We wish we could bring better news but the prognosis for the Australian economy is not good with recession risks rising as the consumer enters a new era of pain, whilst the RBA is likely to only consider limited relief by way of cuts. The consumer has been under pressure for some time, but business confidence and activity has held up. That’s changing now, which sees both consumers and business start the year more aligned in a sombre outlook.

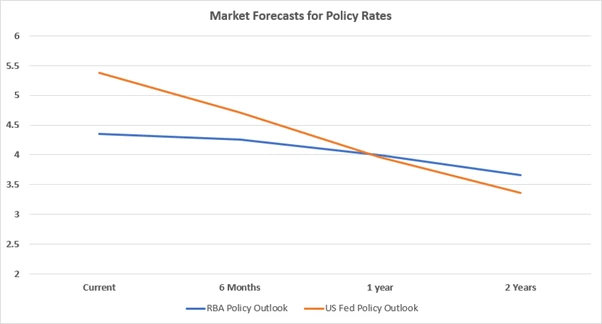

Central banks will ease rates around the world, but this is already starting to be priced in. Policy rates are in restrictive territory, which is helping to slay the inflation dragon as the post-COVID spending frenzy fades. Central banks have been fighting against government policies which have and continue to be expansionary. Employment markets are cooling but from a still firm position providing central banks permission to keep rates higher for longer whilst they await evidence that the inflation job is done. In the US, the rapid deceleration in CPI means the Fed is in play earlier than the RBA, from Q2. To keep rates at their current levels as inflation falls, in a sense, would see the Fed de facto tighten policy as real rates would move higher as inflation falls and policy remained unchanged.

Markets will oscillate around the timing and magnitude of cuts in 2024 but the more important driver for returns over the next 12-24 months is the endgame. We expect the easing cycle to end with a relatively higher policy rate in Australia and the US than prior cycles. To state the obvious, absent an accident, we won’t see a return to ultra-low settings – zero or quantitative easing. And in Australia, it’s clear the 0.75% pre-COVID cash rate won’t be revisited unless we see an economic shock. It’s more likely central banks now regard nominal neutral rates as in the 2.5-3% area. This is only slightly less than what is currently priced into markets over a two-year period. So, to excite bond markets, we need cuts to be brought forward and/or to be larger.

Source: Franklin Templeton, Bloomberg Data

Source: Franklin Templeton, Bloomberg Data

The consumer in Australia enters 2024 on the ropes, which is remarkable given the still low level of unemployment. Australians are saving at the lowest level since the GFC. This is not a bullish signal reflecting confidence to spend but a desperate response to a cost-of-living crisis that has seen real incomes decimated. We know from national accounts that a significant driver of the destruction of real incomes has been by higher levels of tax through bracket creep along with higher interest payments. The implosion in the rate of savings clearly follows a period of accumulation through the COVID period but we now know that the core consumption group of ~24-55-year-olds have burnt through the buffers. As can be seen below, despite the lower savings rate, consumption hit stall speed in 2H 2023 and we see no change in the year ahead.

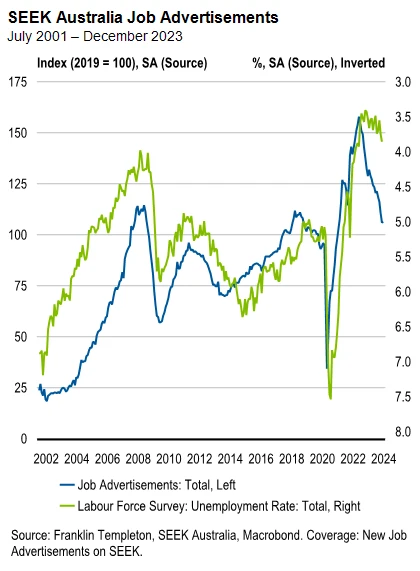

As my colleague Joshua Rout pointed out in our previous note, the labour market is softening. Sure, from a strong position but with the consumer already stretched unemployment doesn’t need to rise that much to accentuate the pressure. The timely SEEK (a popular job search website) monthly job ads data tells us that unemployment is going to 4.5% and possibly higher in the coming months. Still low by historical standards but coming from a low of 3.4% and in a context where the consumer is tapped out, we will see pressure build.

We have observed from the Westpac Melbourne Institute monthly sentiment survey that consumers have expressed extreme levels of pessimism for many months. More recently, however, business confidence has also rolled over after holding up (surprisingly so in our view) for much of 2023. It shouldn’t surprise that business is finally receiving the feedback from their customers and reacting accordingly. The latest reading on confidence from the benchmark NAB Business survey is in negative territory.

National Australia Bank Business Indicators Confidence

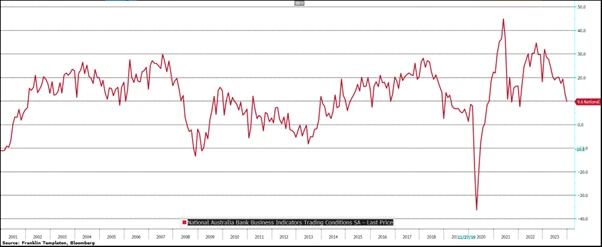

Significantly weaker confidence reflects a deterioration in trading conditions from the same survey which declined through 2023 and is now at the lowest reading since December 2022.

National Australia Bank Indicators Trading Conditions

The bottom line is that consumers were weak in 2023 whilst business, until recently, remained more optimistic. As we head into 2024, both pillars of the economy are weak. This means recession risks are now higher, particularly as the explosive migration led population story settles down and with it the risks that high population growth papers over underlying weak consumption fall.

So, what now for yields?

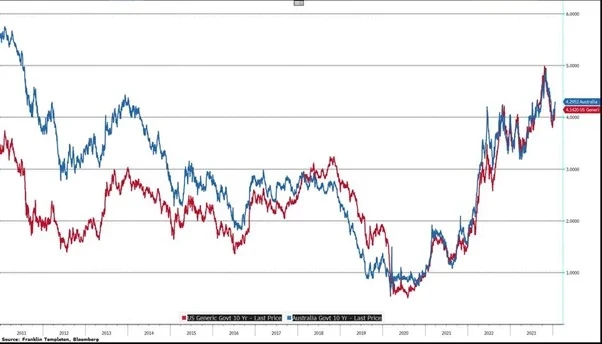

We have maintained that the market is unlikely to see a lot of demand for 10-year bonds that fail to price an adequate risk premium. If central banks perceive neutral rates in this easing cycle to the 2.5-3% area, and the term premium remains around the ~1% area, then the fair value for 10-year government bond yields both in the US and Australia (the latter being dictated to largely by the US) will be in the 4% area. US 10-year treasuries are currently trading at around a 4.14% yield, and Australian 10-year yields are priced at 4.29%. Rather than the persistent 2-3% range for 10-year yields as seen in the 6 years before COVID, it’s more likely we see a 3.5-4.5% range.

Generic US Govt 10-Year Yield & Australian Govt 10-Year Yield

There are any number of risks that could push yields lower in 2024 but it’s likely these would be adverse shocks from left field.

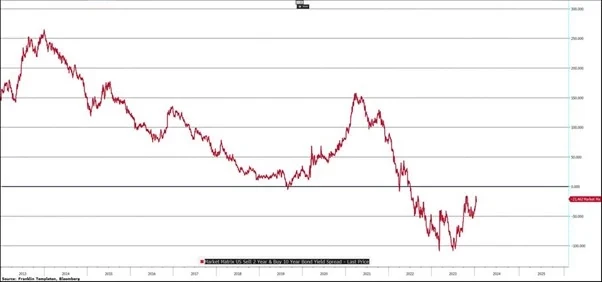

Whilst 10-year yields noodle around their current levels, we expect yield curves to continue to steepen as shorter-term yields decline. In particular, we expect that the US 2-year vs 10-year yield curve differential will return to a positive position after nearly 2 years of inversion. Front end yields historically rally more into easing cycles, and we expect no different behaviour this time. For cash and bank funding, the banks being the savvy participants they are, will likely notch down their term deposit rates as funding rates fall.

US Govt Bond 2-Year vs 10-Year Yield Spread

Credit markets enjoyed a very strong run in 2023 and will confront macro headwinds building in 2024. Credit can continue to perform as investors favour higher yielding but still defensive sectors leading into an easing cycle. We expect non-cyclical investment grade to perform in 1H 2024 as all-in yields in the 5-6%+ area remain attractive. Beyond the 1H 2024, we are more cautious on credit and will monitor if the risks to the downside grow. Within the broader defensives, AAA-rated Residential Mortgage Backed Securities (RMBS) and select Asset Backed Securities (ABS) remain solid and attractive sectors delivering excess returns of approximately 100-150 basis points over cash.

What does it all mean for returns? We believe 2024 might be similar to 2023, a year where yields trade sideways to slightly down with spreads largely stable but facing more pressures as the year progresses. This means returns will be a function of starting yields plus some upside as yields likely moderate lower leaving total returns higher than starting yields. If this proves the case, the outcomes will be quite attractive, with the result being attractive returns above cash and term deposit alternatives to bonds. Should the macro environment see cuts brought forward or delivered in greater quantum, then bonds will rally more.

With respect to our positioning within the Australian Absolute Return Bond Fund, we believe somewhere between a mid to high single digits total return for 2024 expresses a plausible outlook given both our current portfolio positioning and our expectations for the global economy in the year ahead. This would be a similar outcome to 2023 but, arguably, with less volatility likely as inflation risks are now more skewed to the downside.

Andrew Canobi is a Director within the Franklin Templeton Fixed Income team in Melbourne, Australia. Mr. Canobi is a Portfolio Manager for the Franklin Templeton Australian Absolute Return Bond Fund (ASRN 601 662 631).

IMPORTANT INFORMATION

This publication is issued for information purposes only and does not constitute investment or financial product advice. It expresses no views as to the suitability of the services or other matters described in this document as to the individual circumstances, objectives, financial situation, or needs of any recipient. You should assess whether the information is appropriate for you and consider obtaining independent taxation, legal, financial or other professional advice before making an investment decision.

Past performance is not an indicator nor a guarantee of future performance. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. Neither Franklin Templeton Australia, nor any other company within the Franklin Templeton group guarantees the performance of any Fund, nor do they provide any guarantee in respect of the repayment of your capital.

Please read the relevant Product Disclosure Statements (PDSs) and any associated reference documents before making an investment decision. In accordance with the Design and Distribution Obligations and Product Interventions Powers requirements, we maintain Target Market Determinations (TMD) for each of our Funds. All documents can be found via www.franklintempleton.com.au or by calling 1800 673 776.

Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849, AFSL 240827) which is part of Franklin Resources, Inc. Franklin Templeton Australia Limited is the investment manager of the Franklin Australian Absolute Return Bond Fund (ARSN 601 662 631).