From ethical investing to insurance and budgeting advice, there’s plenty of room for advisers to make a difference when building out an offering for this key segment of the market.

Key takeaways

- Female investors tend to be risk-averse

- Many would be receptive to more ethical investments

- Financial needs outside pure investment come into consideration

As female investors of all ages become a growing market for financial advice, any firm would be wise to build out an offering tailored specifically to this segment. To do this requires a good understanding of their investing preferences and financial goals.

Based on the 681 women Netwealth surveyed for its Women as the New Face of Wealth report, here are some key insights on female investors for advisers wanting to enhance their services for this deserving and likely underserved part of the market.

A fondness for the familiar

Many female investors can be conservative, which can potentially lead to lack of diversification in a portfolio.

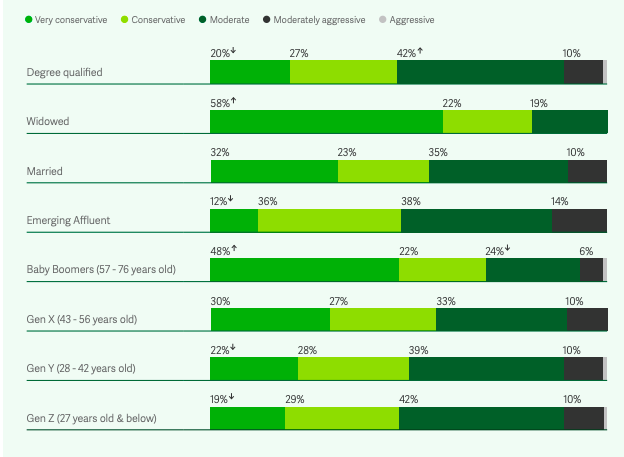

One in three (31 per cent) of women say they are very conservative and avoid exposure to risky assets, while a further 26 per cent say they are conservative and want to invest for guaranteed returns and minimal exposure to risky assets. Another third rate themselves as moderate investors looking for stable and reliable returns without much risk.

This conservatism does shift a bit for younger generations, with Gen Y and Z more likely to be moderate investors, (39 per cent and 42 per cent, respectively), as are those with a degree (42 per cent).

At the other end, older baby boomers are the most risk averse, with 48 per cent rating themselves as very conservative, as are those who are separated or divorced (42 per cent) and widowed (58 per cent).

How would you best describe yourself as an investor?

Source: Netwealth 2023 Advisable Australian (Women 18+ only)

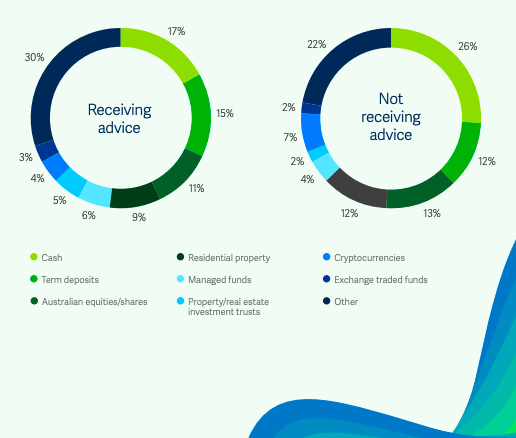

It follows, therefore, that female investors favour the familiar, with 64 per cent of women preferring to invest in more commonly known and available investments.

This skews their portfolio to asset classes such as Australian equities (17 per cent currently invest in them), term deposits (15 per cent) and residential property (14 per cent). A quarter of their portfolios are sitting in cash. Other asset classes they invest in less frequently include cryptocurrencies, managed funds, property/real estate trusts and ETFs.

% allocation in dollar terms of their investment portfolio for those women…

Source: Netwealth 2023 Advisable Australian (Women 18+ only)

For an adviser, there may be value in educating their clients more to help them understand the benefits of diversification, proper asset allocation and the variety of asset classes available to them, at the same time remembering that a conservative approach favouring more commonly available options is not entirely bad as long as it is diversified.

Social conscience a key consideration

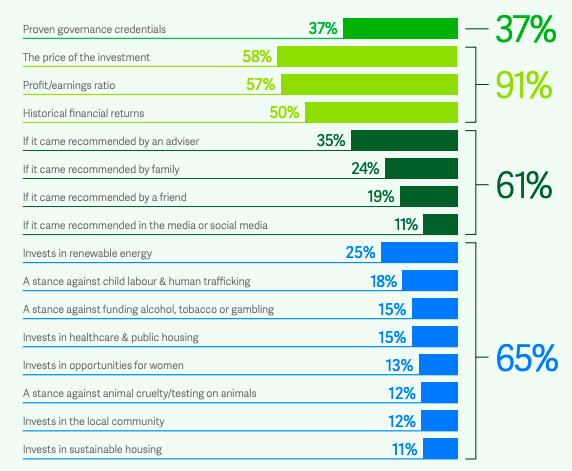

It’s worth noting that many women do invest with an eye on environmental, social and governance (ESG) factors. Financial considerations are top – including the price of the investment (57 per cent), P/E ratios (57 per cent) and historic financial returns (50 per cent). However, ESG factors rank next in importance, with 37 per cent looking at proven governance credentials when investing. Also, 25 per cent said they would invest in renewable energy; 15 per cent would invest in healthcare & public housing; 15 per cent would look at a company’s stance against child labour & human trafficking; 15 per cent at their stance on funding alcohol, tobacco or gambling; and finally, 13 per cent would look at how the company invests in opportunities for women.

Which of the following attributes are most important to you when choosing an investment, you may choose up to five(of those currently investing)?

Source: Netwealth 2023 Advisable Australian (Women 18+ only)

At the same time, there is potential for advisers to help them further in this direction. Over half of women care deeply about environmental issues (59 per cent) and social issues (54 per cent), but only a quarter currently hold responsible investments in their portfolio. However, 42 per cent of those who don’t currently have responsible investments would consider doing so if they didn’t need to pay more, sacrifice returns, and the investment made a quantifiable difference to the environment or society.

Many women look to invest in line with their values, so they may favour investments that not only perform well but also create a positive impact, as opposed to investing solely for performance alone. Advisers should investigate the different responsible investment options available and develop a philosophy and position so they can then offer them to their clients.

Goals extend beyond investing

There is further room to help the large proportion of women who have financial goals beyond investing, but perhaps lack the confidence to realise them.

For example, the results show there could be potential for more cash flow planning, despite apparent assuredness in this regard. On one hand, most women (75 per cent) are confident they can manage their own day-to-day finances, and when making daily money decisions, such as managing the daily budget, and most (65 per cent) said they will not rely on others. Somewhat contradicting this is that many have active saving goals — 59 per cent are actively working on creating and sticking to a budget — and only 35 per cent are very confident in achieving these saving goals.

Insurance is another area where there is unmet need. Only one in three women (34 per cent) have any type of risk-based insurance such as life or income protection — lower compared to males (46 per cent). However 56 per cent are actively working towards arranging or reviewing their insurance, and advisers should take note that just 29 per cent of those say they are very confident they will achieve this goal.

And finally, another area where they need support is estate planning, with 56 per cent saying they are actively engaged in estate planning for the next generation.

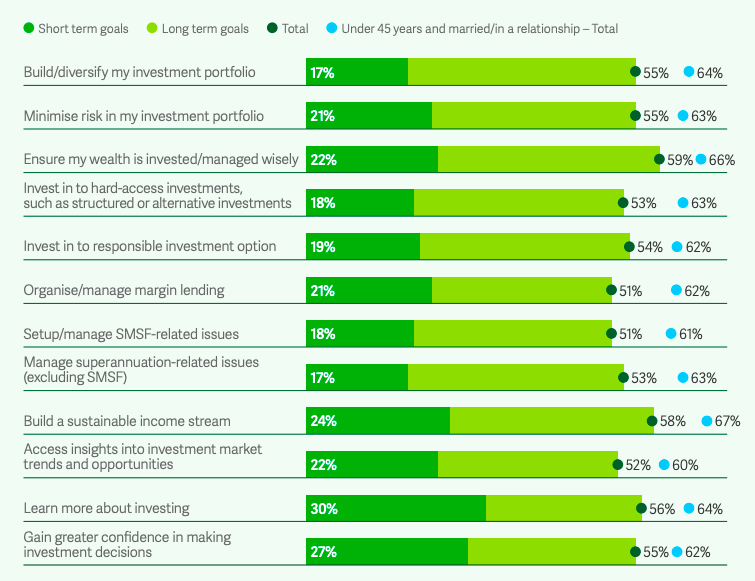

Which of the following financial and wealth goals are you actively working towards in the short term (less than five years) and long term (five years plus)?

Source: Netwealth 2023 Advisable Australian (Women 18+ only)

Not surprisingly women of all ages have a variety of goals that go beyond investing, yet in most instances they are not confident in achieving them in the short or long-term.

Wealth professionals are clearly well placed to support their needs, but for some, they will need to broaden their offering to extend to family and legacy planning.

This is particularly relevant to segments such as divorcees that may have a broader range of wealth goals. Wealth professionals could look to offer a holistic (one-stop-shop) service that brings in the expertise of a range of professionals including divorce lawyers, real estate agents, estate planners and accountants.