Brandywine Global discusses how investors are heavily positioned for US growth and how asset market outperformance and the margin for error for the United States is now much, much lower.

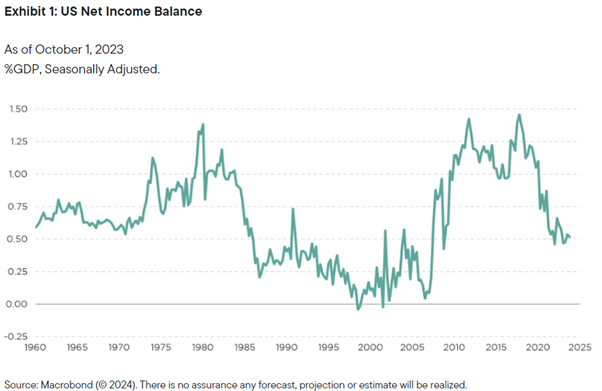

During the 2000s, following the US equity bear market and the rise of China, the US private sector invested heavily overseas to capitalize on more attractive investment opportunities. Over time, this trend led to a substantial improvement in the US net income balance—namely, the difference between what the US earns on its investments overseas minus what it pays to foreign investors in US assets (see Exhibit 1).

While the US remained a net debtor to the world in aggregate because foreign central banks still owned sizeable amounts of US Treasuries, it became a sizeable net creditor to the private sector globally. For the purposes of understanding prospective capital flows and market implications, what matters are the decisions of private sector entities, and by 2012, the private sector held a sizeable short position in the US dollar (USD).

From Net Short to Significant USD Long Position

Over the last decade, this trend has massively reversed. The US has experienced superior growth and asset market performance. On the one hand, the shifting economic model in China, characterized by lower leverage, a weaker property sector, and higher geopolitical risk, and the dual sovereign and banking crises in Europe lowered growth expectations in both regions. On the other hand, renewed technology leadership, resurgent manufacturing, and newfound energy independence via shale gas and oil raised US growth expectations.

As a consequence, private sector capital flows have shifted significantly. Since 2010, foreign investment into the US has surged, such that the net investment position of the US private sector has swung from a $2 trillion (net) surplus to around an $11 trillion (net) deficit. Nearly $9 trillion of that change occurred over the past seven years (see Exhibit 2).

As a share of gross domestic product (GDP), the US has shifted from overweighting foreign assets to the tune of 15% GDP to now underweighting foreign assets in the vicinity of 40% GDP. Alternatively, foreign investors have shifted from underweighting the US by 15% GDP to overweighting US assets by 40% GDP (see Exhibit 3).

This is not to say that investors are wrong in favouring US assets. Investors’ overweight exposure to US assets may well be justified if the US continues to offer better returns on investments than those offered in other parts of the world. Indeed, recent US growth and equity outperformance is validating the overweight position.

However, the point here is that investors are already heavily positioned for US growth and asset market outperformance, a dramatic change from investor positioning in 2010. The margin for error for the US is now much, much lower—if the US economy and markets disappoint, there are now trillions of dollars that could exit US markets.

Franklin Templeton can help you elevate your fixed income portfolio with the expertise from our specialist investment managers. Whether you’re seeking core fixed income, global exposure, or absolute return strategies, Franklin Templeton provides a diverse array of options to meet your investment needs. Discover how our comprehensive suite of strategies can transform your portfolio today, Learn How.

IMPORTANT INFORMATION

This publication is issued for information purposes only and does not constitute investment or financial product advice. It expresses no views as to the suitability of the services or other matters described in this document as to the individual circumstances, objectives, financial situation, or needs of any recipient. You should assess whether the information is appropriate for you and consider obtaining independent taxation, legal, financial or other professional advice before making an investment decision. Issued by Franklin Templeton Australia Limited (ABN 76 004 835 849, AFSL 240827).

© Franklin Templeton Australia Limited. You may only reproduce, circulate and use this document (or any part of it) with the consent of Franklin Templeton Australia Limited.