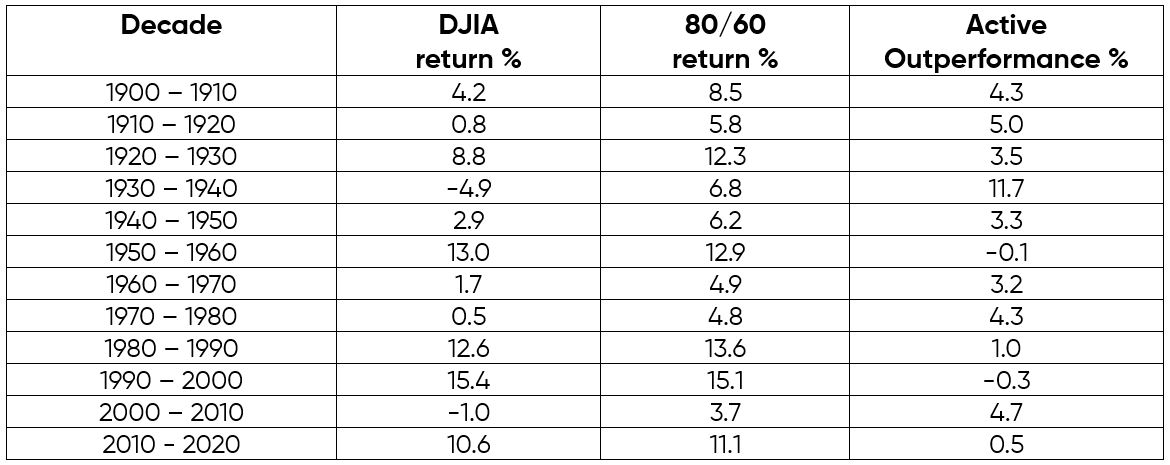

Long term historical data reinforces how such an approach can deliver superior returns to the market benchmark. Table 7 compares the performance of a theoretical 80/60 portfolio (one that captures 80% of market upside but only 60% of any downside) over the last 100 years.

The downside protected portfolio outperformed the index (in this case the Dow Jones Industrial Average) in 10 out of 12 decades16.

Table 7: 80/60 applied to 120 years of DJIA returns

Source: Dow Jones, SSGA.

Adviser insight: limiting the drawdown has a significant impact on subsequent returns

“You get worried for clients – it is harder to recover when you are taking 100% of a market drawdown than it is when you are giving away some of the short term returns for longer term benefit. If you can invest in managers who can minimise the drawdowns, the following year’s returns will be far superior.” Richard Elmes

“The maths around the importance of downside protection are simple and compelling. You lose 50%, you need to make 100% just to get back to the same point.” Andrew Foo

3. Macro Outlook

Are current market conditions conducive to a more active approach?

As much as many would like to think that the peak of market volatility and inflation is very much in the rear-view mirror, there is plenty of evidence to suggest the outlook for markets over the medium, and even long, term is one of stagnancy, volatility, and inflation, effectively meaning real asset growth will be much lower than we have experienced for quite some time.

This is borne out in both adviser sentiment, and in hard data.

Adviser insights: short to medium term outlook is very challenging

“The decade following the GFC was the best decade in history for investors, significantly driven by the rocket fuel of fiscal and monetary policy. But everything in the macro landscape now points to risk. Concentration risk. Valuation risk. Exchange rates mean that US stocks – already at unprecedented valuations – are even more expensive. Markets should be taken with a pinch of salt, and aren’t to be trusted. Being exposed to 100% of any movements doesn’t make sense, especially now, when the facts of the real economy say we should be cautious.” Richard Elmes

“Treacherous is the perfect word to describe how I see the markets in the short term, and

I’m sitting on lots of cash for clients for just this reason, even though it means inflation is eating into their real returns. But markets move in cycles, and I’m optimistic about the medium term. I do think we still start to see a shift in where those returns are found, with the impact of decarbonisation to be felt in all sorts of ways.” Marisa Broome

“I don’t see the favourable conditions we experienced in the last decade are coming back any time soon – it was a perfect storm (in a good way) and in my view, unlikely to be repeated for quite a while.” Anne Graham

“I think the market choppiness will persist for at least the next 12 months, and even though it may have peaked, I expect inflation to remain above the RBA’s target range for quite some time.” Andrew Foo

“The relationships between a lot of macro factors have proven weaker and less predictable than in previous cycles, which makes portfolio decisions more challenging.” Callum Glasby

Historical periods of low asset growth

In contrast to an almost 15-year bull run experienced by equity markets between 2008 and 2022, many market indicators are pointing to an outlook last seen in the late 1960s (and which lasted for several decades).

Between 1972 and late 1979, in a world characterised by persistent inflation and economic uncertainty, the S&P500 was basically unmoved, meaning growth of the index over that 7-year period was zero (with lots of volatility in between).

Figure 3: S & P 500 over time

Source: Bloomberg

When we look at real asset growth, by taking inflation into account, the picture is even more alarming.

As can be seen from the chart below, real asset growth was zero or even negative, between the mid 60s and the mid 90s – a period of 30 years!

The current outlook has a similar look and feel

Several factors are at play that could point to a similarly extended period of inflation, market volatility, and low or negative real asset growth.

- The ageing population will see more competition for labour, feeding into higher wages and inflationary pressures

- The multi-trillion-dollar expenditure by governments around the world, to meet decarbonisation targets, will also be inflationary

- Geopolitical uncertainty will continue to cast a shadow over international trade as the focus on self-dependency grows

- Mega-tech valuations continue to race ahead of profits, leading to a potential bubble

- US Fed Chairman, Jerome Powell, has declared the Fed’s readiness to do whatever it needs to do to bring down inflation, meaning rates could stay elevated for an extended period

Real asset growth – the medium to long- term outlook

The investment team at Milford believes there is a reasonable risk that the combination of current forces at play will manifest as an extended period of low asset growth.

Under that scenario, equity returns could be as low as 6% over the next decade, set against an inflation rate of 4%, giving a real return of just 2%.

In such a landscape, active management not only tends to shine, but its proportional impact is also greatly magnified.

An alpha of 2% on top of a real return of 2% effectively doubles the real rate of return, an effect which obviously compounds over time.

4. Choosing a Manager

Criteria for assessing active managers

A critical aspect of introducing active management into client portfolios is manager selection. History and data has laid bare the fact that plenty of active managers still fail to add value.

What then, are some of the criteria by which active managers can be assessed? Two of the key indicators of good active management from analysis by the US-based Chartered Financial Analyst Institute17 are:

HIGH CONVICTION

Research suggest active managers are more successful when they overweight their high conviction investments. Having too many ‘high conviction’ investments, paradoxically may indicate a lack of conviction. A fund with more than 20 concentrated positions may well be a red flag to investors.

HIGH TRACKING ERROR

A low tracking error could mean a manager is taking a quasi-indexed approach, constrained by perceived commercial pressures. A high tracking error means a manager is actively looking for alpha.

Despite the common perception that high tracking error is associated with higher risk, in actual fact a study18 of Australian active funds showed it was the low tracking error funds that performed more poorly during market downturns. For those funds, the desire to minimise tracking error constrained their ability to position the fund differently from the benchmark.

Adviser insights: how advisers select active managers

“For me, it’s important a manager does what they say on the tin.” Sean Dunne

“I really want to understand a manager in terms of their team members, their experience and history, whether there is any key person risk. What’s most important to me though is that they have conviction.” Marisa Broome

“I look for managers to demonstrate valuation awareness. And I will look at specific holdings, rotation, tracking error, whether they are benchmark aware. What’s their philosophy, and how are the executing against it? We are lucky in that the last three years have put managers through their paces more than the previous 15.” Richard Elmes

“Not all active managers were created equal. A performance track record is obviously important, but what’s more important to me is the philosophy, style, and strategies underlying those returns.” Andrew Foo

Summary

While some observers like to frame the narrative around active and passive management as competition that pits one against the other in an ‘all or nothing’ battle, the reality is that most financial advisers embrace a philosophy that blends active and passive strategies for clients. Within that active component, advisers will further seek to blend different manager styles.

While the nature of this blending varies by individual client characteristics and circumstances, and by market conditions, it is clear that an overarching priority to preserve capital amongst many Australian advice clients sees an emphasis on ‘smoothing the journey’, with portfolios primarily built to reduce downside losses, while still capturing healthy upside growth. Active management is critical to such strategies.

Extensive research shows that active management can be particularly effective in periods of high inflation and market volatility, and there is strong evidence suggesting the medium-term outlook is for an extended period of low real asset growth – conditions in which the value of active alpha is greatly amplified.

While advisers and clients seek comfort from the ‘safe hands on the wheel’ that active managers can provide during periods of turbulence anduncertainty, the quality of the individual managers is critical, with advisers favouring those managers with a well defined philosophy – implemented with clear conviction – ahead of those who are highly correlated with benchmarks/indices and therefore offer questionable value.

1. https://www.spglobal.com/spdji/en/documents/spiva/spiva-us-year-end-2022.pdf

2. https://www.spglobal.com/spdji/en/documents/spiva/spiva-us-year-end-2022.pdf

3. https://www.hartfordfunds.com/insights/market-perspectives/equity/cyclical-nature-active-passive-investing.html

4. https://www.spglobal.com/spdji/en/documents/spiva/spiva-us-year-end-2022.pdf

5. https://www.forbes.com/uk/advisor/investing/passive-investing-vs-active-investing/

6. https://www.spglobal.com/spdji/en/documents/spiva/spiva-australia-year-end-2022.pdf

7. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3813202

8. https://download.asic.gov.au/media/5243978/rep627-published-26-august-2019.pdf

9. https://fpa.com.au/news/australians-who-engage-a-financial-planner-have-a-better-quality-of-life-fpa-launches-inaugural-value-of-advice

10. https://proactiveadvisormagazine.com/advisors-explain-benefits-active-management-clients/

11. https://en.wikipedia.org/wiki/Loss_aversion

12. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=227015

13. https://www.asx.com.au/content/dam/asx/blog/asx-australian-investor-study-2023.pdf

14. https://nationalseniors.com.au/uploads/07183036PAR_OnceBittenTwiceShy_Web_0.pdf

15. https://www.firstlinks.com.au/market-fall-reveals-risk-tolerance-loss-aversion

16. State Street Global Advisors. Active Management of Downside Risk During Long Market Cycles. September 2022.

17. https://blogs.cfainstitute.org/investor/2020/03/11/good-vs-bad-active-fund-management-three-indicators/

18. https://obj.portfolioconstructionforum.edu.au/articles_perspectives/PortfolioConstruction-Forum_SSGA_Tracking_error_causes_short-termism.pdf

Disclaimer: This whitepaper is intended for financial advisers and it is intended to provide general information only. It does not take into account your investment needs or personal circumstances. It is not intended to be viewed as financial advice. You should not rely on any information in this communication in making financial decisions. Before making financial decisions you may wish to seek financial advice. Equity Trustees Limited (“Equity Trustees”) (ABN 46 004 031 298), AFSL 240975, is the Responsible Entity for the Milford Australia funds. Equity Trustees is a subsidiary of EQT Holdings Limited (ABN 22 607 797 615), a publicly listed company on the Australian Securities Exchange (ASX: EQT). Milford Australia Pty Ltd ABN 65 169 262 971 (AFSL 461253) has prepared this advertisement as investment manager of the Milford Australia Funds. Please read the relevant fund’s Product Disclosure Statement at milfordasset.com.au. Past performance is not a reliable indicator of future performance. The Milford Investment Funds Target Market Determinations are available at milfordasset.com. The Target Market Determination is a document describing who a financial product is likely to be appropriate for (i.e. the target market), and any conditions around how the product can be distributed to investors. It also describes the events or circumstances where the Target Market Determination for this financial product may need to be reviewed.