The bulls took charge of global equity markets at the start of the year on Fed-pivot hopes and China reopening excitement. As we head into the third month of 2023, the bears are starting to wrestle for control, as scepticism over the sustainability of the rally continues to increase.

There are many themes playing out in this tug of war, as is normally the case in global markets. Not only top-down macro and political themes, but also bottom-up, regional, sector and stock specific themes.

In this note we share five themes we expect will have implications for global equity returns this year and 5 stocks to position for each of these.

5 Thematics for 2023

Source: Alphinity, February 2023

Theme 1: Emerging market macro is ahead of Developed markets

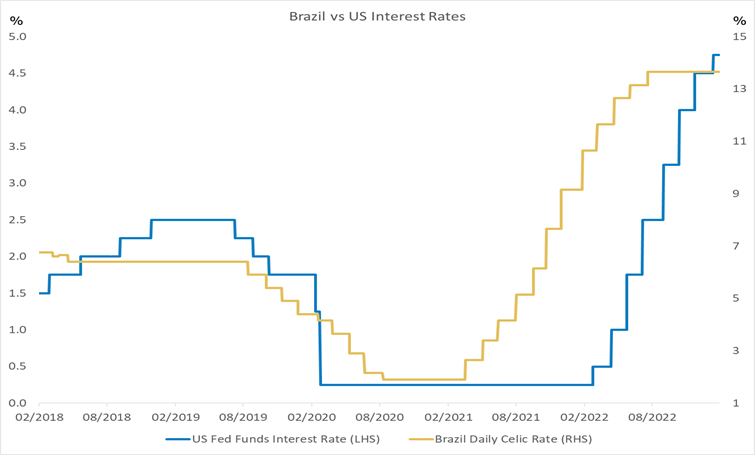

Some of the more vulnerable economies were impacted earlier and more severely by the COVID-19 pandemic, which required a faster and more aggressive reaction. Latin-American economies, such as Brazil, hiked interest rates 12 consecutive times between February ’21 and September ’22, with the market now expecting the first rate cut in November ’23. Inflation and unemployment are also past peak levels, supporting consumer and business confidence.

Brazil started hiking rates well ahead of the US

Source: Bloomberg, February 2023

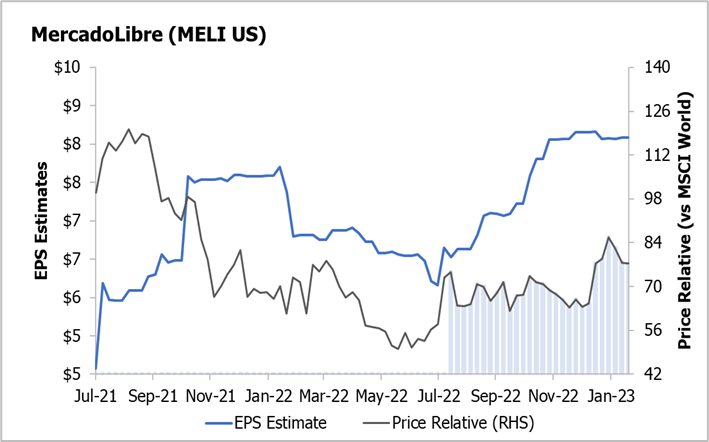

MercadoLibre (MELI): Eco-system model creates huge competitive advantages

MELI is the largest e-commerce and fintech eco-system company in Latin America. Its integrated platform is designed to provide users with a complete portfolio of services, ranging from an extensive marketplace, payment and credit solutions to logistics and advertising.

Their recent 4Q22 result again reflected impressive revenue growth, fantastic operating margin expansion and market share gains across key businesses. MELI is also well positioned to benefit from competitor, Americanas’ (with a c15-17% market share) demise.

MELI is a high-quality company with strong earnings growth, which we view as attractively valued at 40x FY24 price/earnings.

Enjoying positive momentum in revenue & earnings growth

Source: Bloomberg, Alphinity February 2023

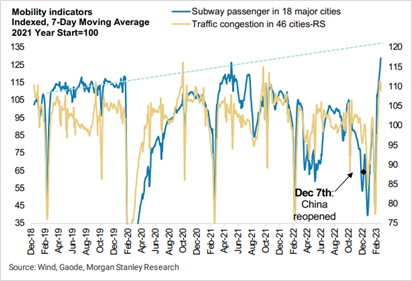

Theme 2: China reopening cadence

China’s reopening after three years of severe COVID lockdowns is now known. A broad range of economic indicators have already recovered, but some questions remain around the implications of China’s ailing property sector, geo-political tensions, the lingering COVID threat and the government’s response to it all. Recent results and muted company commentary flagged the delayed spill over effect into company earnings. China’s recovery will be nuanced with different implications across and within sectors as we shift from the China reopening to recovery phase.

China intracity traffic has normalised and flights have rebounded

Source: Morgan Stanley Research

Starbucks (SBUX): Leading specialty coffee retailer in the world to benefit from China’s reopening

Starbucks is the leading specialty coffee retailer in the world, and one of the largest restaurant chains globally. SBUX owns or operates stores across more than 80 markets. The US still accounts for approximately 70% of revenues but China is the next largest single market.

SBUX recently reported a strong set of 1Q FY23 (or 4Q CY22) results for their US operations, but numbers out of China disappointed. SBUX continued to open new stores in China through COVID, increasing their store count from 4000 to 6000 currently and targeting 9000 by FYE23. Reopening closed stores in addition to their expanded network throughout China, could see a big rebound in China’s revenue and operating profit contributions to the group.

The company guided to strong earnings growth of 15-20% for FY23-25 and capital returns of US$20bn. In our view, SBUX remains attractively valued PE (25x FY24) and Free Cashflow (3% yield)

SBUX: China Same Store Sales – Potential to rebound on reopening

Source: Bloomberg, February 2023

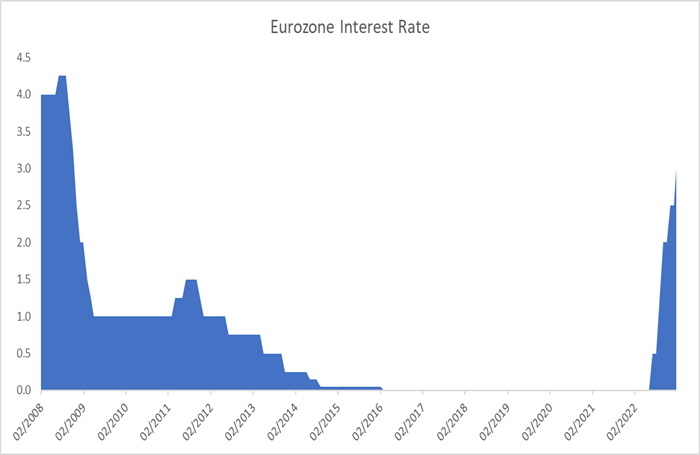

Theme 3: Europe is doing better than feared

If we cast our minds back to the beginning of 2022, the outlook for Europe was particularly gloomy. The Russian/Ukraine war added extra fuel to the supply chain constraints and slowing growth fires. Recent economic data points from manufacturing, to inflation, employment and business activity are all coming through better than feared. Raising hopes that the ECB may be able to hike rates less aggressively and Europe can avoid a recession.

ECB hiking for first time since 2011 positive for European banks

Source: Bloomberg, February 2023

ING Groep (ING) – Best in class European retail bank benefiting from higher rates

ING is a European retail bank and international wholesale bank, servicing approximately 40 million customers across 40 countries worldwide and is a well-recognised digital banking leader.

Looking ahead, we see a potential for Net Interest Income to significantly beat expectations in FY23/24, while credit costs can surprise to the downside in a better than feared macro scenario. Finally, INGA has a strong balance sheet that can deliver higher capital returns for shareholders.

ING offers an attractive combination of resilient earnings growth and an above average forward dividend yield (>7%), which is not fully reflected in current valuations (PE 8.5x forward).

ING – European banks enjoying EPS upgrades again

Source: Bloomberg, February 2023

Theme 4: Biden’s inflation reduction act is a long-term game changer

US President Biden’s Inflation Reduction Act (IRA), signed into law in August 2022, is the biggest climate bill in the country’s history and will have a profound impact across industries for the next decade and beyond. It earmarks c$500bn in new spending but some analysts estimate this could balloon to US$1.3-1.7trn over 10 years.

The act specifically includes $369 billion for clean energy and climate investment, with significant investments in renewables, such as solar and wind.

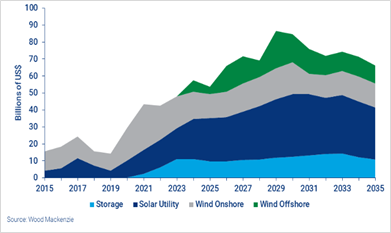

Projected US renewable energy investment under IRA – c$1.2trn through 2035

Source: Wood Mackenzie, February 2023

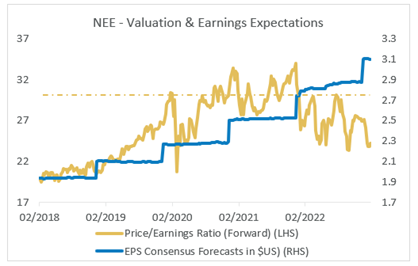

NextEra Energy (NEE) – IRA boosting long term renewables targets

NEE is one of the world’s largest investors in renewable power assets and provides clean energy to approximately 5.8m US customers. NEE is among the best positioned to benefit from the IRA, with a 20% share across US wind, solar and storage markets.

NEE’s recent 4Q22 result rounded out the year with a record 8GW of renewable energy, with a total backlog of 19GW. NEE raised their renewables targets by 15% and extended it to 2026 in response to the IRA.

NextEra has a long history of double-digit earnings growth and is likely to continue beating their targets in our view. Following a recent selloff, the stock is attractively priced at 23x price/earnings, at the lower end of its 5-year trading range.

NEE – Now well below LT valuation & Offering strong EPS growth

Source: Bloomberg, February 2023

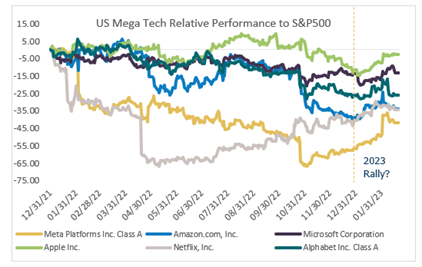

Theme 5: Is FAANGMAN dead or just resting?

The January US Mega tech stock, or so called “FAANGMAN” (Facebook, Alphabet, Amazon, Apple, Netflix, Google etc), rally started to fade throughout the recent reporting season, with many reporting disappointing quarterly results and/or softer guidance for 2023.

Whilst each of the names within the collective have very different underlying drivers, the overall sector continues to see earnings downgrades for FY23 and FY24. In our view, most of these companies are high quality stocks with fantastic business models and innovative management teams. We will revisit these companies again, once share prices adjust to the more subdued economic reality.

US Mega Tech stocks have found new life 2023 YTD, but could be short-lived

Source: Factset, February 2023

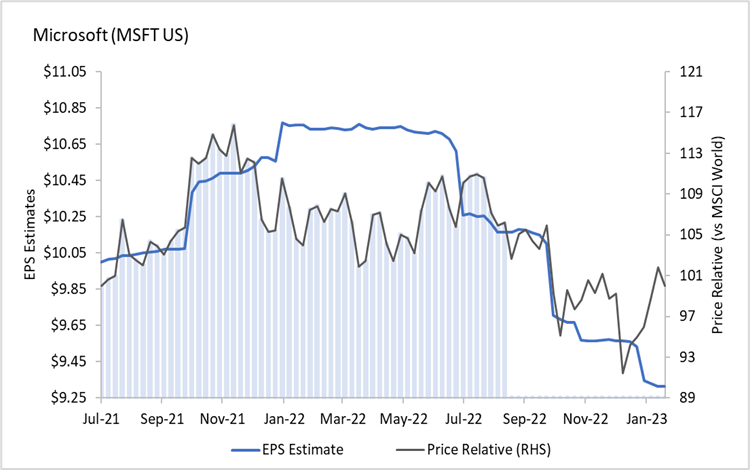

Microsoft (MSFT) – Why it is too early to get excited

Microsoft is the world’s largest software company and a market leader across numerous software categories including productivity applications (Office, Office 365), cloud computing (Azure), operating systems (Windows), business applications, and internet services (LinkedIn).

We exited our position in MSFT in September ’22 as evidence continued to build of a deceleration in Azure and Windows. Alphinity conducted a 2-week US research trip during July 2022, where meetings with cloud players and semiconductor companies validated the thesis of weakening cloud consumption and PC markets.

MSFT’s recent 2Q23 results was another miss with 3Q23 guidance pointing to an ongoing slowdown in Cloud & other areas. With ongoing earnings cuts and a forward price earnings valuation of 28x, the risk/reward remains uncompelling to us.

MSFT – Meetings with Cloud players validated exit thesis in Sept 2022

Source: Alphinity, Bloomberg, February 2023

There will always be numerous themes that will benefit specific companies and disadvantage others. Regardless of a bull or a bear victory.

You can find out more about how at Alphinity we continue to do extensive bottom-up research to find the best beneficiaries through different market cycles here