Integrating Living Legacies: A Transformative Approach to Wealth Transfer Strategies Among Clients

The transfer of wealth between generations is an important topic for many older Australians, who are increasingly seeking guidance on how their assets should be divided while still alive. This often involves difficult questions around how much wealth should be transferred, who the recipients will be and what sorts of activities should be funded.

Demographic factors are pushing many Australians to consider living legacies. The last of the baby boomers are now entering retirement and many are holding record amounts of wealth as property prices have soared. As a result, many older Australians are keen to transfer their wealth during their lifetimes to other family members who may be not so fortunate or well-off.

Simple desires often involve wanting to help children or grandchildren buy their first home, fund their secondary or tertiary education, pay for weddings, or help out in other ways with smaller monetary gifts. The cost-of-living crisis in Australia has added to the impetus for the transfer of wealth to younger Australians – so much so that Australia is now experiencing one of the biggest generational wealth transfers it has ever experienced. It is estimated that Australians aged 60 or over will be transferring an average of $175 billion per year in wealth for the next decade at least, according to a 2021 Productivity Commission report.

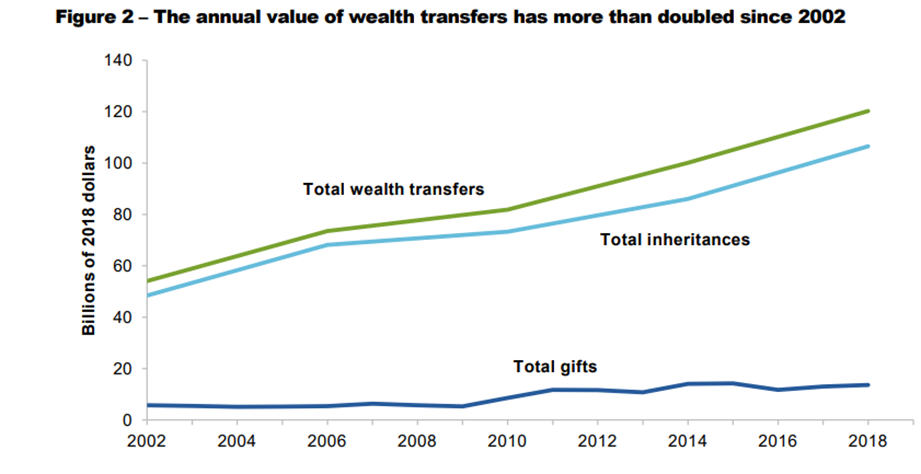

That report found that the aggregate annual value of wealth transfers has more than doubled in real terms since 2002. Between 2002 and 2018, the aggregate value of wealth transfers was approximately $1.5 trillion, of which $1.3 trillion was inheritances and $155 billion was gifts, as the chart below shows.

Source: Productivity Commission, Wealth transfers and their economic effects

Fidelity’s own research highlights the trend towards living legacies and the desire for it. A recent study undertaken for Fidelity by research firm MYMAVINS found that almost four in five Australians aged 26 years or older believed sharing their wealth with the next generation was important. The research involved an online survey of 1,500 Australian consumers over 26, with fieldwork undertaken in September 2023.

The Fidelity International survey found that two in five people prefer to share their wealth as a living legacy compared to one in five who prefer to just share their wealth as a bequest. The remaining two in five have an equal preference, meaning that four in five want to leave a living legacy.

Canvassing the options an important discussion

Fidelity’s own conversations with clients shows that many Australians do not want to wait until they have passed on their wealth and would prefer to leave a financial legacy while alive.

What has often helped to prompt this discussion is an annual review of clients’ finances. One of the things advisers tell us they talk about with clients at every review is whether any estate planning is in place or, if they don’t have anything in place, they have a conversation about the importance of it. That has been very effective in getting clients to plan estates and consider living legacies.

Typically, wealth advisers investigate different options with clients before final decisions are made to explore different ways of making wealth transfers. This can involve anything from simple monetary gifts to a grandchild to multiple gifts spread across children and grandchildren, or perhaps larger transfer to enable to purchase of shares or property.

Educating clients on their options is important. Sometimes the education involves starting with the basics on who the recipients of the transfer will be. Sometimes, the best approach is to start with their children and do some work with them to better understand their spending or savings habits. That may involve helping to teach good wealth-making habits. This is important to give the benefactor the confidence that the transferred funds will be used for a good purpose such as wealth creation or debt reduction.

Once the type and method of transfer is decided with clients, communicating the living legacy and its purpose to the beneficiaries is very important. This is an opportunity for older Australians to engage recipients on the wealth transfer, its significance and its management.

Gen Y, or millennials, are the generation that will be receiving the most wealth and are more likely to take a collaborative approach with their financial advisers. They have also grown up with more technology than their parents and are happy to complement or verify any advice with their own research. Wealth advisers and other professional can also guide Australians through these decisions.

Those in the Fidelity International Survey who said they would seek out professional help were most likely to trust a solicitor or family lawyer on estate planning matters at 49 per cent, followed by a professional financial planner at 37 per cent.

Our survey also found that from a Gen Y perspective, many said that if they were to receive significant financial help, or inheritance from their family, they would rely on a professional financial planner for advice for what’s best to do with it.

Governance of transfer matters

A framework governing intergenerational wealth transfer can help families better manage, preserve, and maintain control of the transfer of and, importantly, to avoid conflict. Important factors to consider in a living legacy plan include clearly identifying who the beneficiaries will be, determining the most appropriate investment vehicles to hold and transfer assets and rules for resolving disagreements. While not all wealthy retirees believe they have an obligation to transfer wealth, among those that do, avoiding disputes and conflicts is often a key concern.

With so much wealth at stake, professional advice is important. While wealth holders and managers have concentrated primarily on wealth creation and its protection in the past, this is changing as living legacies become more important. As older Australians accumulate record levels of wealth, wealth transfers must be carefully planned to keep relationships between generations harmonious and to ensure the effectiveness of living legacies.

We recently launched a podcast series in conjunction with Ensombl which you can listen to here to learn more about living legacies.

All information is current as at 13 March 2024 unless otherwise stated. Not for use by or distribution to retail investors. Only available to a person who is a “wholesale client” under section 761G of the Corporations Act 2001 (Commonwealth of Australia) (“Corporations Act“)

This document is issued by FIL Responsible Entity (Australia) Limited ABN 33 148 059 009, AFSL No. 409340 (‘Fidelity Australia’). Fidelity Australia is a member of the FIL Limited group of companies commonly known as Fidelity International. Prior to making any investment decision, investors should consider seeking independent legal, taxation, financial or other relevant professional advice. This document is intended as general information only and has been prepared without taking into account any person’s objectives, financial situation or needs. You should also consider the relevant Product Disclosure Statements (‘PDS’) for any Fidelity Australia product mentioned in this document before making any decision about whether to acquire the product. The PDS can be obtained by contacting Fidelity Australia on 1800 044 922 or by downloading it from our website at www.fidelity.com.au. The relevant Target Market Determination (TMD) is available via www.fidelity.com.au. This document may include general commentary on market activity, sector trends or other broad-based economic or political conditions that should not be taken as investment advice. Information stated about specific securities may change. Any reference to specific securities should not be taken as a recommendation to buy, sell or hold these securities. You should consider these matters and seeking professional advice before acting on any information. Any forward-looking statements, opinions, projections and estimates in this document may be based on market conditions, beliefs, expectations, assumptions, interpretations, circumstances and contingencies which can change without notice, and may not be correct. Any forward-looking statements are provided as a general guide only and there can be no assurance that actual results or outcomes will not be unfavourable, worse than or materially different to those indicated by these forward-looking statements. Any graphs, examples or case studies included are for illustrative purposes only and may be specific to the context and circumstances and based on specific factual and other assumptions. They are not and do not represent forecasts or guides regarding future returns or any other future matters and are not intended to be considered in a broader context. While the information contained in this document has been prepared with reasonable care, to the maximum extent permitted by law, no responsibility or liability is accepted for any errors or omissions or misstatements however caused. Past performance information provided in this document is not a reliable indicator of future performance. The document may not be reproduced, transmitted or otherwise made available without the prior written permission of Fidelity Australia. The issuer of Fidelity’s managed investment schemes is Fidelity Australia.

© 2024 FIL Responsible Entity (Australia) Limited. Fidelity, Fidelity International and the Fidelity International logo and F symbol are trademarks of FIL Limited.