Ferrari is one of the world’s most iconic brands. It’s also an amazing stock. Ferrari was founded in Italy in the 1940s and was spun off from Stellantis in 2016 under the ticker RACE IM.

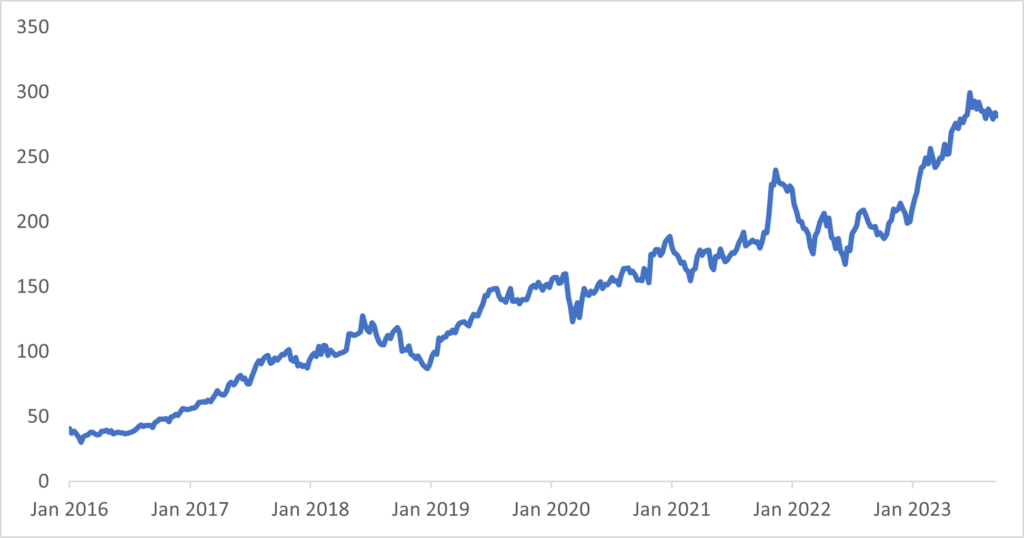

The IPO price was EUR43 and Ferrari is currently trading at ~EUR300 for a 600% return since listing. The analysis below outlines the Case for RACE and highlights 4 main reasons to why we love the stock.

RACE Stock Price Since Listing in 2016

Reason #1: High margin, high return, high growth business

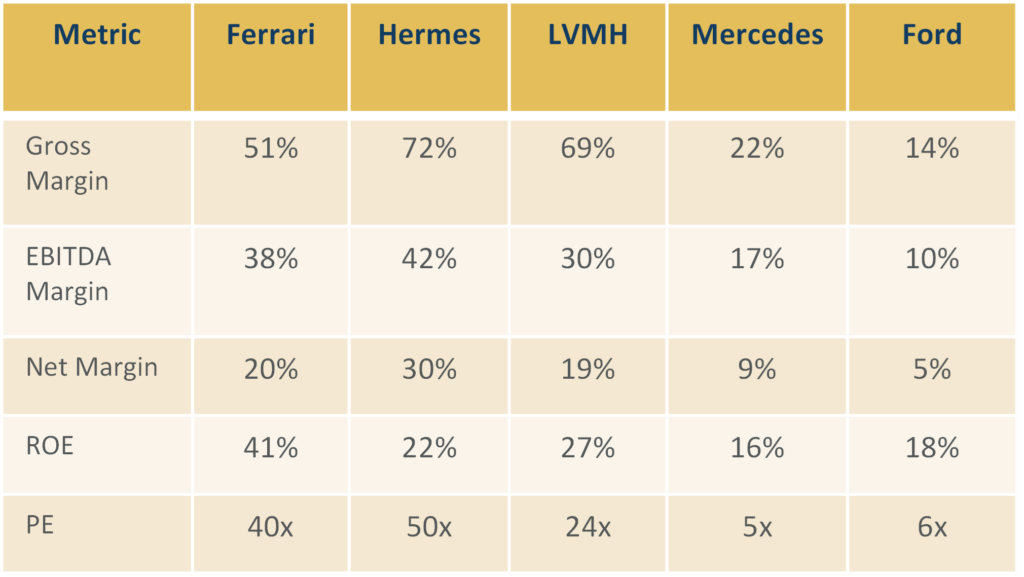

Ferrari has achieved the holy trinity of high returns, high growth and a reasonable valuation. RACE boasts gross margins of ~50%, net margins of over 20% and an ROE of approximately 40%. This margin and non-cyclical earnings profile is why Ferrari is typically considered a luxury stock like Hermes, rather than an auto stock like GM, Ford or even Mercedes.

Point #2: A+ industry structure leads to earnings visibility and upgrades

When I was a student at Harvard Business School I did many case studies applying the Porter’s 5 Forces Framework. The 5 Forces is an analytical tool developed by Michael Porter in the late 1970s to analyse industry structure and competitive environments.

From this perspective, Ferrari is literally the textbook case of an A+ company. They are a heritage brand with incredibly high barriers to entry, they have few competitors, few substitutes, price insensitive customers with very little bargaining power, and a supply chain that is localised and very difficult to replicate.

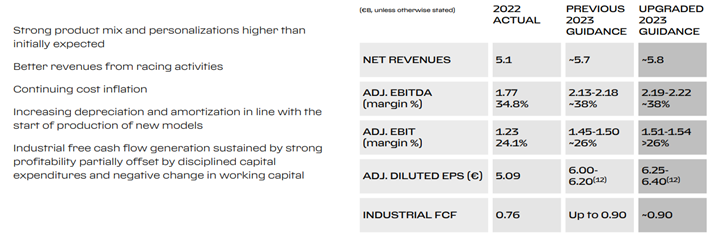

The net result is that Ferrari has an immense level of control over its own earnings and strong earnings visibility. Management upgraded its FY23 revenue guidance, adjusted EBIT margin guidance as well as adjusted EPS and FCF estimates at the last result. More importantly, this upgrade cycle is a consistent pattern shown by RACE management since listing.

Reason #3: Impressive Brand Recognition and Unique Positioning Among Auto Peers

Ferrari is repeatedly recognised as one of the world’s leading brands and they are confident in what their brand stands for and who their target customer is. Most auto meetings these days are focused on the transition to EVs and the rise of autonomous driving (AD). While these are important strategic directions for the auto sector as a whole, it often feels like the companies are in a RACE (no pun intended) to out electrify and out tech each other.

Ferrari is refreshingly contrarian on both these fronts. Ferrari management has made a strong commitment NOT to get into autonomous driving (AD). The whole point of buying a Ferrari is to drive it yourself!

While Ferrari is a leader in hybrids with approximately 45% of deliveries already in the hybrid space, it’s first fully electric car will not be presented until 2025 with the first deliveries the following year. They do not expect pure EVs to be more than 5% of total shipments by 2026. Part of this is strategic positioning that one of the great joys (so I am told) of owning a Ferrari is the vrooooom, sound it makes when you start the ICE engine. EVs don’t vroom so Ferrari plans to continue to develop ICE engines into the 2030s.

Reason #4: Technological leader

Technological leadership comes in part from the company’s F1 racing pedigree. Scuderia Ferrari has been racing in the Formula 1 World Championship since the series was launched in 1950. RACE transfers technologies initially developed for racing to its road cars, which reinforces the brand identity and the scarcity value of the vehicles. Examples include steering wheel paddles for gear shifting, the use and development of composite materials, which make cars lighter and faster, and technology related to hybrid propulsion. RACE road cars have also benefited from the know-how acquired in the wind tunnel by racing car development teams, enjoying greater stability as they reach high speeds.

Investment Risks

Of course, no stock is without risks. For Ferrari, the main risks are that it is a single brand, single product company and therefore lack the diversification of a luxury stock like LVMH or a more diversified auto company like Mercedes or Tesla. From a governance perspective, this is still to some extent a family endeavour with the Agnelli family de facto controlling approximately 51% of the voting rights of the company. Finally, Euronext Milan is not the most liquid market so the Average Daily Traded Value (ADTV) of Ferrari as a EUR50 billion market cap company, is less than it would be if it was traded in the US or France.

Conclusion

The case for RACE is clear. Ferrari is a high margin, high return, high growth company operating in a competitive environment with high barriers to entry, few competitors, leading technology and loyal customers. What’s not to like about Ferrari?

Visit our website to discover further insights from Alphinity.